Elemental Economics: A 2026 Outlook on Passive Component Price Volatility

The "Rodney Dangerfield" of Electronics: Why Passive Components Get No Respect

Consume electronics’ components are the Rodney Dangerfield’s of the CE space, they get no respect. Of course there are the superstars, microprocessors, that get most of the publicity, and an occasional flash-in-the-pan component, such as memory might be currently, but the average component is rarely mentioned and must work tirelessly behind the scenes each day to make sure your CE product works properly. Resistors, capacitors, inductors and the like populate the lesser slots on PC boards while processors get special heat sinks, fans, and highly refined power even though they are nothing without those rank and file components.

Shifting Tides: Moving Beyond Typical Pricing Fluctuations

We are used to hearing about higher costs relative to those flashy devices mentioned above but despite their proliferation across all CE devices those lowly components rarely are the cause for pricing concerns. There are spates of panic buying and short-term logistical issues that push up simple component prices, but we are beginning to sense that what we have seen most recently is more than just the more typical ups and downs of component pricing.

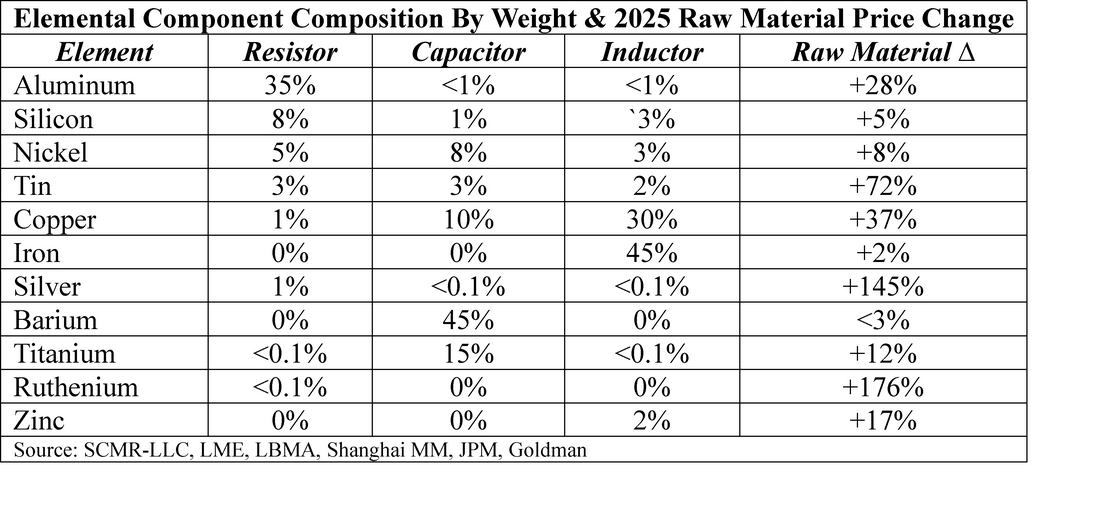

Elemental Breakdown: Component Composition by Weight and Raw Material Costs

Looking at the three component[1] categories, we can break down their component elemental weights and the price increases seen in 2025 for each elemental raw material..

[1] For this note, unless otherwise indicated, we are using standard 0603/0805 resistors, MLCCs (Multi-layer Ceramic Capacitors), and wire-wound inductors.

Consume electronics’ components are the Rodney Dangerfield’s of the CE space, they get no respect. Of course there are the superstars, microprocessors, that get most of the publicity, and an occasional flash-in-the-pan component, such as memory might be currently, but the average component is rarely mentioned and must work tirelessly behind the scenes each day to make sure your CE product works properly. Resistors, capacitors, inductors and the like populate the lesser slots on PC boards while processors get special heat sinks, fans, and highly refined power even though they are nothing without those rank and file components.

Shifting Tides: Moving Beyond Typical Pricing Fluctuations

We are used to hearing about higher costs relative to those flashy devices mentioned above but despite their proliferation across all CE devices those lowly components rarely are the cause for pricing concerns. There are spates of panic buying and short-term logistical issues that push up simple component prices, but we are beginning to sense that what we have seen most recently is more than just the more typical ups and downs of component pricing.

Elemental Breakdown: Component Composition by Weight and Raw Material Costs

Looking at the three component[1] categories, we can break down their component elemental weights and the price increases seen in 2025 for each elemental raw material..

[1] For this note, unless otherwise indicated, we are using standard 0603/0805 resistors, MLCCs (Multi-layer Ceramic Capacitors), and wire-wound inductors.

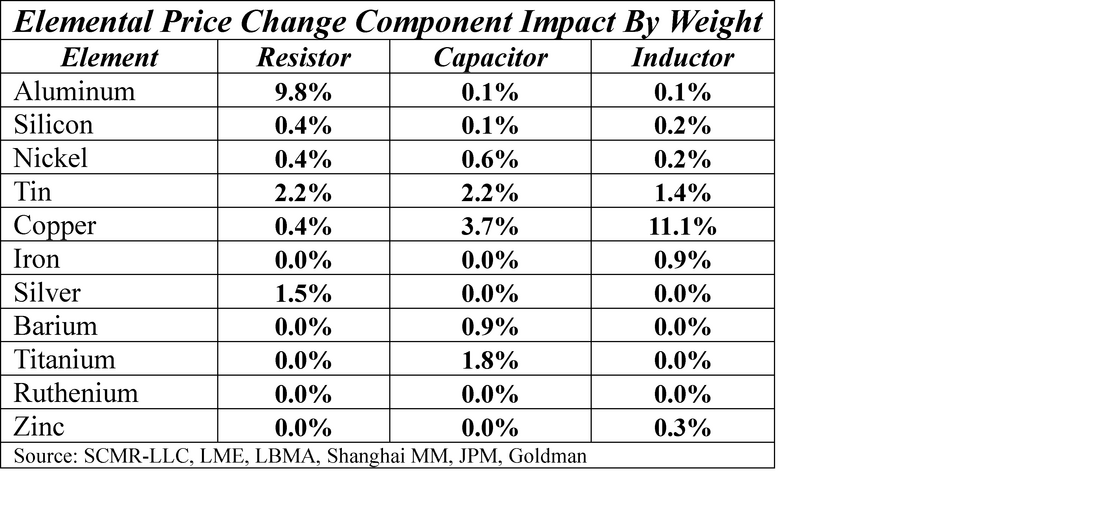

Calculating the Economic Impact: Why Weight Does Not Equal Cost

Carrying it a bit further we calculate the impact of each element of the three component classes by weight by multiplying the weight percentage by the change in price.

Carrying it a bit further we calculate the impact of each element of the three component classes by weight by multiplying the weight percentage by the change in price.

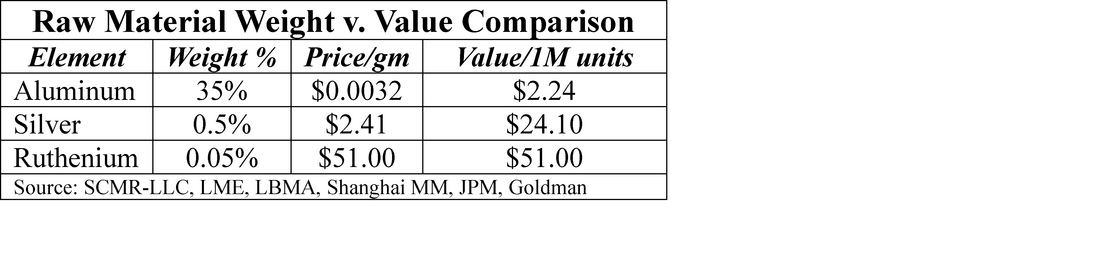

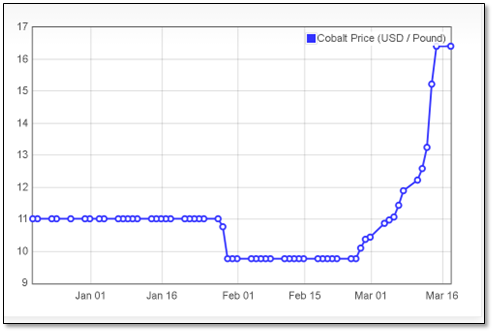

While some of these changes are significant, such as copper for inductors or aluminum for resistors, this math downplays the impact of a number of elements, such as silver and ruthenium that had extremely large price increases last year. The economic impact of these price increases is considerably greater as mass does not equal cost which we show here for three of the more volatile elements in a resistor.

While there is 700 times more aluminum in a resistor than ruthenium by weight, the ruthenium is 22 times more expensive than the aluminum content based on total dollar value. This means that the impact of the 35% price increase for aluminum has only a 0.03% impact on the final resistor price, while the ruthenium and silver price increases are what is driving up the cost of the components.

2026 Forecast: Price Trajectories for Resistors, Inductors, and MLCCs

2026 Forecast: Price Trajectories for Resistors, Inductors, and MLCCs

- Resistors - Based on the total value calculation for resistors, we expect a 10% to 15% increase in price this year. Even in power resistors which have large aluminum heat sinks, the cost impact of the 35% price rise in aluminum is still under 3%.

- Inductors – Heavily composed of iron and copper by weight, inductors are less impacted by some of the larger trace element increases. Based on a total value calculation we would expect inductors to see a ~5% to 6% increase.

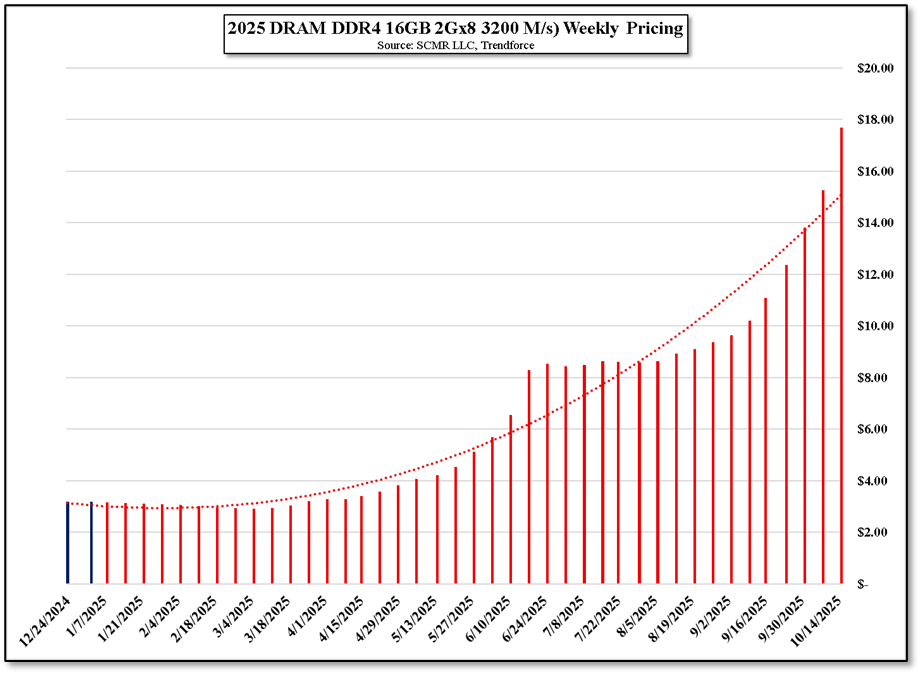

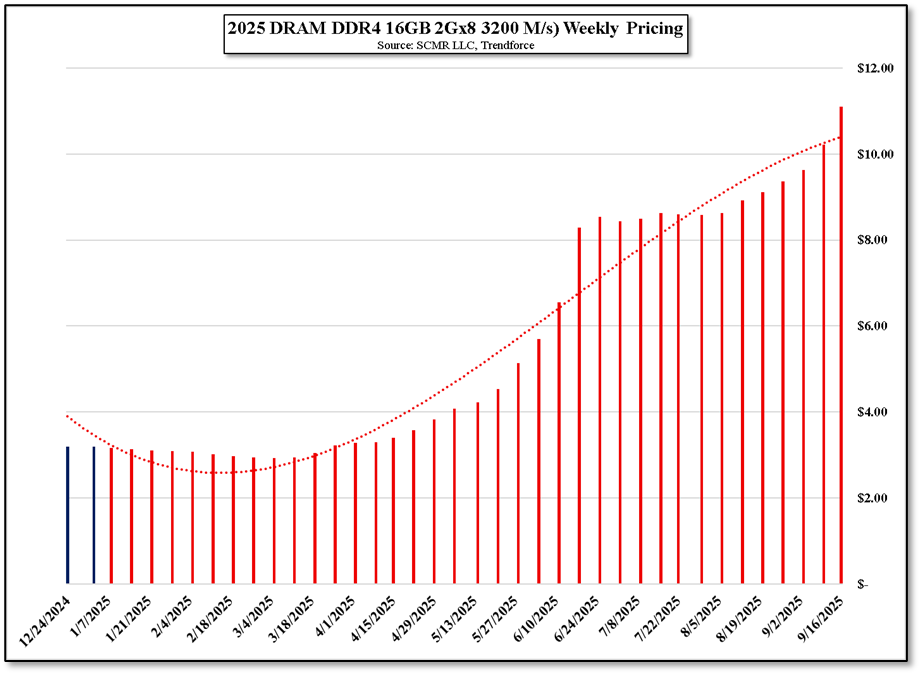

- Capacitors (MLCC) - Using the same metrics, capacitor costs would have absorbed a ~15% cost increase based on raw material price increases in 2025, but there is another factor that will likely push that number higher, perhaps as high as 25%, and that is a lack of availability. As we have mentioned in earlier notes, MLCC production is relatively static but has faced unusually strong demand from the AI server space where Nvidia (NVDA) Blackwell chipsets use as many as 10,000 MLCCs per board. This has pulled capacity from more standard clients which we expect to continue this year, leading to expectations for MLCC price increases above the 15% based on raw material prices alone.

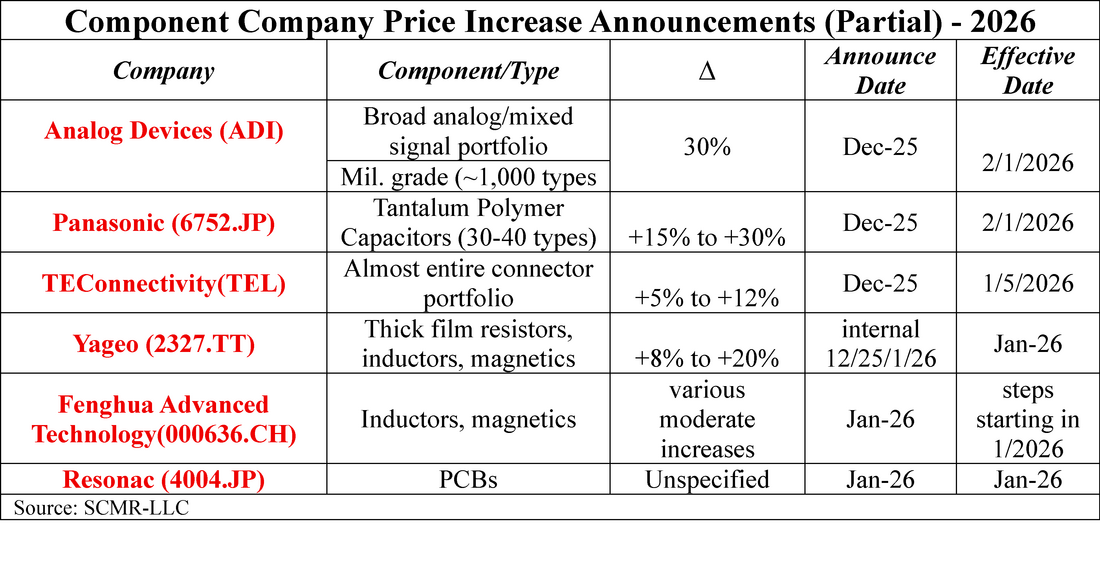

Although we are not always privy to internal pricing memos there have been a number of price announcements made concerning components either late last year or in January, with most taking place immediately or sometime in 1Q ’26. This is a partial list primarily from companies that have made public announcements or made notifications to distributors.

Conclusion: The End of the "Commodity Complacency" Era

The data reveals a stark new reality for the consumer electronics supply chain: the era of "lowly" components providing a stable, low-cost backbone is over. For decades, procurement teams focused their negotiation energy on high-value silicon, treating resistors, capacitors, and inductors as rounding errors in the Bill of Materials (BOM). In 2026, that "Rodney Dangerfield" lack of respect has met a hard floor of elemental economics.

We are no longer dealing with typical cyclical fluctuations. The convergence of record-breaking precious metal costs (Ruthenium and Silver) and structural demand shifts (AI servers consuming 10,000 MLCCs per board) has decoupled component pricing from historical norms.

The data reveals a stark new reality for the consumer electronics supply chain: the era of "lowly" components providing a stable, low-cost backbone is over. For decades, procurement teams focused their negotiation energy on high-value silicon, treating resistors, capacitors, and inductors as rounding errors in the Bill of Materials (BOM). In 2026, that "Rodney Dangerfield" lack of respect has met a hard floor of elemental economics.

We are no longer dealing with typical cyclical fluctuations. The convergence of record-breaking precious metal costs (Ruthenium and Silver) and structural demand shifts (AI servers consuming 10,000 MLCCs per board) has decoupled component pricing from historical norms.

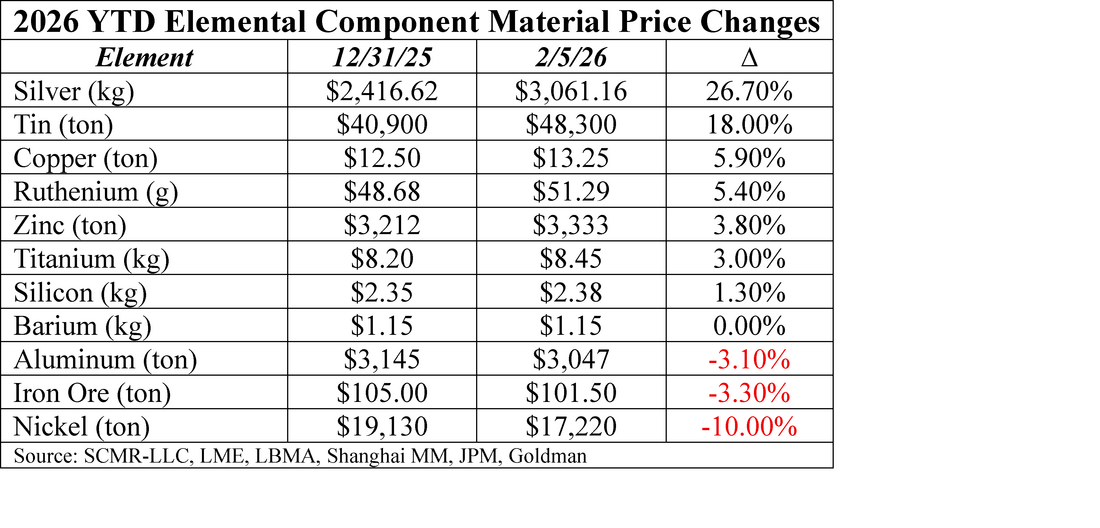

- Resistors: While physically light, their reliance on "trace superstars" like Ruthenium (+176%) and Silver (+145%) has turned them into the most volatile passive component. Manufacturers like Yageo and Fenghua have already breached the 20% price hike threshold this February to defend their margins against these metal surges.

- Capacitors (MLCCs): The 15% raw material impact is merely the baseline. The true driver for 2026 is Capacity Displacement. As tier-one suppliers pivot production to high-margin AI and Automotive "Super-Caps," standard consumer-grade clients are facing a "new and more competitive supply reality: stable-to-soft pricing for legacy parts, but sharp 25%+ premiums for high-capacity components due to simple unavailability.

- Inductors: Heavily weighted toward Copper (+37%) and Tin (+72%), these components are the most "honest" reflections of the industrial metal market. With copper hitting record highs of $13,300/ton in early 2026, the ~5% to 6% price increases we projected are likely a conservative floor.

RSS Feed

RSS Feed