Sharp’s Two-Fab Future: A Quick Study in Strategic Consolidation

The Restructuring of Yongo and the Foxconn Influence

Rumors have been circulating in Japan that Sharp (6753.JP) plans to close its Yonago’ subsidiary as part of its continuing restructuring effort under the leadership of Foxconn (2354.TT), who holds a 66% controlling stake in Sharp. The press hinted that this would lead to the closing of one of Sharp’s small panel fabs, however the Yonago facilities are not panel producers but assemblers, taking raw panels (typically open cell) and adapting them for specific applications or purposes.

The Survival of Kameyama #1 & the Survival of Kameyama #2

We expect Sharp will still maintain LCD panel production at its Kameyama #1 fab, which produces automotive displays, ruggedized displays, displays for medical devices, and POS/ATM displays. Sharp also operates a Gen 6 fab in Hakusan, but that fab was partially financed by Apple (AAPL) and is not owned by Foxconn. Sharp closed its Kameyama #2 fab (still producing small amounts until later this year), which will become an AI server production facility and an EV parts manufacturing plant after it winds down its last obligations.

The Hakusan Fab: A Strategic Partnership with Apple

As mentioned above, Sharp technically also owns a Gen 6 plant in Hakusan which it purchased from Japan Display (6740.JP) in 2020 for $390 million, however while Sharp owns the real estate, Apple owns much of the specialized equipment in the fab, making it a dedicated fab for small/medium Apple devices. Sharp also maintains a Micro-LED pilot line at the Hakusan plant and Foxconn (not Sharp) owns a Gen 10.5 LCD TV panel plant in Guangzhou, which continues to operate, producing TV panels.

The Legacy of Sakai: From LCD Pioneer to AI Data Center

Sharp has had a rocky career in the display space. As one of the first LCD display developers, building screens for calculators and handheld devices, Sharp built its first LCD plant in Tenri, Japan back in 1973, even before they had ‘generation’ designations for substrate sizes.. This was followed by R&D lines and the company’s first Gen 1 fab in 1991 and a Gen 3 fab in 1995. But the real expansion took place in the 2000’s with Sharp’s Gen 4 Mie #3 plant (2003), Kameyama #1 (Gen 6) in 2004, Kameyama #2 (Gen 8) in 2006, and under the heading of ‘Bigger is Better’, Sharp began building some of the largest and most modern LCD fabs in 2009, culminating in the construction of the first Gen 10 LCD fab in Sakai in 2009. This plant was considered the most sophisticated in the world, but arrived just as TV set demand was declining, and while a technical marvel at the time, was a burden for Sharp in the 2010 to 2020 time frame. The plant was closed and sold to Softbank (9434.JP) (459,999 m2 for ~$676 million) and KDDI (9433.JP) (former color filter plant ~33,000m2 for $68 million). The facilities are to be used for AI training and agent hosting.

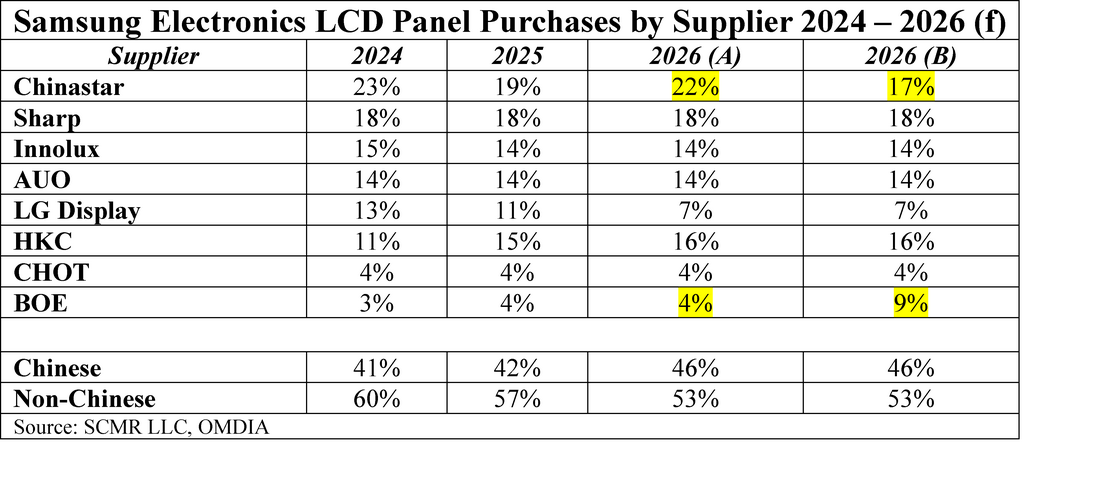

In 2016 Foxconn’s purchased its controlling stake in Sharp after years of Sharp’s losses in the display space and began the era of a more ‘asset light’ Sharp, eventually leading to what will be Sharp’s position in the middle of this year, a much smaller company with two fabs, and a more diverse product portfolio that is far less dependent on internal product production. In fact Sharp will have only two remaining fabs by the end of this year, the Hakusan fab that produces small panel displays for Apple, and the Kameyama #1 fab that produces automotive and medical displays, a far cry from twenty years ago when Sharp was the leading producer of LCD displays worldwide (15% to 20% share depending on the quarter) and the leading brand in North America, beating out rivals Samsung Electronics (005930.KS) and Sony (SNE).

Conclusion – A Leaner Sharp for 2026

The era of Sharp as a global "panel titan" effectively concludes with the April 1, 2026, absorption of its display subsidiary back into the parent corporation. This merger serves as the final seal on the "Asset-Light" strategy mandated by Foxconn, shifting Sharp from a capital-intensive manufacturer to a high-margin Brand and Solutions provider.

By the second half of 2026, Sharp’s footprint will be defined by a permanent exit from the volatility of mass-market LCD fabrication. The Sakai site, once the pinnacle of Gen 10 engineering, has been fully decoupled from Sharp's operations to serve as a national AI hub for SoftBank and KDDI. Similarly, the transfer of Kameyama No. 2 to Foxconn removes a significant financial burden from Sharp’s balance sheet.

What remains is a highly specialized "two-fab" core: the Hakusan plant, secured by its strategic role in Apple’s supply chain, and Kameyama No. 1, Sharp’s final proprietary stronghold for high-margin automotive and medical glass. Sharp has traded its former 20% global market share for a more stable existence where its value lies in intellectual property and branding, delivering specialized AIoT and workplace technologies that rely on a global supply chain rather than the massive, high-risk factories of its past and the whims of a formerly recalcitrant management. There is no guarantee this ‘new’ Sharp will ultimately be successful, but much of the financial burden of the display segment has been removed. Now it is up to the current management to make a more specialized Sharp regain some of its former glory.

Rumors have been circulating in Japan that Sharp (6753.JP) plans to close its Yonago’ subsidiary as part of its continuing restructuring effort under the leadership of Foxconn (2354.TT), who holds a 66% controlling stake in Sharp. The press hinted that this would lead to the closing of one of Sharp’s small panel fabs, however the Yonago facilities are not panel producers but assemblers, taking raw panels (typically open cell) and adapting them for specific applications or purposes.

The Survival of Kameyama #1 & the Survival of Kameyama #2

We expect Sharp will still maintain LCD panel production at its Kameyama #1 fab, which produces automotive displays, ruggedized displays, displays for medical devices, and POS/ATM displays. Sharp also operates a Gen 6 fab in Hakusan, but that fab was partially financed by Apple (AAPL) and is not owned by Foxconn. Sharp closed its Kameyama #2 fab (still producing small amounts until later this year), which will become an AI server production facility and an EV parts manufacturing plant after it winds down its last obligations.

The Hakusan Fab: A Strategic Partnership with Apple

As mentioned above, Sharp technically also owns a Gen 6 plant in Hakusan which it purchased from Japan Display (6740.JP) in 2020 for $390 million, however while Sharp owns the real estate, Apple owns much of the specialized equipment in the fab, making it a dedicated fab for small/medium Apple devices. Sharp also maintains a Micro-LED pilot line at the Hakusan plant and Foxconn (not Sharp) owns a Gen 10.5 LCD TV panel plant in Guangzhou, which continues to operate, producing TV panels.

The Legacy of Sakai: From LCD Pioneer to AI Data Center

Sharp has had a rocky career in the display space. As one of the first LCD display developers, building screens for calculators and handheld devices, Sharp built its first LCD plant in Tenri, Japan back in 1973, even before they had ‘generation’ designations for substrate sizes.. This was followed by R&D lines and the company’s first Gen 1 fab in 1991 and a Gen 3 fab in 1995. But the real expansion took place in the 2000’s with Sharp’s Gen 4 Mie #3 plant (2003), Kameyama #1 (Gen 6) in 2004, Kameyama #2 (Gen 8) in 2006, and under the heading of ‘Bigger is Better’, Sharp began building some of the largest and most modern LCD fabs in 2009, culminating in the construction of the first Gen 10 LCD fab in Sakai in 2009. This plant was considered the most sophisticated in the world, but arrived just as TV set demand was declining, and while a technical marvel at the time, was a burden for Sharp in the 2010 to 2020 time frame. The plant was closed and sold to Softbank (9434.JP) (459,999 m2 for ~$676 million) and KDDI (9433.JP) (former color filter plant ~33,000m2 for $68 million). The facilities are to be used for AI training and agent hosting.

In 2016 Foxconn’s purchased its controlling stake in Sharp after years of Sharp’s losses in the display space and began the era of a more ‘asset light’ Sharp, eventually leading to what will be Sharp’s position in the middle of this year, a much smaller company with two fabs, and a more diverse product portfolio that is far less dependent on internal product production. In fact Sharp will have only two remaining fabs by the end of this year, the Hakusan fab that produces small panel displays for Apple, and the Kameyama #1 fab that produces automotive and medical displays, a far cry from twenty years ago when Sharp was the leading producer of LCD displays worldwide (15% to 20% share depending on the quarter) and the leading brand in North America, beating out rivals Samsung Electronics (005930.KS) and Sony (SNE).

Conclusion – A Leaner Sharp for 2026

The era of Sharp as a global "panel titan" effectively concludes with the April 1, 2026, absorption of its display subsidiary back into the parent corporation. This merger serves as the final seal on the "Asset-Light" strategy mandated by Foxconn, shifting Sharp from a capital-intensive manufacturer to a high-margin Brand and Solutions provider.

By the second half of 2026, Sharp’s footprint will be defined by a permanent exit from the volatility of mass-market LCD fabrication. The Sakai site, once the pinnacle of Gen 10 engineering, has been fully decoupled from Sharp's operations to serve as a national AI hub for SoftBank and KDDI. Similarly, the transfer of Kameyama No. 2 to Foxconn removes a significant financial burden from Sharp’s balance sheet.

What remains is a highly specialized "two-fab" core: the Hakusan plant, secured by its strategic role in Apple’s supply chain, and Kameyama No. 1, Sharp’s final proprietary stronghold for high-margin automotive and medical glass. Sharp has traded its former 20% global market share for a more stable existence where its value lies in intellectual property and branding, delivering specialized AIoT and workplace technologies that rely on a global supply chain rather than the massive, high-risk factories of its past and the whims of a formerly recalcitrant management. There is no guarantee this ‘new’ Sharp will ultimately be successful, but much of the financial burden of the display segment has been removed. Now it is up to the current management to make a more specialized Sharp regain some of its former glory.

RSS Feed

RSS Feed