It’s the Little Things…

Microprocessors get all the press, with their billions of transistors squeezed into a tiny piece of silicon, but who does all the real work these days? Its us, the passive components that serve and protect the microprocessor and its fancy TSVs, 3D stacking, and metal highways. We do all the work and they get all the glory, but it hasn’t felt so good when you microprocessors have to sit on the shelf because manufacturers have to wait months to get us lowly passive components. Yeah, we only cost a few pennies but there is usually only one microprocessor and hundreds or thousands of us passives in a system, so without us there is no system. Okay, we are anthropomorphizing passive components, but these simple components are the traffic cops, bus drivers, and garbage collectors for many CE devices and while they seem immaterial when compared to transistors and the complex systems they can be molded into, they are as necessary to those systems as water is to humans.

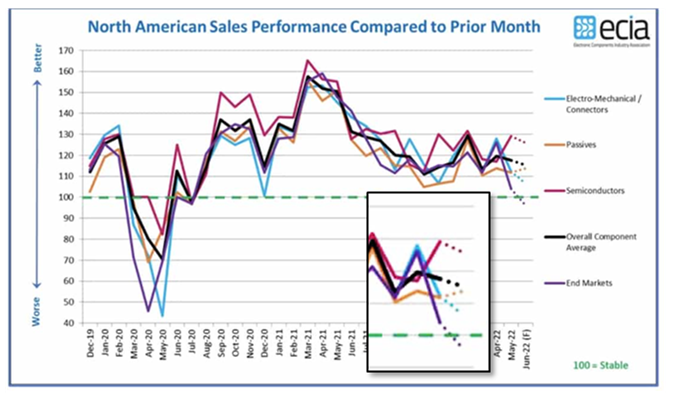

The ECIA (Electrical Component Industry Association) surveys its members via an independent 3rd party (Technology Partners Consulting) on a regular basis to get a sense of both sentiment across the components industry and a read on inventory and pricing levels. As this data is for North America, it is not conclusive for the global market but does give some major data points as to where the industry has been and is headed. As can be seen in Figure 2, while m/m sales increases peaked in March of last year, they have remained consistently above the 100 mark, which indicates stable sales gains, however the inset shows that expectations for June, while still above 100 for individual component categories, indicates that the end markets will fall below 100 for the first time since the COVID-19 pandemic began.

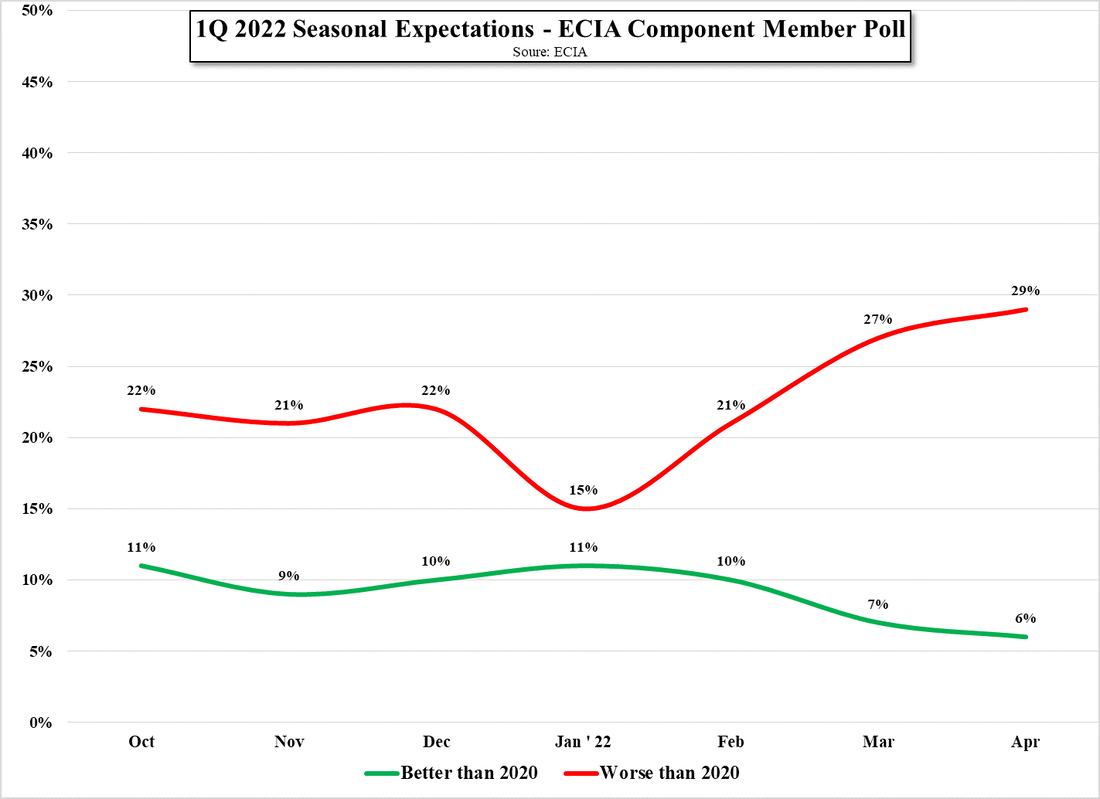

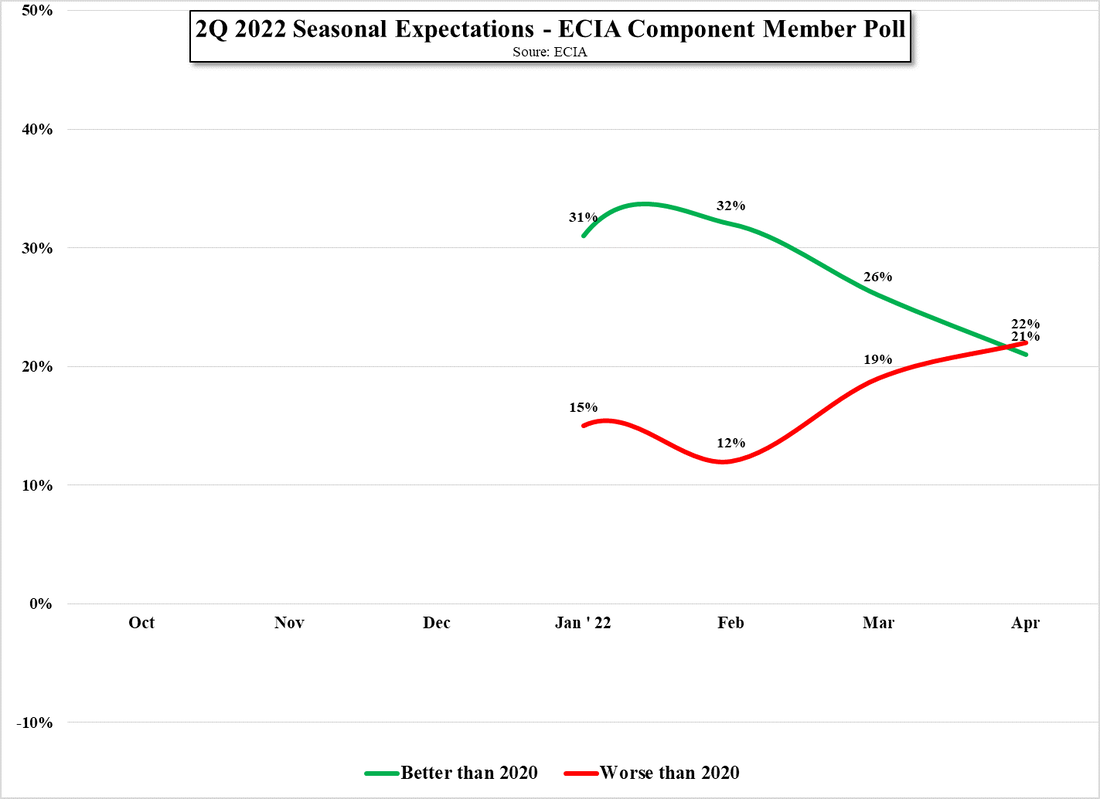

More specifically, as shown in Figure 3 and Figure 4, members were pessimistic about the prospects for sales in 1Q, relative to 2020 and got more pessimistic as the quarter developed, and while that pessimism about 2nd quarter was at a low in January, it continued to rise as 1Q developed. With expectations for the industry expected to fall below 100 in June, it would seem that a positive view of the industry from its members has been replaced with a negative one, although individual component segments, while down in June, have remained above the 100 mark, sort of a “…well the industry is crappy, but we’re still doing o.k….”, with ~90% of respondents indicating they see a book-to-bill of 1 or greater at their company.

We see the worry coming from the fact that while general component inventories are all relatively close to normal for most categories, concern that inventory levels will continue to grow in 2Q is the case for ~45% of respondents, while only 8% expect those levels to decline. These metrics are actually down from those heading into 1Q, but component inventory levels were artificially low early this year as supply chain issues and high raw material prices limited the supply of a number of components, both active and passive. Since then supply pressure has eased a bit and component suppliers have tried to normalized shipments, but are concerned that seasonal factors will make it necessary to build inventory further without underlying demand.

All in, component suppliers remain pessimistic about the state of the industry but seem to be more optimistic about their individual segments. In most cases raw material and energy prices continue to rise and with component inventories at normal levels, it becomes more difficult to pass on price increases, so the carrying cost of potentially higher inventories becomes more of a burden in 2Q and potentially 3Q, while demand returns to more modest pre-COVID 19 levels. We believe this is the basis for the industry pessimism seen above but with sales remaining above the 100 line for most component segments each seems to have a more positive view of their own segment than the industry overall.

The ECIA (Electrical Component Industry Association) surveys its members via an independent 3rd party (Technology Partners Consulting) on a regular basis to get a sense of both sentiment across the components industry and a read on inventory and pricing levels. As this data is for North America, it is not conclusive for the global market but does give some major data points as to where the industry has been and is headed. As can be seen in Figure 2, while m/m sales increases peaked in March of last year, they have remained consistently above the 100 mark, which indicates stable sales gains, however the inset shows that expectations for June, while still above 100 for individual component categories, indicates that the end markets will fall below 100 for the first time since the COVID-19 pandemic began.

More specifically, as shown in Figure 3 and Figure 4, members were pessimistic about the prospects for sales in 1Q, relative to 2020 and got more pessimistic as the quarter developed, and while that pessimism about 2nd quarter was at a low in January, it continued to rise as 1Q developed. With expectations for the industry expected to fall below 100 in June, it would seem that a positive view of the industry from its members has been replaced with a negative one, although individual component segments, while down in June, have remained above the 100 mark, sort of a “…well the industry is crappy, but we’re still doing o.k….”, with ~90% of respondents indicating they see a book-to-bill of 1 or greater at their company.

We see the worry coming from the fact that while general component inventories are all relatively close to normal for most categories, concern that inventory levels will continue to grow in 2Q is the case for ~45% of respondents, while only 8% expect those levels to decline. These metrics are actually down from those heading into 1Q, but component inventory levels were artificially low early this year as supply chain issues and high raw material prices limited the supply of a number of components, both active and passive. Since then supply pressure has eased a bit and component suppliers have tried to normalized shipments, but are concerned that seasonal factors will make it necessary to build inventory further without underlying demand.

All in, component suppliers remain pessimistic about the state of the industry but seem to be more optimistic about their individual segments. In most cases raw material and energy prices continue to rise and with component inventories at normal levels, it becomes more difficult to pass on price increases, so the carrying cost of potentially higher inventories becomes more of a burden in 2Q and potentially 3Q, while demand returns to more modest pre-COVID 19 levels. We believe this is the basis for the industry pessimism seen above but with sales remaining above the 100 line for most component segments each seems to have a more positive view of their own segment than the industry overall.

Simple Intel 4004 Microprocessor mask - 1971 - Source:http://alumni.media.mit.edu/~mcnerney/2009-4004/4004-masks-composite.jpg

- North American Components Sales - Source: ECIA

1Q 2022 Seasonal Expectations - ECIA Component Poll - Source: ECIA

2Q 2022 Seasonal Expectations - ECIA Component Poll - Source: ECIA

RSS Feed

RSS Feed