October Display Panel Shipments Fall 15.8%: Market Shifts to Profit-First Strategy

The Outlook

On a longer-term basis, we expect 2026 to be a mixed year, with display shipment growth within a range between -2.4% and +0.5%, with the lean toward the negative. This will reflect on panel producer utilization rates, which we expect to be lower than this year, especially early in the year. We do expect area growth in 2026 to be between 2.5% and 3.7% as ultra-large displays (~100”) grow as a percentage, but we caution that we expect average area growth to slow over the next few years as physical limitations keep ultra-large sets from growing larger. On the plus side of the average panel area equation is less fab depreciation and cost reductions for Ultra-large panels, which should make them more viable to the average customer. On the minus side are the physical size limitations that these panels require.

Conclusion: Display Panel Market Shifts to Rational Supply Management Amid Demand Volatility

The October display panel shipment data reflects a swift correction in the consumer electronics (CE) market, shifting from two months of unusual strength to a sharp 15.8% month-over-month decline. This drawdown was driven by a combination of weakening consumer spending and an inventory correction by CE brands that had over-ordered in prior months.

Crucially, the response from dominant panel producers, particularly in China, signals the continuation of a strategic pivot toward rational supply management. By reducing fab utilization instead of aggressively cutting prices to maintain market share, a past practice enabled by generous government subsidies, manufacturers are prioritizing stable profitability over volume at all costs. This is a fundamental change in market dynamics, suggesting a healthier, more mature industry outlook less susceptible to catastrophic price collapse or sharp upward movement.

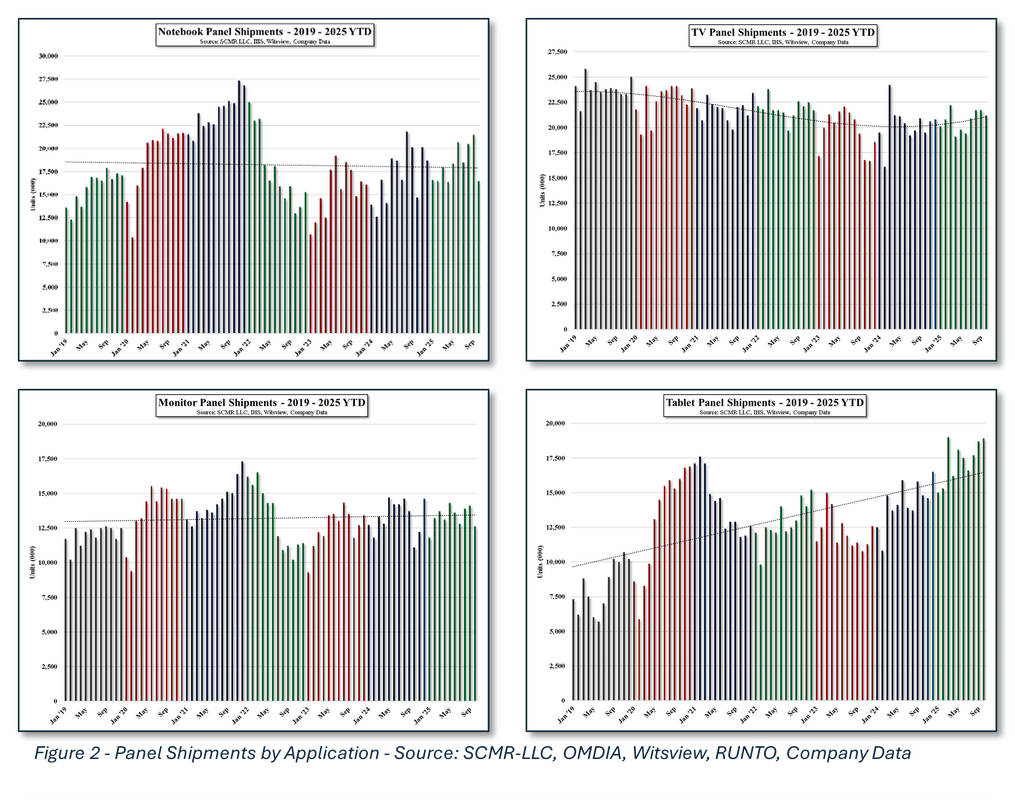

Looking ahead, the market faces a mixed-growth environment in the longer term. While unit shipments are forecast to see minimal to negative growth in 2026, the Area Shipment metric is expected to show positive growth (2.5% to 3.7%). This divergence confirms the continuing trend of larger-sized displays (e.g., 100" ultra-large TVs) driving the average yearly panel size higher, albeit with physical and cost limitations keeping some of that growth in check..

We focus on this trade-off: weak unit demand points to consumer conservatism, but the strategic reduction in supply and persistent area growth indicates a disciplined market structure that is better equipped to support panel maker financials despite the cyclical headwinds. While we expect these factors to support a more stable display space in 2026 real consumer demand will drive shipments with a somewhat negative outlook for the 1st quarter. Inventory levels coming out of the Christmas/New Year holidays will play into that equation, but we are still to early into the holiday season to estimate early 2026 inventory levels.

Conclusion: Display Panel Market Shifts to Rational Supply Management Amid Demand Volatility

The October display panel shipment data reflects a swift correction in the consumer electronics (CE) market, shifting from two months of unusual strength to a sharp 15.8% month-over-month decline. This drawdown was driven by a combination of weakening consumer spending and an inventory correction by CE brands that had over-ordered in prior months.

Crucially, the response from dominant panel producers, particularly in China, signals the continuation of a strategic pivot toward rational supply management. By reducing fab utilization instead of aggressively cutting prices to maintain market share, a past practice enabled by generous government subsidies, manufacturers are prioritizing stable profitability over volume at all costs. This is a fundamental change in market dynamics, suggesting a healthier, more mature industry outlook less susceptible to catastrophic price collapse or sharp upward movement.

Looking ahead, the market faces a mixed-growth environment in the longer term. While unit shipments are forecast to see minimal to negative growth in 2026, the Area Shipment metric is expected to show positive growth (2.5% to 3.7%). This divergence confirms the continuing trend of larger-sized displays (e.g., 100" ultra-large TVs) driving the average yearly panel size higher, albeit with physical and cost limitations keeping some of that growth in check..

We focus on this trade-off: weak unit demand points to consumer conservatism, but the strategic reduction in supply and persistent area growth indicates a disciplined market structure that is better equipped to support panel maker financials despite the cyclical headwinds. While we expect these factors to support a more stable display space in 2026 real consumer demand will drive shipments with a somewhat negative outlook for the 1st quarter. Inventory levels coming out of the Christmas/New Year holidays will play into that equation, but we are still to early into the holiday season to estimate early 2026 inventory levels.

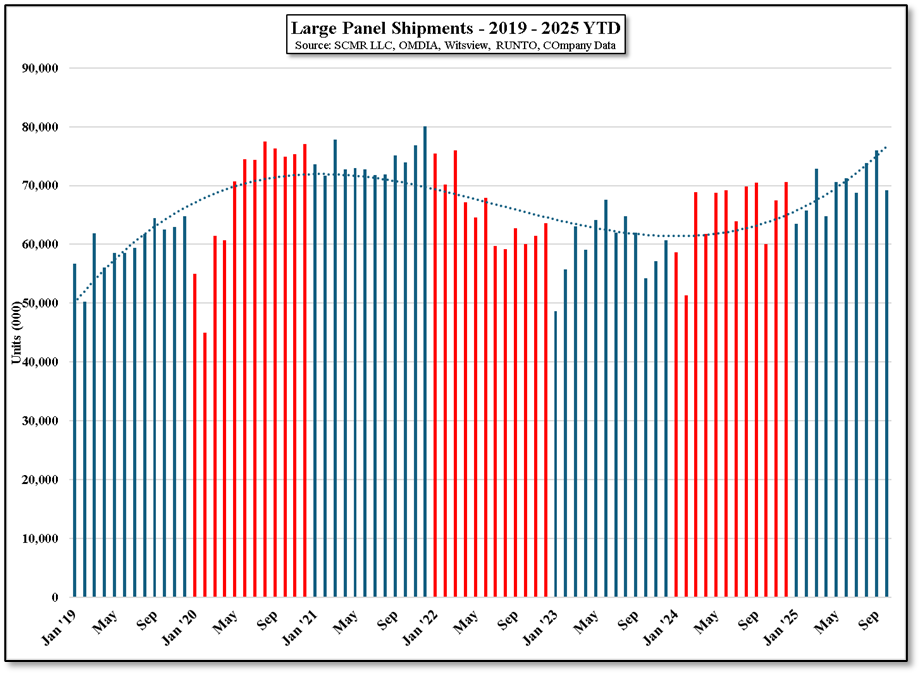

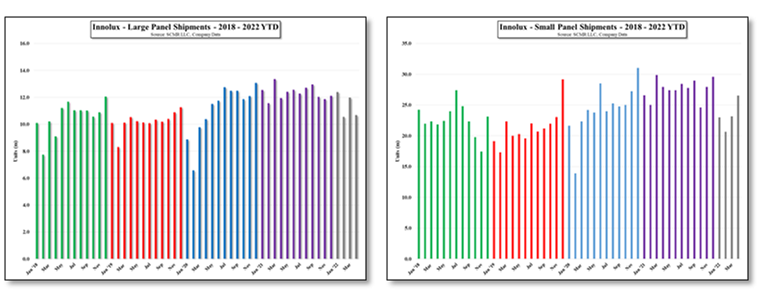

Figure 1 - Large Panel Shipments - 2019 - 2025 YTD - Source: SCMR-LLC, OMDIA, Witsview, RUNTO, Company Data

RSS Feed

RSS Feed