TV Prices – In Limbo Again

The Pre-Launch Pricing Vacuum

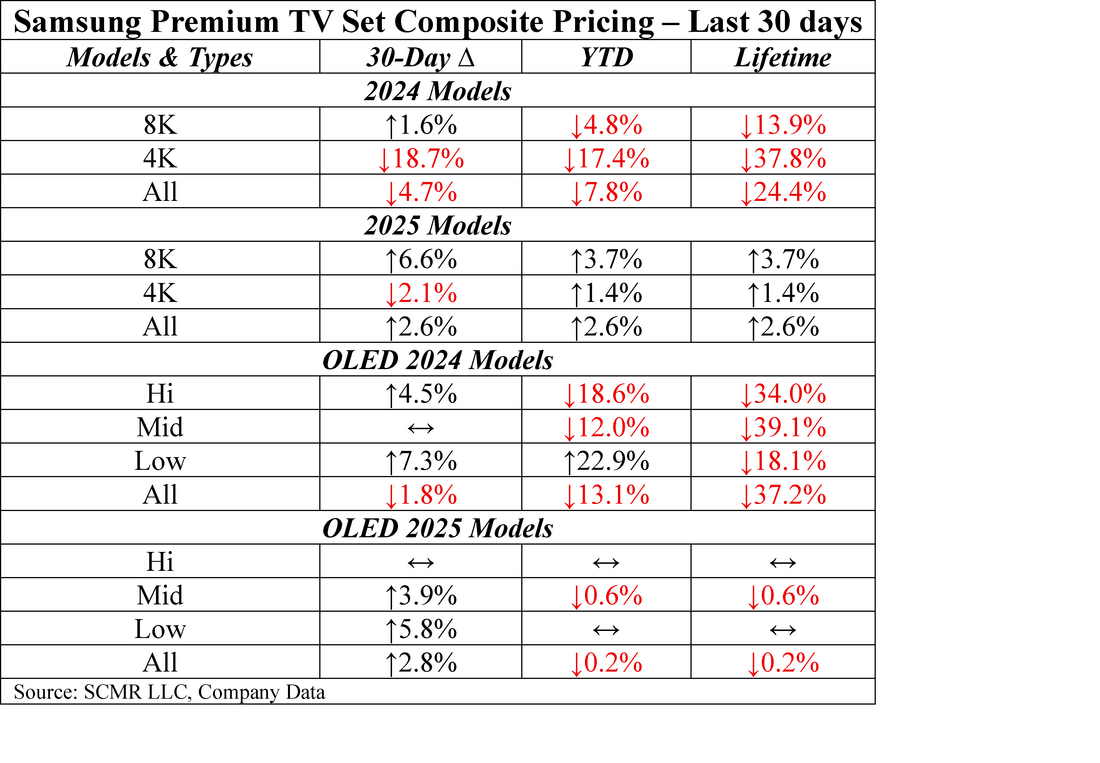

Detail is not particularly necessary to indicate Samsung’s premium TV pricing thus far into the year.. Most categories have seen price increases since year-end 2025, ranging from up 0.4% to up 4.7% by category. On an unweighted basis the Mini-LED/QD segment, which includes both 8K and 4K Mini-LED/QD TV sets, did see a decline of 0.4%, which came entirely from Samsung’s 8K line, while the much large 4K line saw the 0.4% price increase mentioned above. In the OLED TV line only the low end category saw a decline since year-end, while all other OLED set categories saw increases.

Segment Breakdown: Divergent Trends in Mini-LED and OLED

Looking at the 2025 line by category for both year-to-date price movements and lifetime prices gives a better indication of where 2025 TV set prices are on a relative basis.

Detail is not particularly necessary to indicate Samsung’s premium TV pricing thus far into the year.. Most categories have seen price increases since year-end 2025, ranging from up 0.4% to up 4.7% by category. On an unweighted basis the Mini-LED/QD segment, which includes both 8K and 4K Mini-LED/QD TV sets, did see a decline of 0.4%, which came entirely from Samsung’s 8K line, while the much large 4K line saw the 0.4% price increase mentioned above. In the OLED TV line only the low end category saw a decline since year-end, while all other OLED set categories saw increases.

Segment Breakdown: Divergent Trends in Mini-LED and OLED

Looking at the 2025 line by category for both year-to-date price movements and lifetime prices gives a better indication of where 2025 TV set prices are on a relative basis.

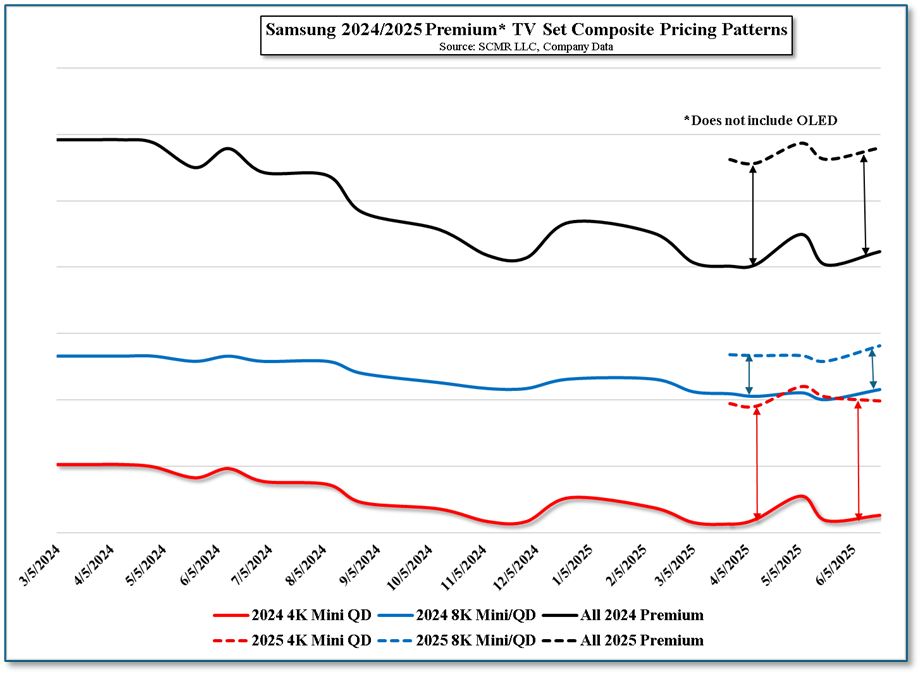

We note that almost all TV set models reached 2025 lows on or around the Black Friday holiday and rose in price through the Christmas and New Year holidays, so it is of no surprise that most have continued to increase in price since year end. As new models are typically released in late March 2025 models are in a no-man’s land of pricing as there is little for consumers to compare against.

The 2026 Outlook: Compounding Cost Pressures

That said, we expect upward price pressure on new models, or perhaps similar pricing to last year’s initial prices but a slower price decline to offset increased memory costs. Since the tariff rules have changed once again, much CE pricing for 2026 models is in limbo, but unless the current administration acquiesces to the will of the Supreme Court quickly, all bets are off until a clearer tariff picture is found. Therefore we expect more TV set price movement based on inventory levels than cost and import/export issues until the administration decides what path it will take on tariffs.

Conclusion: A Strategic Stalemate for Premium TV Pricing

The current state of Samsung’s premium TV pricing is best described as a "strategic stalemate" driven by three conflicting forces: seasonal inventory clearing, skyrocketing component costs, and a volatile regulatory environment.

For the consumer, the window for "value" has temporarily closed. With 2025 models rising from their holiday lows and 2026 models poised to launch at a premium, inflated by both memory scarcity and renewed tariff uncertainty, the market is likely to remain in pricing limbo until the secondary discount cycle begins in late second quarter.

The 2026 Outlook: Compounding Cost Pressures

That said, we expect upward price pressure on new models, or perhaps similar pricing to last year’s initial prices but a slower price decline to offset increased memory costs. Since the tariff rules have changed once again, much CE pricing for 2026 models is in limbo, but unless the current administration acquiesces to the will of the Supreme Court quickly, all bets are off until a clearer tariff picture is found. Therefore we expect more TV set price movement based on inventory levels than cost and import/export issues until the administration decides what path it will take on tariffs.

Conclusion: A Strategic Stalemate for Premium TV Pricing

The current state of Samsung’s premium TV pricing is best described as a "strategic stalemate" driven by three conflicting forces: seasonal inventory clearing, skyrocketing component costs, and a volatile regulatory environment.

- The 2025 Inventory Floor -The data confirms that the "price floor" for the 2025 lineup was established during the Black Friday window. The subsequent YTD increases in most categories, particularly the 4.7% rise in High-tier OLEDs, indicate that retailers have successfully transitioned from aggressive liquidations to a "harvest" phase. With the 2025 models now in a "no-man's land" ahead of the 2026 launch, current pricing reflects a lack of competitive pressure rather than a surge in demand.

- The "DRAM" Factor - While 2025 models are drifting, the 2026 lineup faces a significant cost-of-goods headwind. The DRAM crisis, driven by the AI-fueled surge in DRAM and NAND demand, has caused memory costs to more than quadruple. For a premium Smart TV, which relies heavily on these chips for AI processing and upscaling, this translates to a ~5–7% increase in the total Bill of Materials (BOM). Consequently, consumers should expect the initial MSRPs for Samsung’s 2026 "TV sets to be set higher (more likely) than last year’s launch points to protect manufacturer margins unless they decide to bite the bullet and maintain comparative initial pricing but reduce discounting momentum going forward (less likely).

- The Tariff Wildcard - The February 20, 2026, Supreme Court ruling (striking down IEEPA-based tariffs) initially suggested a potential reprieve for consumer electronics. However, the administration’s immediate pivot to Section 122 tariffs (imposing a 15% duty effective February 24) has effectively neutralized any near-term price relief. This "tariff ping-pong" ensures that inventory management, rather than fundamental cost reduction, will remain the primary driver of retail price movement, likely through the first half of the year.

For the consumer, the window for "value" has temporarily closed. With 2025 models rising from their holiday lows and 2026 models poised to launch at a premium, inflated by both memory scarcity and renewed tariff uncertainty, the market is likely to remain in pricing limbo until the secondary discount cycle begins in late second quarter.

RSS Feed

RSS Feed