Anecdotal Evidence

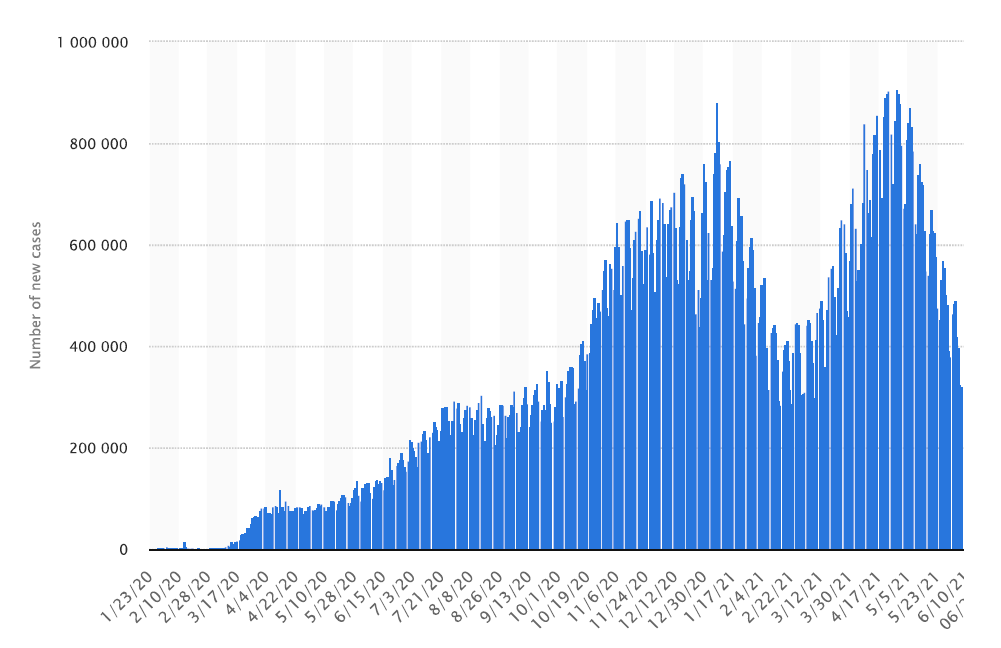

Coming out of the worst part of the global COVID-19 pandemic has not been easy and not nearly as predictable as most thought. What was thought to be the peak in global cases early this year and the quick decline that followed was the hope that the global population needed to gain some perspective on how long the disease related social restrictions might last, however a 2nd ramp up that peaked in late April seems to have validated the concept of ‘waves’, which led some to the expectation that additional waves are possible and likely. The initial ramp toward the first wave was met with hard restrictions on travel and social distancing that changed the way the global population interacted and set a tone for what has been described as a new social order, while the 2nd wave seems to have been less restrictive, with more push to return to a more ‘normal’ social structure. Having spent many years looking at cyclicality across a number of industries, we see the rise and fall of this disease as cycles and expect the pattern to continue.

Global New COVID-19 Cases – 1/23/20 to 7/4/21 – Source: Statista

That said, during each of these cycles, the effects of the virus on global social culture was profound and changed the way vast numbers of people performed their jobs. The quarantines that were a result of the rising side of each cycle forced many to work in isolation, generating significant demand for CE products that either made such work possible, such as laptops and PCs, or provided entertainment during those periods when what would have been more normal social interaction would have been restricted. While part of the global workforce huddled in their homes and wore PJs during Zoom meetings, those that provided the necessary equipment to allow that change in social culture continued to work. At the onset of the first wave, not all workers were able or wanted to expose themselves to a factory environment and staff shortages led to component shortages that began to spread across the CE space, but even when the first wave subsided, businesses saw this social change as something more permanent, rather than something that was a result of a ‘forced’ situation.

Buyers were given strict orders to make sure that components were available so demand could be met and cost became secondary and even though the first wave quickly trended down, the CE supply chain did not deviate from its objective of amassing inventory to fill the needs of this new, less mobile population. This proved correct as the second wave hit, and even with factory staffing closer to normal levels, components remained in short supply, particularly in those industries that have a high new capacity cost. As the second wave began to ebb, mangers were now convinced that the concept of inventory at all cost was correct and component shortages continued triggering more price increases.

But now, something has changed. Rather than the gleeful enthusiasm that has been the watchword of many in the CE supply chain and the daily talk of product delivery dates in 2022, we hear more that ‘while prices will rise in 3Q, the rate of increase will be lower’, or ‘we expect component shortages to ease in 2H’, or even a bit of hesitancy to build inventory as we head toward the holiday season. These are anecdotal points, and not shared by every point in the CE supply chain, but for the first time since last year, we see some businesses beginning to question the need to continue to pay up for components.

Whether this is a natural course of events for a cyclical industry or whether just a pause in a very intense cycle is hard to tell, and not everyone echoes these thoughts. Some continue to whistle past the graveyard and believe that this unusual circumstance is the new norm, while others are at least working with a bit more caution than in past quarters, especially those that have seen a leveling off of consumer demand, such as in the TV or smartphone markets. But regardless of the reasoning, we have noticed the change, which we would categorize as an attitude more reflective of reality, rather than one that has been akin to sprinting without knowing how far away the finish line is.

Don’t get us wrong. We do not think that the CE supply chain has abandon all hope and is awaiting the next rise of Aion (who is the Greek god of cyclicality or unbounded time, Alec), but caution and a conservative approach has not been in the CE dialect for about a year, and with the first few bits of restraint beginning to appear, we thought it notable. The only thing that worries us has been the lack of the usual, ‘but this time it’s different’ that usually comes right before a down cycle, but perhaps we just didn’t hear it.

Buyers were given strict orders to make sure that components were available so demand could be met and cost became secondary and even though the first wave quickly trended down, the CE supply chain did not deviate from its objective of amassing inventory to fill the needs of this new, less mobile population. This proved correct as the second wave hit, and even with factory staffing closer to normal levels, components remained in short supply, particularly in those industries that have a high new capacity cost. As the second wave began to ebb, mangers were now convinced that the concept of inventory at all cost was correct and component shortages continued triggering more price increases.

But now, something has changed. Rather than the gleeful enthusiasm that has been the watchword of many in the CE supply chain and the daily talk of product delivery dates in 2022, we hear more that ‘while prices will rise in 3Q, the rate of increase will be lower’, or ‘we expect component shortages to ease in 2H’, or even a bit of hesitancy to build inventory as we head toward the holiday season. These are anecdotal points, and not shared by every point in the CE supply chain, but for the first time since last year, we see some businesses beginning to question the need to continue to pay up for components.

Whether this is a natural course of events for a cyclical industry or whether just a pause in a very intense cycle is hard to tell, and not everyone echoes these thoughts. Some continue to whistle past the graveyard and believe that this unusual circumstance is the new norm, while others are at least working with a bit more caution than in past quarters, especially those that have seen a leveling off of consumer demand, such as in the TV or smartphone markets. But regardless of the reasoning, we have noticed the change, which we would categorize as an attitude more reflective of reality, rather than one that has been akin to sprinting without knowing how far away the finish line is.

Don’t get us wrong. We do not think that the CE supply chain has abandon all hope and is awaiting the next rise of Aion (who is the Greek god of cyclicality or unbounded time, Alec), but caution and a conservative approach has not been in the CE dialect for about a year, and with the first few bits of restraint beginning to appear, we thought it notable. The only thing that worries us has been the lack of the usual, ‘but this time it’s different’ that usually comes right before a down cycle, but perhaps we just didn’t hear it.

RSS Feed

RSS Feed