Fun with Data – New Semiconductor Fabs

According to Semi.org, using data from its 2,400 members, 19 new semiconductor fabs will begin construction this year with an additional 10 beginning construction next year. Of those 29 new fabs, 22 will be 300mm lines and 7 will range from 100mm to 200mm. The cost of these new fabs will be ~$140b and will add up to 2.6m 200mm wpm. China and Taiwan will see 8 new fabs each, while 6 will be built in the US, Europe with 3 and both Japan and South Korea having 2 each. Semi also notes that there are 8 additional lower probability fab projects that could be added.

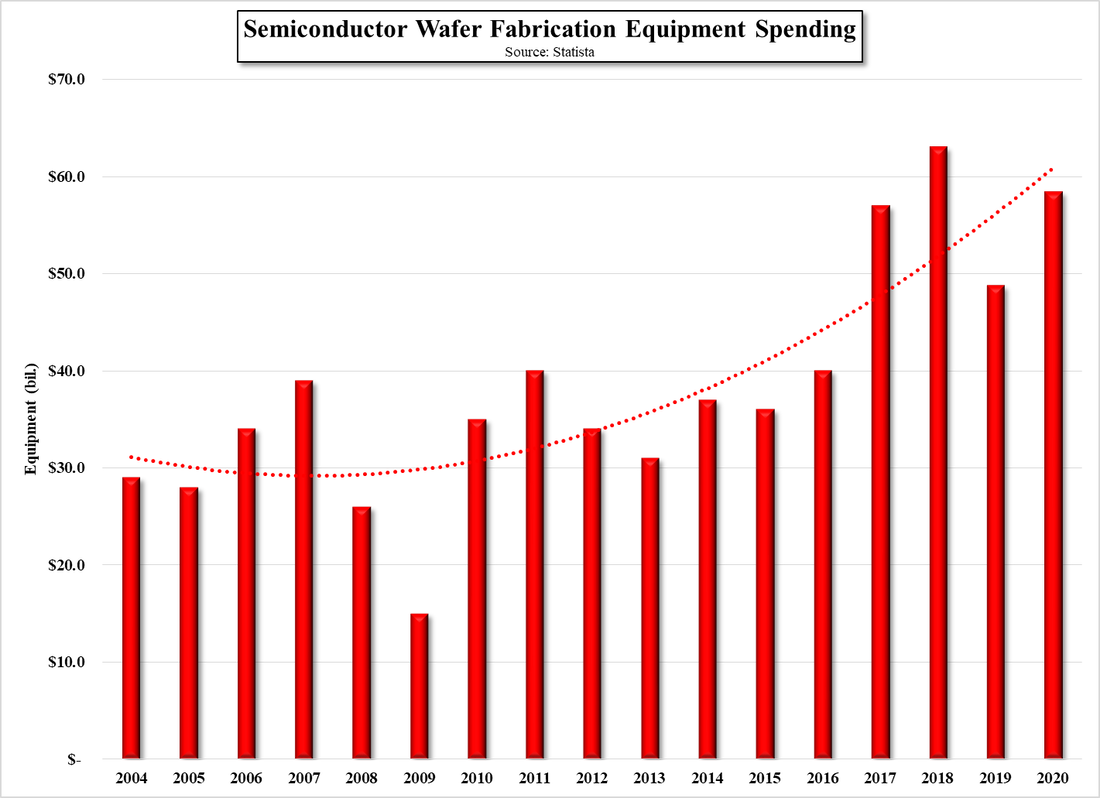

15 of the new fabs will be foundries with capacity ranging from 30,000 wpm to 200,000 wpm and 4 will be memory fabs with capacity ranging from 100,000 wpm to 400,000 (200mm equiv.) As the time frame for new fab construction is two years from groundbreaking to equipment install, even those beginning construction this year will likely not be producing until 2023, and we expect each project will have developed its own justification (automotive, telecom, etc) for the expansion. We show semiconductor fab equipment spending over the last 17 years in the chart below.

15 of the new fabs will be foundries with capacity ranging from 30,000 wpm to 200,000 wpm and 4 will be memory fabs with capacity ranging from 100,000 wpm to 400,000 (200mm equiv.) As the time frame for new fab construction is two years from groundbreaking to equipment install, even those beginning construction this year will likely not be producing until 2023, and we expect each project will have developed its own justification (automotive, telecom, etc) for the expansion. We show semiconductor fab equipment spending over the last 17 years in the chart below.

Semiconductor Wafer Fabrication Equipment Spending - Source: Statista

RSS Feed

RSS Feed