Can’t See the Forest for the Trees

It has not been lost to the press that Apple (AAPL) has been working toward moving more of its product line toward OLED displays, and all sorts of timelines for the iPad, Macbooks, and potentially other products’ OLED adoption have been bandied about. Given that there are only a few potential OLED suppliers who are both qualified by Apple and can deliver the volumes necessary, much of the discussion around Apple’s transition has been concerning Samsung Display (pvt), LG Display, and China’s BOE (200725.CH). With current production of OLED IT panels limited to Gen 6 OLED fabs, all three OLED producers (and some others) have indicated or hinted that they would be making investments in new capacity to support Apple’s transition, of course, without naming Apple itself as a customer.

In order to improve efficiency and volume, there has been considerable speculation that such new facilities would be Gen 8 RGB OLED fabs, which currently do not exist (LG Display has Gen 8 OLED fabs but they use a non-RGB process that is not viable for Apple’s specifications), so considerable R&D has been, and still has to be done to design the equipment necessary to make the transition to Gen 8 OLED production for Apple’s (and others’) IT products.

Up until the beginning of this year, most predictions included Samsung Display starting construction on a Gen 8 RGB OLED fab this year, either converting an idle Gen 8 LCD fab or converting a Gen 6 line to Gen 8. LG Display, while a bit less specific, has been expected to do the same, and BOE, has hinted that they will follow a similar path ‘as the market demands’, but the ever-shifting sands of the CE space have begun to cast askance at those plans and concomitant timelines. The equipment needed to deposit OLED materials on the larger Gen 8 substrates takes considerable R&D to develop, and as we have noted previously, there are only a few companies with the expertise to develop such tools. Sunic Systems (171090.KS) is working with LG Display, and at one time Samsung Display was working with ULVAC (6728.JP) on such tool development, but has since abandon that project, and is looking at the industry leader Canon-Tokki (7751.JP) as a potential Gen 8 deposition tool supplier. However, Canon does not want to bear the cost of the tool’s development, as Gen 8 OLED adoption is still an unknown, and expects Samsung Display to pay for the development as a part of the tool price.

With the objective of reducing costs/m2, a boost to tool costs will eat away at the process BOM, and SDC has been hesitating to place the order with Canon, with a cut-off of the end of 2Q if it is to meet the goal of Gen 8 production for Apple in 2024. But it seems not only has the cost of building out Gen 8 OLED capacity been an issue, but the trade press has taken Apple’s recent Mac sales declines as an omen that is adding additional hesitation to the Gen 8 OLED build-out for all potential participants. We differ.

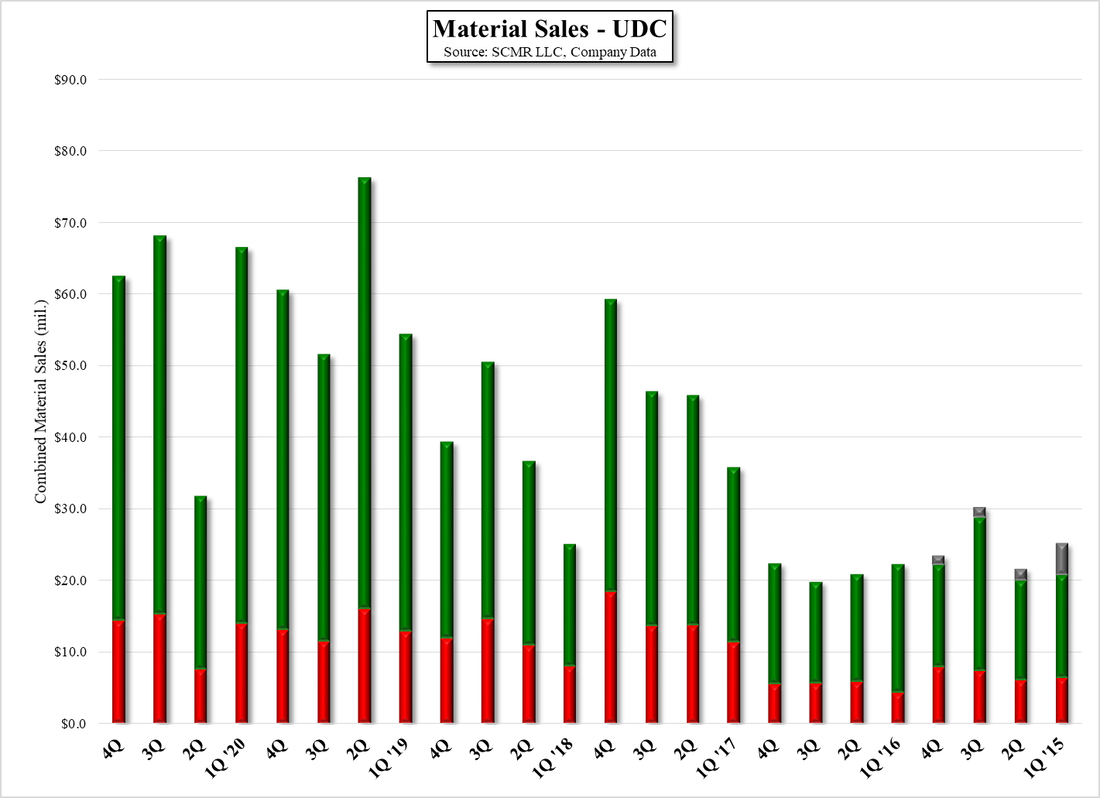

As with almost all CE products, the COVID-19 pandemic changed what was previously a relatively stable demand picture for Apple products. Mobile devices saw some early positive momentum, but the need to communicate online became the driver for tablet, laptop, and PC sales that set volume records. We look at the years between 2020 and 2022 as ‘aberrational’ in terms of demand and look to more normalized unit volumes as a better indicator of what we should expect going forward. In the case of Apple, particularly the Apple Mac, a tool that is known for its use among content developers who require high quality displays, the logic holds that Apple would like to make the transition to OLED for its color purity, high contrast, and color gamut, but recent headlines from overseas are decrying the fact that Apple’s Mac sales are declining and adding to OLED panel producers’ hesitation concerning spending for Gen 8 RGB OLED fabs.

However looking at Apple’s Mac sales going back to 2018, they average $6.35b per quarter, including the heady COVID years, which puts the last two quarters above the LTY average, despite the decline from 2022. More specifically, Apple’s 2Q Mac sales of $7.168b, which seemed to trigger the recent press concerns, are only 1.14% lower than the average of all 2Q results since 2018, including those in the COVID years, and just looking at the pre-COVID years (2018 – 2020), 2023 2Q Mac sales are 28.7% higher than the average.

We expect SDC and LGD are most concerned about the cost of making the conversions to Gen 8 against other larger substrate transitions, rather than Apple’s near-term results, and if either company has been assuming that demand during COVID was ‘real’, we have misjudged both companies. Spending the billions necessary to build out a Gen 8 OLED infrastructure for IT was a risky business before COVID, during COVID, and will be after COVID, but those decisions tend not to be made on near-term issues, as they are bets that will play out over many years. SDC does have the cost issue to settle with Canon, especially as LGD has aligned with Sunic Systems, but we expect that has more to do with the timing of Samsung Display’s decision than the relative decline in Apple’s Mac sales over the last two quarters.

In order to improve efficiency and volume, there has been considerable speculation that such new facilities would be Gen 8 RGB OLED fabs, which currently do not exist (LG Display has Gen 8 OLED fabs but they use a non-RGB process that is not viable for Apple’s specifications), so considerable R&D has been, and still has to be done to design the equipment necessary to make the transition to Gen 8 OLED production for Apple’s (and others’) IT products.

Up until the beginning of this year, most predictions included Samsung Display starting construction on a Gen 8 RGB OLED fab this year, either converting an idle Gen 8 LCD fab or converting a Gen 6 line to Gen 8. LG Display, while a bit less specific, has been expected to do the same, and BOE, has hinted that they will follow a similar path ‘as the market demands’, but the ever-shifting sands of the CE space have begun to cast askance at those plans and concomitant timelines. The equipment needed to deposit OLED materials on the larger Gen 8 substrates takes considerable R&D to develop, and as we have noted previously, there are only a few companies with the expertise to develop such tools. Sunic Systems (171090.KS) is working with LG Display, and at one time Samsung Display was working with ULVAC (6728.JP) on such tool development, but has since abandon that project, and is looking at the industry leader Canon-Tokki (7751.JP) as a potential Gen 8 deposition tool supplier. However, Canon does not want to bear the cost of the tool’s development, as Gen 8 OLED adoption is still an unknown, and expects Samsung Display to pay for the development as a part of the tool price.

With the objective of reducing costs/m2, a boost to tool costs will eat away at the process BOM, and SDC has been hesitating to place the order with Canon, with a cut-off of the end of 2Q if it is to meet the goal of Gen 8 production for Apple in 2024. But it seems not only has the cost of building out Gen 8 OLED capacity been an issue, but the trade press has taken Apple’s recent Mac sales declines as an omen that is adding additional hesitation to the Gen 8 OLED build-out for all potential participants. We differ.

As with almost all CE products, the COVID-19 pandemic changed what was previously a relatively stable demand picture for Apple products. Mobile devices saw some early positive momentum, but the need to communicate online became the driver for tablet, laptop, and PC sales that set volume records. We look at the years between 2020 and 2022 as ‘aberrational’ in terms of demand and look to more normalized unit volumes as a better indicator of what we should expect going forward. In the case of Apple, particularly the Apple Mac, a tool that is known for its use among content developers who require high quality displays, the logic holds that Apple would like to make the transition to OLED for its color purity, high contrast, and color gamut, but recent headlines from overseas are decrying the fact that Apple’s Mac sales are declining and adding to OLED panel producers’ hesitation concerning spending for Gen 8 RGB OLED fabs.

However looking at Apple’s Mac sales going back to 2018, they average $6.35b per quarter, including the heady COVID years, which puts the last two quarters above the LTY average, despite the decline from 2022. More specifically, Apple’s 2Q Mac sales of $7.168b, which seemed to trigger the recent press concerns, are only 1.14% lower than the average of all 2Q results since 2018, including those in the COVID years, and just looking at the pre-COVID years (2018 – 2020), 2023 2Q Mac sales are 28.7% higher than the average.

We expect SDC and LGD are most concerned about the cost of making the conversions to Gen 8 against other larger substrate transitions, rather than Apple’s near-term results, and if either company has been assuming that demand during COVID was ‘real’, we have misjudged both companies. Spending the billions necessary to build out a Gen 8 OLED infrastructure for IT was a risky business before COVID, during COVID, and will be after COVID, but those decisions tend not to be made on near-term issues, as they are bets that will play out over many years. SDC does have the cost issue to settle with Canon, especially as LGD has aligned with Sunic Systems, but we expect that has more to do with the timing of Samsung Display’s decision than the relative decline in Apple’s Mac sales over the last two quarters.

Forest Illustration Credit: Luis Del Rio Comachero/Unsplash

Apple Mac Sales - 2018 - 2023 YTD - Source: SCMR LLC, Company Data

RSS Feed

RSS Feed