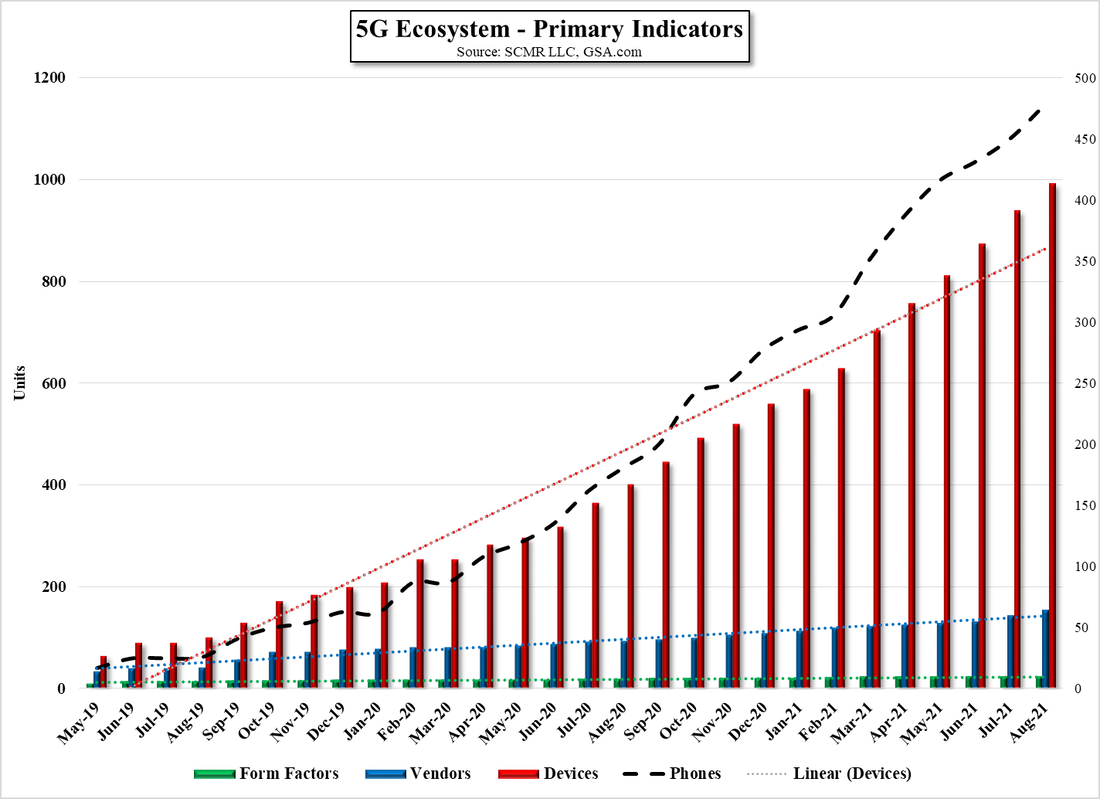

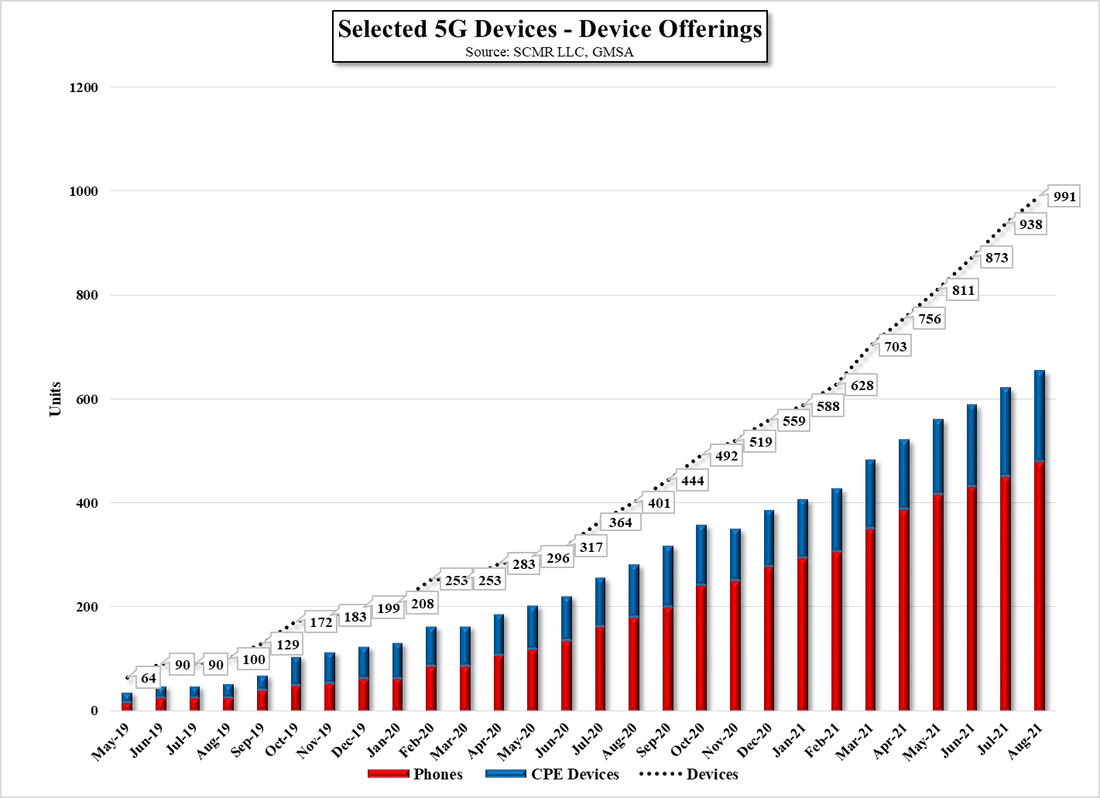

The FAA’s Other failure

In November of 2021 we noted that AT&T (T) and Verizon (VZ) had agreed to defer the launch of 5G services on C-Band spectrum (3.7 to 3.98 GHz), a portion of the 5G spectrum that they acquired during an earlier auction, until early January 2022. The postponement was at the request of the FAA who claims that the new service could interfere with altimeters used on aircraft. This comes in contrast to the FCC examination and approval of the band, finding no evidence to support the FAA’s claims, making sure that a wide spectrum guard band is left unused adjacent to the C-band spectrum. That guard band is twice the width requested by the airlines to make absolutely sure the altimeters are protected.

What made that a bit unusual is that the C-band spectrum was already being used in ~40 countries for 5G, with no reported altimeter problems, while at the time the FAA was quoted saying, “Tick, tick, tick” in a Tweet, alluding to the eventual disaster they expected to occur, which has riled many, especially as the FAA acknowledged that it had no proven evidence of interference from C-band operation and continued to use contacts in Congress to wage a battle against the FCC’s ‘no issue’ ruling. While the FAA continued to push for a block to 5G C-band deployment near airports, they released a bulletin in November ‘21 suggesting that “radio altimeter manufacturers, aircraft manufacturers, and operators voluntarily provide to federal authorities specific information related to altimeter design and functionality, specifics on deployment and usage of radio altimeters in aircraft, and that they test and assess their equipment in conjunction with federal authorities.” In other words, lets upgrade those altimeters, despite the fact that the same C-band issues had been under review for over 4 years.

It now seems that the FAA has issued a new directive that requires both cargo and passenger airplanes in the US to install 5G C-band tolerant radio altimeters or an approved RF filter by February 24, 2024, which will allow AT&T, Verizon, and other potential 5G carriers to bring 5G services to full power near airports, something which they have been unable to do under the 2021 stand-off agreement, but the new directive also contained the FAA’s estimate of what it would cost to modify planes under the new rules. That cost is ~$26m to outfit 180 airplanes that need new altimeters and 820 that will need RF filters, out of a total fleet of 7,993 planes, far less than the direct and indirect cost of resources used to promote the media battle that has lasted over a year and a half between the FAA and the FCC. Some have even suggested that AT&T and Verizon would have paid the $26m for the upgrades out-of-pocket if they had known of the cost, or it could have been included in the price of the spectrum bid at auction if it had been communicated by the FAA (the auction bid for the C-band was $81.2 billion).

Once again political infighting based on political agendas between government agencies cost the taxpayers money and resources, and slowed the progress of technology improvements, with the low level of communications between agencies that have a common focus generating headlines that both confuse consumers and create governmental distrust. While expanding 5G services might not be an essential key to economic growth in the US, it does have implications across a broad spathe of consumer devices and the deployment of 5G in the US will serve to enhance many existing services and produce income for a wide variety of companies, including the Treasury of the United States. If carriers are unsure that they will be able to deploy purchased spectrum, the value of that spectrum will decline, and given that the 1st C-band auction, which took place in 2020, generated $81b in gross bids, those dollars will pay for lots of projects that will benefit consumers.

Mandates (according to usa.gov)

FCC - The goal of the Commission is to promote connectivity and ensure a robust and competitive market.

FAA – The goal of the FAA is to provide the safest, most efficient aerospace system in the world.

What made that a bit unusual is that the C-band spectrum was already being used in ~40 countries for 5G, with no reported altimeter problems, while at the time the FAA was quoted saying, “Tick, tick, tick” in a Tweet, alluding to the eventual disaster they expected to occur, which has riled many, especially as the FAA acknowledged that it had no proven evidence of interference from C-band operation and continued to use contacts in Congress to wage a battle against the FCC’s ‘no issue’ ruling. While the FAA continued to push for a block to 5G C-band deployment near airports, they released a bulletin in November ‘21 suggesting that “radio altimeter manufacturers, aircraft manufacturers, and operators voluntarily provide to federal authorities specific information related to altimeter design and functionality, specifics on deployment and usage of radio altimeters in aircraft, and that they test and assess their equipment in conjunction with federal authorities.” In other words, lets upgrade those altimeters, despite the fact that the same C-band issues had been under review for over 4 years.

It now seems that the FAA has issued a new directive that requires both cargo and passenger airplanes in the US to install 5G C-band tolerant radio altimeters or an approved RF filter by February 24, 2024, which will allow AT&T, Verizon, and other potential 5G carriers to bring 5G services to full power near airports, something which they have been unable to do under the 2021 stand-off agreement, but the new directive also contained the FAA’s estimate of what it would cost to modify planes under the new rules. That cost is ~$26m to outfit 180 airplanes that need new altimeters and 820 that will need RF filters, out of a total fleet of 7,993 planes, far less than the direct and indirect cost of resources used to promote the media battle that has lasted over a year and a half between the FAA and the FCC. Some have even suggested that AT&T and Verizon would have paid the $26m for the upgrades out-of-pocket if they had known of the cost, or it could have been included in the price of the spectrum bid at auction if it had been communicated by the FAA (the auction bid for the C-band was $81.2 billion).

Once again political infighting based on political agendas between government agencies cost the taxpayers money and resources, and slowed the progress of technology improvements, with the low level of communications between agencies that have a common focus generating headlines that both confuse consumers and create governmental distrust. While expanding 5G services might not be an essential key to economic growth in the US, it does have implications across a broad spathe of consumer devices and the deployment of 5G in the US will serve to enhance many existing services and produce income for a wide variety of companies, including the Treasury of the United States. If carriers are unsure that they will be able to deploy purchased spectrum, the value of that spectrum will decline, and given that the 1st C-band auction, which took place in 2020, generated $81b in gross bids, those dollars will pay for lots of projects that will benefit consumers.

Mandates (according to usa.gov)

FCC - The goal of the Commission is to promote connectivity and ensure a robust and competitive market.

FAA – The goal of the FAA is to provide the safest, most efficient aerospace system in the world.

RSS Feed

RSS Feed