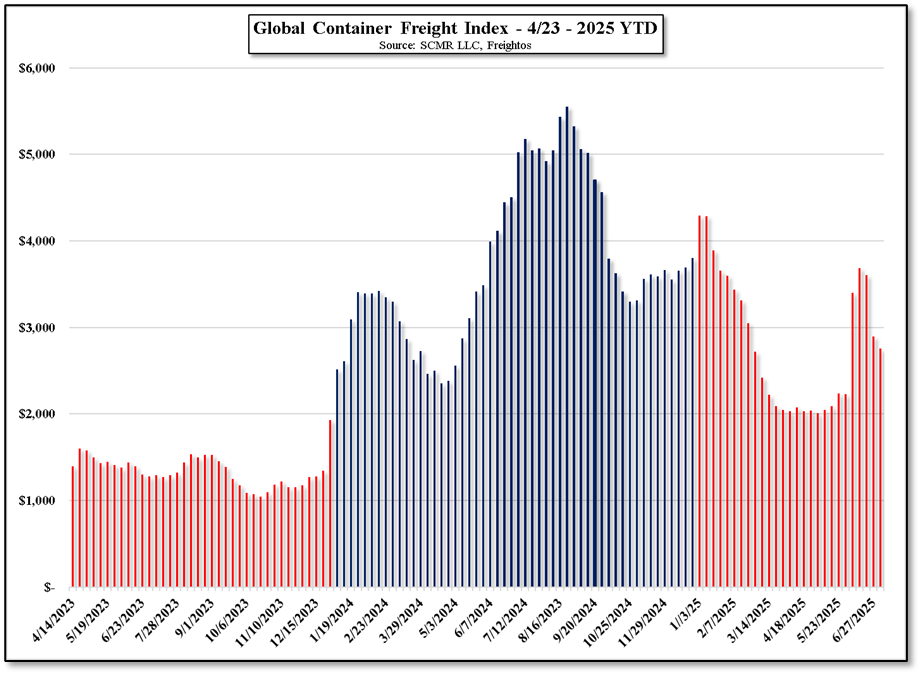

A Fragile Equilibrium: How the SCOTUS Tariff Intervention Blocked the Energy Cascade

As always, we pay particular attention to display panel prices as they are the front-line of the CE product pricing cycle. While memory price increases have taken center stage in recent months, the display panel percentage of BOM for laptops ranges from 20% to 25%, for TV sets, between 40% and 50%, and for monitors, over 60%, making them a key determinant in the CE product pricing model. That said, we are currently at an unusual juncture, with a number of “one-time” factors playing into that equation, with panel prices only one factor in what has become a much more complex pricing architecture.

The Subsidized Squeeze: Chinese New Year and the 85-inch Shift

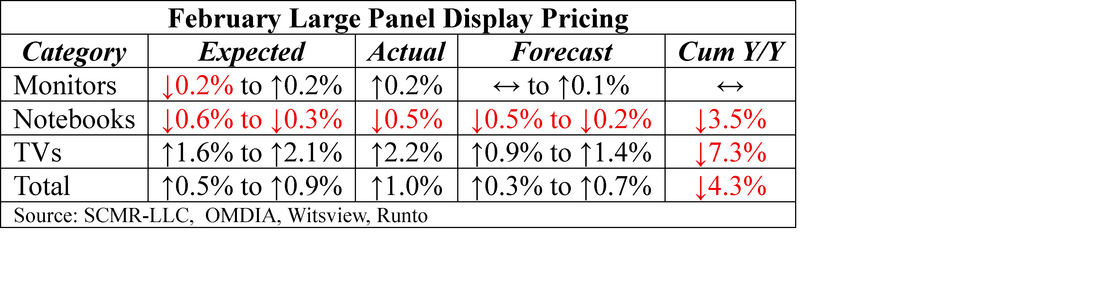

February saw only modest moves in IT panel prices (Monitors and Notebooks), while TV panel prices settled slightly above our expected range. We believe this is a result of the utilization cuts that panel producers made during the Chinese New Year holiday, tightening supply and generating enough unease among panel buyers that they were willing to pay higher prices to build TV panel inventory. While demand remains relatively static globally, better than expected premium TV set sales in China during the holiday, spurred by the renewal of “New for Old” government subsidies, pushed panel buyers to refill depleted panel inventory. This was primarily felt in panel sizes 85” and above but pushed panel producers away from more conventional sizes (<85”), reducing supply and raising prices. We expect this to continue into March but to a lesser degree as demand remains flat as the Chinese subsidy momentum subsides.

February saw only modest moves in IT panel prices (Monitors and Notebooks), while TV panel prices settled slightly above our expected range. We believe this is a result of the utilization cuts that panel producers made during the Chinese New Year holiday, tightening supply and generating enough unease among panel buyers that they were willing to pay higher prices to build TV panel inventory. While demand remains relatively static globally, better than expected premium TV set sales in China during the holiday, spurred by the renewal of “New for Old” government subsidies, pushed panel buyers to refill depleted panel inventory. This was primarily felt in panel sizes 85” and above but pushed panel producers away from more conventional sizes (<85”), reducing supply and raising prices. We expect this to continue into March but to a lesser degree as demand remains flat as the Chinese subsidy momentum subsides.

The Energy Tax: Crude Volatility and Carrier Surcharges

As of As of March 13, the 'short-term effects of the oil situation' have manifested in a new layer of costs. Major carriers have enacted an Emergency Fuel Surcharge (EFS), roughly $150–$160 per container for long-haul routes, to account for Brent Crude breaching the $100/bbl. mark following the closure of the Strait of Hormuz. For a 65” TV, this adds a non-negotiable $0.76 per unit to the landed cost before it reaches a US port.

Chipflation 2.0: AI-Driven Shortages in the Smart TV BOM

From the BOM perspective, since the end of 2025 component prices have continued to climb, particularly memory and advanced packaging products., and while TV sets use significantly less memory than laptops, the push toward HBM (high Bandwidth Memory) used for AI has left commodity memory like the DDR4 used in TVs in short supply.. Even though contract prices were up 4x last year, they have already risen almost 60% in 1Q of this year. This has pushed memory, as a percentage of BOM, from 2.5% of manufacturing cost last year to over 7% as of the end of this month.

In addition, the demand (again AI) for CoWoS (Chip on Wafer on Substrate) components has made it more difficult to maintain a consistent supply of SoC’s used in TV video processors, especially at entry and mid-price tiers. This has caused a ~15% increase in the cost of SoC’s used for video processing due to a lack of advanced packaging materials. Further, the oil issue has even deeper ramifications at $100/bbl. as a feedstock to the plastic resins that form TV set chassis. This will add another ‘soft cost’ to the BOM of ~$3.00.

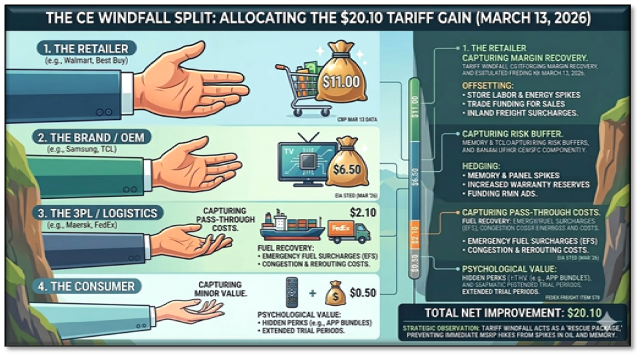

The $20.10 Anomaly: Quantifying the Tariff/Energy Trade-Off

That said, the surprise here is that when we do an analysis of all the puts and takes that affect the CE space over the last 30 days, the buyer of a 65” LCD TV should have seen a theoretical $20.10 reduction in price, even with the price of both oil and memory increasing (and panels) during the period. The Customs Bureau stopped collecting the IEEPA tariffs on February 20, roughly a 23% (high-volume CE imports) levy, replacing it with a 10% global flat-rate tariff that will last for 150 days (7/24/26). In terms of our 65” TV, that change had a larger dollar value than all of the component and logistic increases, netting out to a positive $20.10 swing. Simply, the tariff windfall ($32.50) far outweighed the energy/logistics/BOM drag ($12.10).

The Capture Conflict: Who Gets the Windfall?

Of course, the consumer will likely not see most of that theoretical improvement in price as there are a multitude of outstretched hands that come first in the CE supply chain.

As of As of March 13, the 'short-term effects of the oil situation' have manifested in a new layer of costs. Major carriers have enacted an Emergency Fuel Surcharge (EFS), roughly $150–$160 per container for long-haul routes, to account for Brent Crude breaching the $100/bbl. mark following the closure of the Strait of Hormuz. For a 65” TV, this adds a non-negotiable $0.76 per unit to the landed cost before it reaches a US port.

Chipflation 2.0: AI-Driven Shortages in the Smart TV BOM

From the BOM perspective, since the end of 2025 component prices have continued to climb, particularly memory and advanced packaging products., and while TV sets use significantly less memory than laptops, the push toward HBM (high Bandwidth Memory) used for AI has left commodity memory like the DDR4 used in TVs in short supply.. Even though contract prices were up 4x last year, they have already risen almost 60% in 1Q of this year. This has pushed memory, as a percentage of BOM, from 2.5% of manufacturing cost last year to over 7% as of the end of this month.

In addition, the demand (again AI) for CoWoS (Chip on Wafer on Substrate) components has made it more difficult to maintain a consistent supply of SoC’s used in TV video processors, especially at entry and mid-price tiers. This has caused a ~15% increase in the cost of SoC’s used for video processing due to a lack of advanced packaging materials. Further, the oil issue has even deeper ramifications at $100/bbl. as a feedstock to the plastic resins that form TV set chassis. This will add another ‘soft cost’ to the BOM of ~$3.00.

The $20.10 Anomaly: Quantifying the Tariff/Energy Trade-Off

That said, the surprise here is that when we do an analysis of all the puts and takes that affect the CE space over the last 30 days, the buyer of a 65” LCD TV should have seen a theoretical $20.10 reduction in price, even with the price of both oil and memory increasing (and panels) during the period. The Customs Bureau stopped collecting the IEEPA tariffs on February 20, roughly a 23% (high-volume CE imports) levy, replacing it with a 10% global flat-rate tariff that will last for 150 days (7/24/26). In terms of our 65” TV, that change had a larger dollar value than all of the component and logistic increases, netting out to a positive $20.10 swing. Simply, the tariff windfall ($32.50) far outweighed the energy/logistics/BOM drag ($12.10).

The Capture Conflict: Who Gets the Windfall?

Of course, the consumer will likely not see most of that theoretical improvement in price as there are a multitude of outstretched hands that come first in the CE supply chain.

Figure 1 - Data Insight: A Perfect Offset - Source: SCMR-LLC, Nano-Banana 2

We note that this infographic is good for today only, as any extension of the oil price rise will erode the tariff benefits, but we do note that while the oil situation is certainly a crucial one that has a widespread effect across the entire CE supply chain, the tariff issue has a longer-term effect that gives brands margin flexibility that they did not have coming into this year. Whether they capture it internally to boost profitability or use it to boost sales remains a big, and as of yet unanswered question, but we expect while all supply chain participants are aware of the impact of the tariff change, they are currently more focused on the short-term effects of the oil situation.

Conclusion: The 150-Day Margin Buffer

In a standard year, the simultaneous rise of $100/bbl crude, a 60% memory spike, and higher-than-expected panel prices would have mandated a significant MSRP hike for the US 65” TV market. However, the February 20 Supreme Court ruling has provided the industry with a temporary, yet substantial, "get out of jail free" card.

By replacing a 23% IEEPA levy with a 10% Section 122 duty, the administration has inadvertently created a $20.10 per-unit margin cushion. This windfall is currently acting as a silent stabilizer, absorbing the $12.10 logistics and BOM drag that would otherwise have crashed into retail price points.

The critical question for the next quarter is one of duration. With Section 122 set to expire on July 24, 2026, and the USTR already pivoting toward new Section 301 investigations, this margin buffer is likely a "150-day anomaly." We expect brands to maintain current price rigidity, ignoring the theoretical $20.10 consumer savings, to build a war chest for a potentially more expensive H2 2026. For now, the supply chain isn’t fighting for the consumer’s dollar; it is fighting to capture a piece of the SCOTUS-driven windfall before energy and labor spikes eat it alive.

Conclusion: The 150-Day Margin Buffer

In a standard year, the simultaneous rise of $100/bbl crude, a 60% memory spike, and higher-than-expected panel prices would have mandated a significant MSRP hike for the US 65” TV market. However, the February 20 Supreme Court ruling has provided the industry with a temporary, yet substantial, "get out of jail free" card.

By replacing a 23% IEEPA levy with a 10% Section 122 duty, the administration has inadvertently created a $20.10 per-unit margin cushion. This windfall is currently acting as a silent stabilizer, absorbing the $12.10 logistics and BOM drag that would otherwise have crashed into retail price points.

The critical question for the next quarter is one of duration. With Section 122 set to expire on July 24, 2026, and the USTR already pivoting toward new Section 301 investigations, this margin buffer is likely a "150-day anomaly." We expect brands to maintain current price rigidity, ignoring the theoretical $20.10 consumer savings, to build a war chest for a potentially more expensive H2 2026. For now, the supply chain isn’t fighting for the consumer’s dollar; it is fighting to capture a piece of the SCOTUS-driven windfall before energy and labor spikes eat it alive.

RSS Feed

RSS Feed