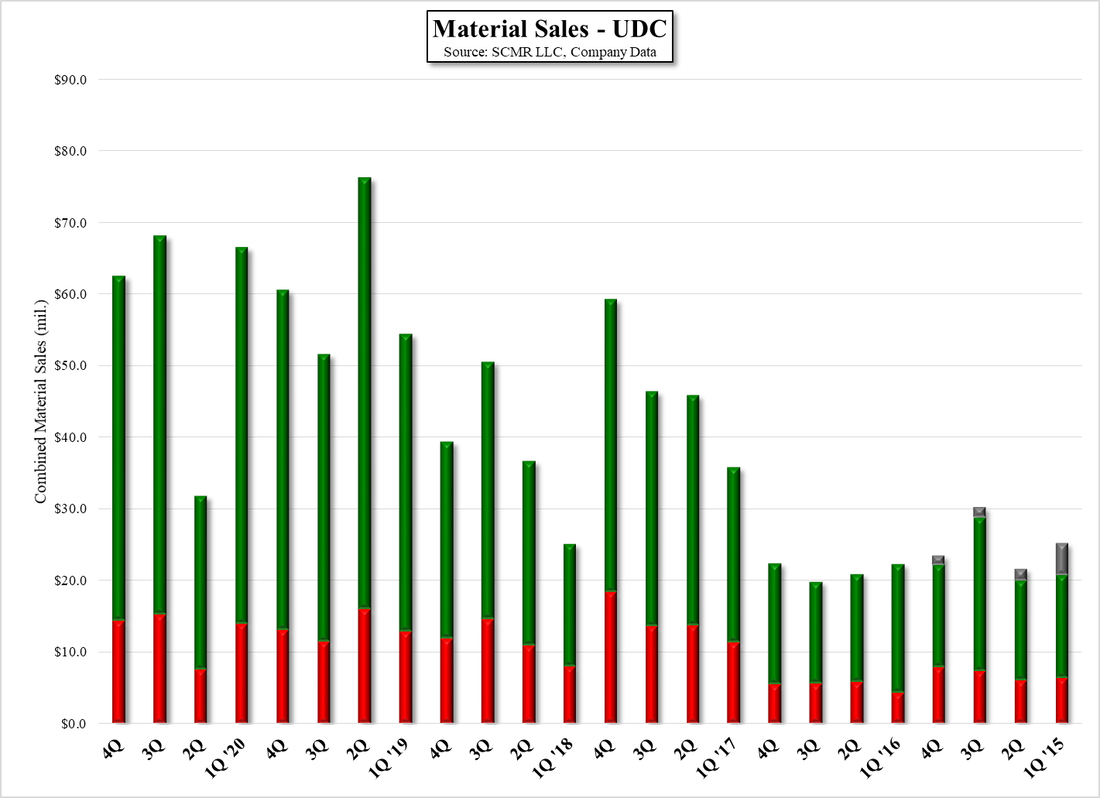

Off Again, On Again

We have mentioned a number of times that over the last few quarters Samsung Electronics (005930.KS) and LG Display (LPL) have been negotiating over a panel supply deal for OLED displays. Samsung, whose display affiliate Samsung Display (pvt) has exited the LCD TV panel business, has been looking to expand its premium TV offerings, and while it offers its own Quantum Dot/OLED TVs, production is limited to one 30K fab, leaving Micro-LED TVs at the top of the line, albeit far out of reach for almost all consumers, the company’s Mini-LED/Quantum Dot lines, a small QD/OLED line, and Samsung’s Quantum Dot only LCD TVs. With the premium Tv market the only TV segment expected to show positive y/y growth this year, building out that segment is quite important currently and likely necessary for the next few years.

Samsung Premium TV 2023 Line-Up

While the definition of ‘premium’ in the Tv market varies, we define the ‘premium’ TV market as sets that are 55” or larger and cost $1,000 or more, and the lines shown in the graphic above all fall into that category, with a few models just below the ‘premium’ cut as shown in the table below. As the Micro-LED line is not really a consumer-friendly priced item. We would expect Samsung, if a deal were concluded, to insert the ‘New OLED’ line at the same price points as the QD/OLED line to increase the volume of OLED offerings at those price points, and consequently, those price points are roughly equal to LG’s (066570.KS) own G3 OLED TV line, so price competition between the two rivals would not create further friction.

The big question however is Samsung’s margins on the new OLED line, much of which would be determined by the agreed-on price for the panels, which was said to be the contention throughout the earlier negotiations. As Samsung is expected to purchase ~2m units next year, increasing to 3m and 5m in the following years (unconfirmed), and perhaps up to 1m panels this year, they are looking for a substantial discount to LGD’s normal transfer price. LG Display has been running its WOLED fabs at less than full utilization so far this year, and such a deal would give a needed boost to OLED utilization rates that have dragged down profitability in recent quarters. However rumors that Samsung is demanding prices below those offered to LG Display’s parent, which would likely cause a bit of bad blood between parent and affiliate. That said, LG owns almost 60% of LG Display, so it’s an odd situation for LG.

While news services have picked up the supposed ‘movement’ in the negotiations, this would not be the first time a ‘deal done’ signal was given (or assumed) from local South Korean media. While such a deal will have benefits for both parties, there is considerable emotional skin in the game for Samsung, who decided in 2013 that producing large RGB OLED panels was not a viable process. In fact, they were correct in that assumption, as LG Display does not use and RGB patterning process in its OLED panels, but one encompassing creating a white light with a combination of OLED emitters and using a color filter to create the necessary red, green and blue sub-pixels., which reduces the brightness of the display. Over the years LGD has adopted a number of improvements that have offset some of that issue, but the current-day management at Samsung must bow to the fact that the 2013 decision has given LGD a distinct advantage in the OLED TV space, as both the sole OLED TV panel supplier and LG’s over 50% share of the OLED TV set market.

It will be challenging for Samsung to come up with a marketing plan that continues to sell its QD/OLED technology while extoling the virtues of LG Display’s OLED TV panel vision, and not degrading the company’s Mini-LED/QD technology, which Samsung has been championing since 2021. Of course that is what the marketing guys get paid for, so we expect rounds of advertisements providing little empirical information about the pluses and minuses of each technology, and more on why whatever the technology is, Samsung’s is better than others. Samsung’s smartphone and TV divisions were ‘ordered’ to find solutions to improve earnings after 1Q results led to an 18% decline in sales and the lowest operating profit the company has seen in many years. Tv division sales were down 14.8% y/y, so there is considerable pressure to expand the premium set business and bring up margins from upper management, so likely less face saving, and more sales will be the holiday mantra this year.

The big question however is Samsung’s margins on the new OLED line, much of which would be determined by the agreed-on price for the panels, which was said to be the contention throughout the earlier negotiations. As Samsung is expected to purchase ~2m units next year, increasing to 3m and 5m in the following years (unconfirmed), and perhaps up to 1m panels this year, they are looking for a substantial discount to LGD’s normal transfer price. LG Display has been running its WOLED fabs at less than full utilization so far this year, and such a deal would give a needed boost to OLED utilization rates that have dragged down profitability in recent quarters. However rumors that Samsung is demanding prices below those offered to LG Display’s parent, which would likely cause a bit of bad blood between parent and affiliate. That said, LG owns almost 60% of LG Display, so it’s an odd situation for LG.

While news services have picked up the supposed ‘movement’ in the negotiations, this would not be the first time a ‘deal done’ signal was given (or assumed) from local South Korean media. While such a deal will have benefits for both parties, there is considerable emotional skin in the game for Samsung, who decided in 2013 that producing large RGB OLED panels was not a viable process. In fact, they were correct in that assumption, as LG Display does not use and RGB patterning process in its OLED panels, but one encompassing creating a white light with a combination of OLED emitters and using a color filter to create the necessary red, green and blue sub-pixels., which reduces the brightness of the display. Over the years LGD has adopted a number of improvements that have offset some of that issue, but the current-day management at Samsung must bow to the fact that the 2013 decision has given LGD a distinct advantage in the OLED TV space, as both the sole OLED TV panel supplier and LG’s over 50% share of the OLED TV set market.

It will be challenging for Samsung to come up with a marketing plan that continues to sell its QD/OLED technology while extoling the virtues of LG Display’s OLED TV panel vision, and not degrading the company’s Mini-LED/QD technology, which Samsung has been championing since 2021. Of course that is what the marketing guys get paid for, so we expect rounds of advertisements providing little empirical information about the pluses and minuses of each technology, and more on why whatever the technology is, Samsung’s is better than others. Samsung’s smartphone and TV divisions were ‘ordered’ to find solutions to improve earnings after 1Q results led to an 18% decline in sales and the lowest operating profit the company has seen in many years. Tv division sales were down 14.8% y/y, so there is considerable pressure to expand the premium set business and bring up margins from upper management, so likely less face saving, and more sales will be the holiday mantra this year.

RSS Feed

RSS Feed