More Fun With Data – Smartphone Cameras

Cameras are a mainstay feature for smartphones and we have followed the trend toward multiple cameras on such devices for years, with the first adding a second main camera in 2014. Little changed for a few years, but in 2018 a 3rd main camera was added to a number brands and by October, Samsung had one-upped the industry by adding a 4th main camera. In 2019 12.8% of all smartphone models had 4 or more main cameras which increased to 39.2% the following year, while last year that share dropped to 24.7% as smartphone pricing became a more serious factor, making 4 main cameras a bit more superfluous.

We believe much of the smartphone industry’s push to add multiple cameras on smartphones was generated by the industry itself and less so by consumers, so the lesser share of 4 or more main cameras last year strikes us a good thing, but at the same time the resolution of smartphone cameras has also improved, a more important metric than the number of cameras on a device. It is estimated that in 2021 more than 50% of main cameras fell within the 13Mp to 48Mp range, while ~20% were 49Mp to 64%, and those numbers are limited a bit by the iPhone, whose main cameras have relatively small pixel counts (12Mp) that are enhanced by software and TOF. Last year there were 32 models, representing 5.6% of all smartphone models that had main cameras with over 100Mp, up from 10 in 2020, so we see the trend moving to quality rather than quantity.

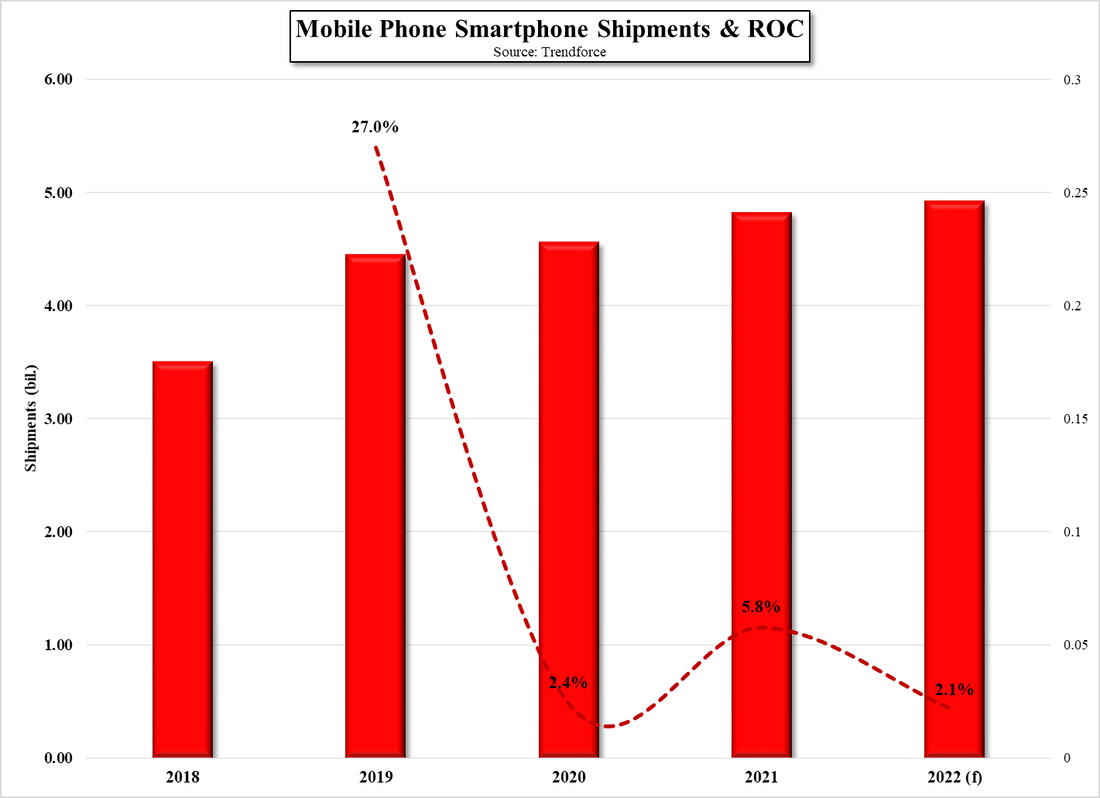

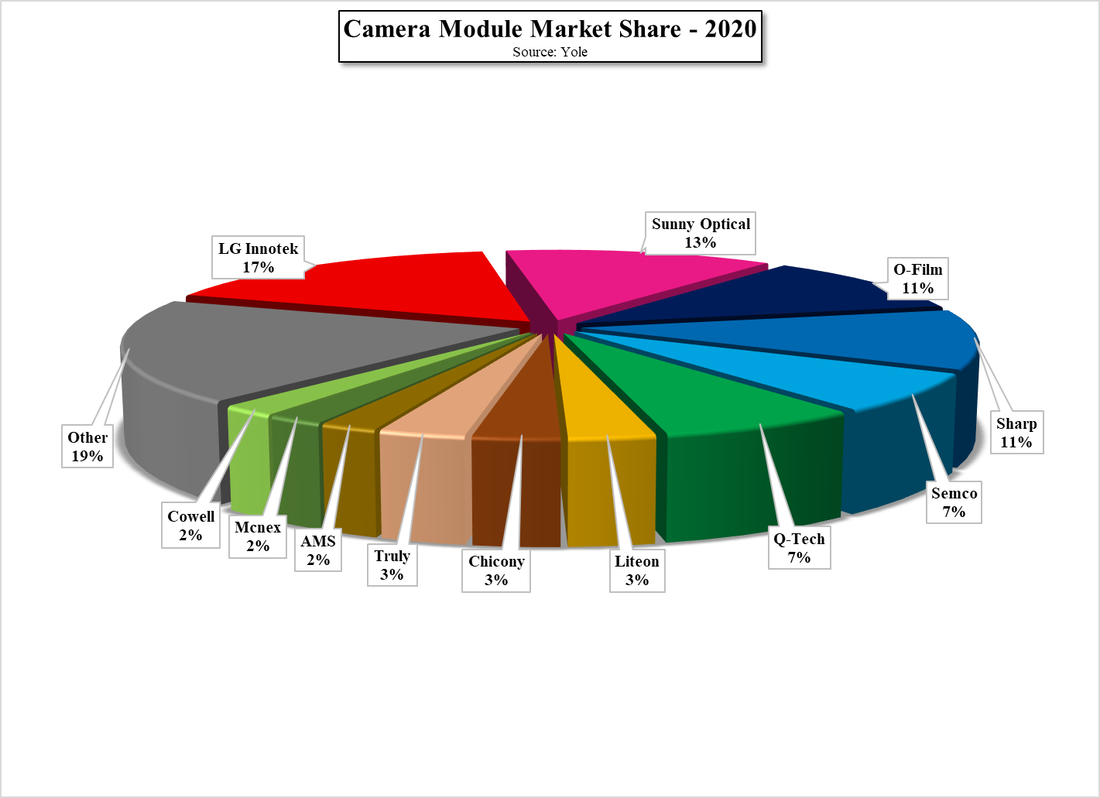

That’s the good news, but we are concerned about the growth rate of the mobile camera market in light of the change in focus, and while camera module shipments increased by 5.8% last year, expectations are closer to 2% to 2.5%, which seems a bit low but at least is reflective of what we expect will be the continued focus on mid-tier and low-end phones where camera counts are a more sensitive issue and higher quality cameras on flagship and foldables. Some of this has already been revealed in relatively weak forecasts for some Chinese camera component manufacturers, but the sales of the camera modules last year grew by 8.2% and is expected to see a CAGR (2020 – 2026) of 14.8% through 2026, with the slowest growing sub-segment, image sensors, still growing at a CAGR of 6.7% over the period. Leaders in the module space (2020) are LG Innotek (011070.KS), Sunny Optical (2382.HK), O-Film (002456.CH), Sharp (6753.JP), and Semco (009150.KS), as indicated in Fig. 3.

We believe much of the smartphone industry’s push to add multiple cameras on smartphones was generated by the industry itself and less so by consumers, so the lesser share of 4 or more main cameras last year strikes us a good thing, but at the same time the resolution of smartphone cameras has also improved, a more important metric than the number of cameras on a device. It is estimated that in 2021 more than 50% of main cameras fell within the 13Mp to 48Mp range, while ~20% were 49Mp to 64%, and those numbers are limited a bit by the iPhone, whose main cameras have relatively small pixel counts (12Mp) that are enhanced by software and TOF. Last year there were 32 models, representing 5.6% of all smartphone models that had main cameras with over 100Mp, up from 10 in 2020, so we see the trend moving to quality rather than quantity.

That’s the good news, but we are concerned about the growth rate of the mobile camera market in light of the change in focus, and while camera module shipments increased by 5.8% last year, expectations are closer to 2% to 2.5%, which seems a bit low but at least is reflective of what we expect will be the continued focus on mid-tier and low-end phones where camera counts are a more sensitive issue and higher quality cameras on flagship and foldables. Some of this has already been revealed in relatively weak forecasts for some Chinese camera component manufacturers, but the sales of the camera modules last year grew by 8.2% and is expected to see a CAGR (2020 – 2026) of 14.8% through 2026, with the slowest growing sub-segment, image sensors, still growing at a CAGR of 6.7% over the period. Leaders in the module space (2020) are LG Innotek (011070.KS), Sunny Optical (2382.HK), O-Film (002456.CH), Sharp (6753.JP), and Semco (009150.KS), as indicated in Fig. 3.

Mobile Phone Smartphone Shipments & ROC - Source: Trendforce

Camera Module Market Share - 2020 - Source: Yole

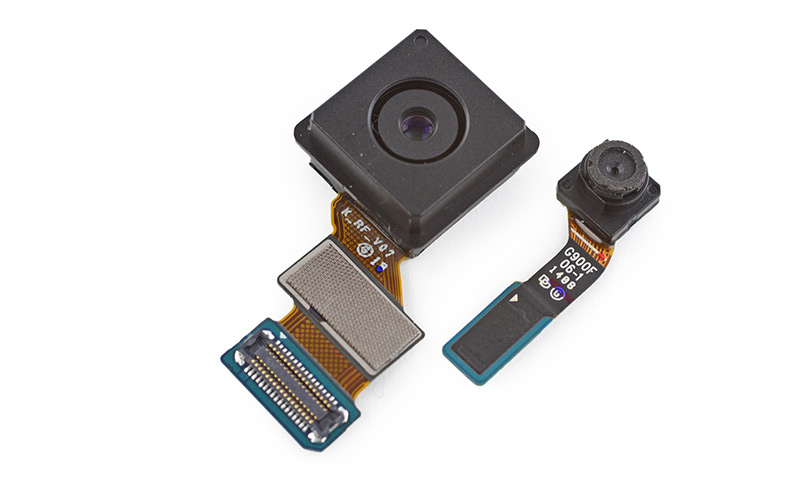

Camera Module from Samsung Galaxy S5 – Source: Samsung

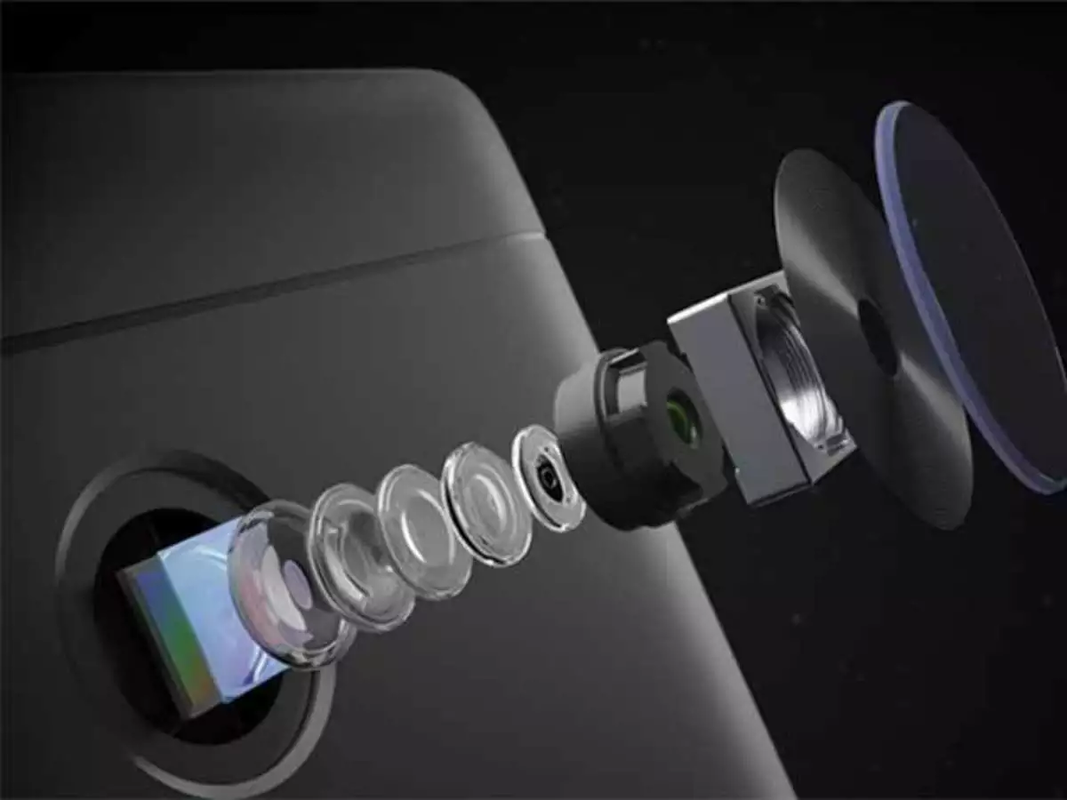

Physical Blow-uo of camera module components – Source: India Times

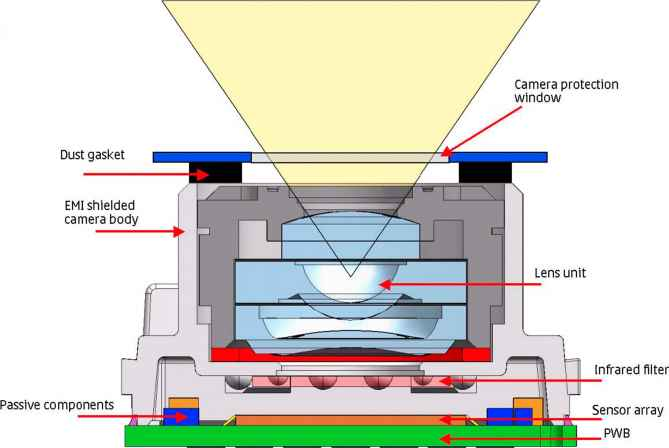

Camera Module Schematic - Cell Phone Repair Chicago

RSS Feed

RSS Feed