Universal Display – Big Beat – Eyes Open

Universal Display (OLED) reported 4Q and full year results that were considerably above consensus. 4Q sales were $141.54m, up 20.9% q/q and up 37.8% y/y, against a consensus estimate of $109.3m, net income was $53.9m up 33.1% q/q and up 104% y/y, while EPS was $1.14, up 33.0% q/q and up 102.8% y/y, against a consensus estimate of $0.64. Material sales, which drive the company’s business, were $62.54m, down 9.0% q/q but up 2.9% y/y, while license & royalty sales were $75.05m, up 68.5% q/q and up 98.5% y/y. Guidance for 2021 (full-year) was for sales between $530m and $560m or a mid-point of $545m, which is right on the consensus estimates for 2021.

Before we go further, we believe it is worth deconstructing the UDC numbers a bit to get a better idea of how the company worked through 4Q and what was an unusual year. Since accounting rule ASC 606 was put into effect in 2018, rather than book license and royalty revenue when it is received, companies must recognize license and royalty on a pro rata basis, based on material sales and estimates of the total value of the contract over its life. While this rule goes toward smoothing out license and royalty revenue that varied significantly on a quarterly basis under previous rules, it also requires companies to estimate the total contract value regularly and how price changes and sell-through progress agree with previous ASC 606 estimates. If there are material changes to contract estimate variables, the ratio between material sales and license and royalty revenue gets ‘trued up’, which was the case with UDC this quarter. Approximately $17m of additional revenue was recognized in 4Q as part of the ‘true-up’, which the company stated was based on how COVID-19 affected their business over the 2020 year.

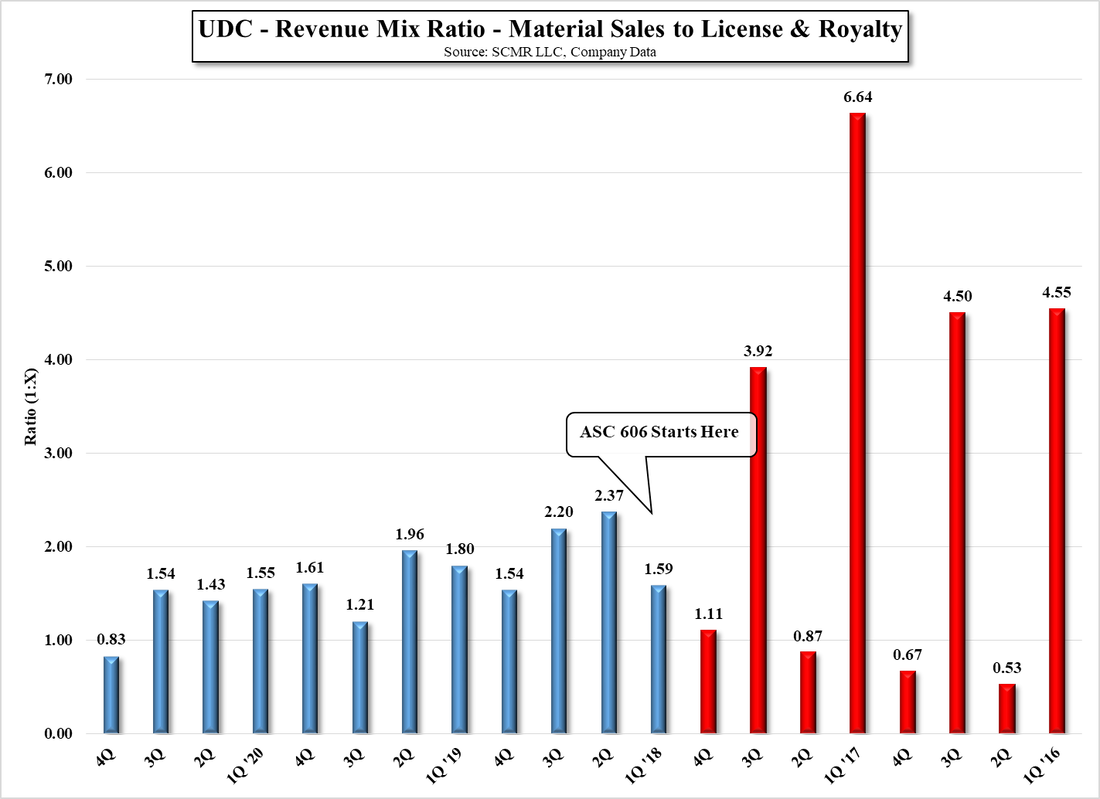

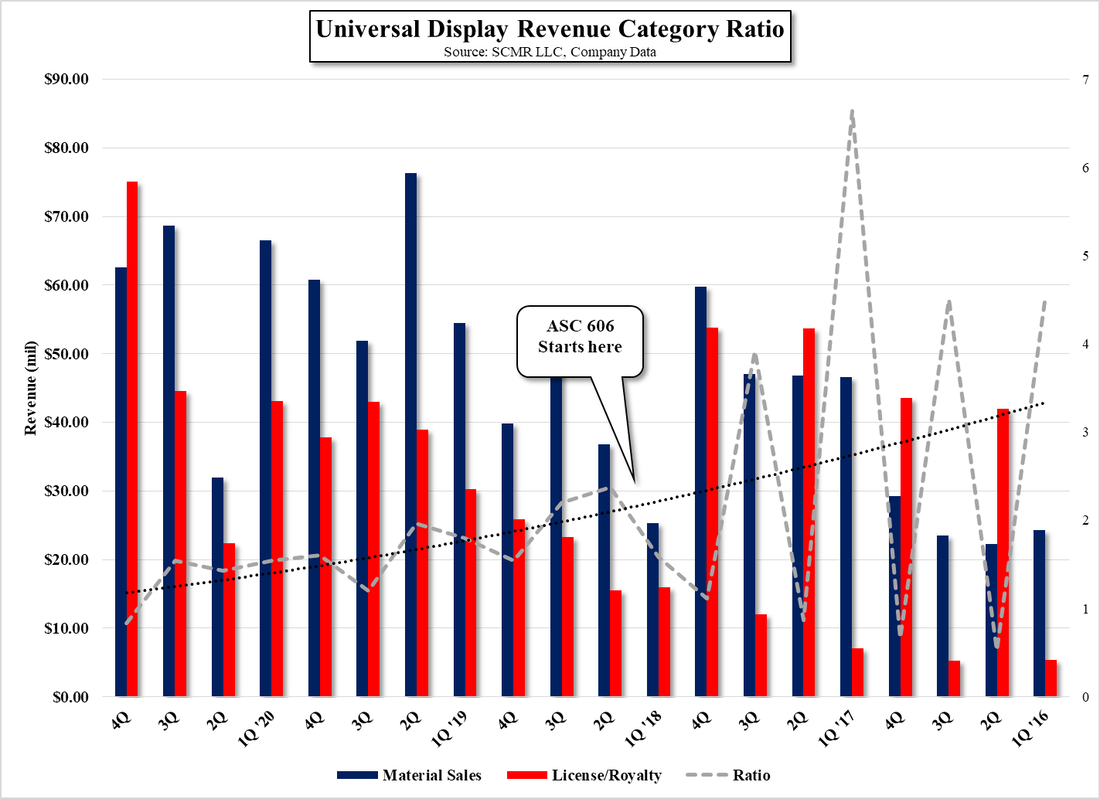

A more visual way to see the result of this true-up is to look at the ratio between material sales and license and royalty income (Fig. 1). Before ASC 606, License & Royalty revenue was sporadic, primarily a result of Samsung Display’s (pvt) bi-annual payments, different from all other L&R agreements. Since ASC 606 (blue), the ratio has become far less volatile, averaging 1.925, 1.645, and 1.357 in 2018, 2019, and 2020, with the previous four quarters averaging 1.53. The 4Q true-up caused the rationto drop to .83, meaning the 4Q examination indicated that the L&R revenue, as measured against expected material sales over the life of the contract, was too low, and hence the $17m of additional L&R revenue booked in the quarter. If there were no true-up and the 1.53 ratio was held into 4Q, the 4Q sales would have been ~107m, slightly below consensus. That said, UDC guided to a return to a 1:1.5 ratio for this year, barring any unusual circumstances that would cause another true-up. Fig. 2 shows the actual revenue segments, along with the ratio trend line and the ratio itself (gray).

Before we go further, we believe it is worth deconstructing the UDC numbers a bit to get a better idea of how the company worked through 4Q and what was an unusual year. Since accounting rule ASC 606 was put into effect in 2018, rather than book license and royalty revenue when it is received, companies must recognize license and royalty on a pro rata basis, based on material sales and estimates of the total value of the contract over its life. While this rule goes toward smoothing out license and royalty revenue that varied significantly on a quarterly basis under previous rules, it also requires companies to estimate the total contract value regularly and how price changes and sell-through progress agree with previous ASC 606 estimates. If there are material changes to contract estimate variables, the ratio between material sales and license and royalty revenue gets ‘trued up’, which was the case with UDC this quarter. Approximately $17m of additional revenue was recognized in 4Q as part of the ‘true-up’, which the company stated was based on how COVID-19 affected their business over the 2020 year.

A more visual way to see the result of this true-up is to look at the ratio between material sales and license and royalty income (Fig. 1). Before ASC 606, License & Royalty revenue was sporadic, primarily a result of Samsung Display’s (pvt) bi-annual payments, different from all other L&R agreements. Since ASC 606 (blue), the ratio has become far less volatile, averaging 1.925, 1.645, and 1.357 in 2018, 2019, and 2020, with the previous four quarters averaging 1.53. The 4Q true-up caused the rationto drop to .83, meaning the 4Q examination indicated that the L&R revenue, as measured against expected material sales over the life of the contract, was too low, and hence the $17m of additional L&R revenue booked in the quarter. If there were no true-up and the 1.53 ratio was held into 4Q, the 4Q sales would have been ~107m, slightly below consensus. That said, UDC guided to a return to a 1:1.5 ratio for this year, barring any unusual circumstances that would cause another true-up. Fig. 2 shows the actual revenue segments, along with the ratio trend line and the ratio itself (gray).

UDC - Revenue Mix Ratio - Material Sales to License & Royalty - Source: SCMR LLC, Company Data

Universal Display Revenue Category Ratio - Source: SCMR LLC, Company Data

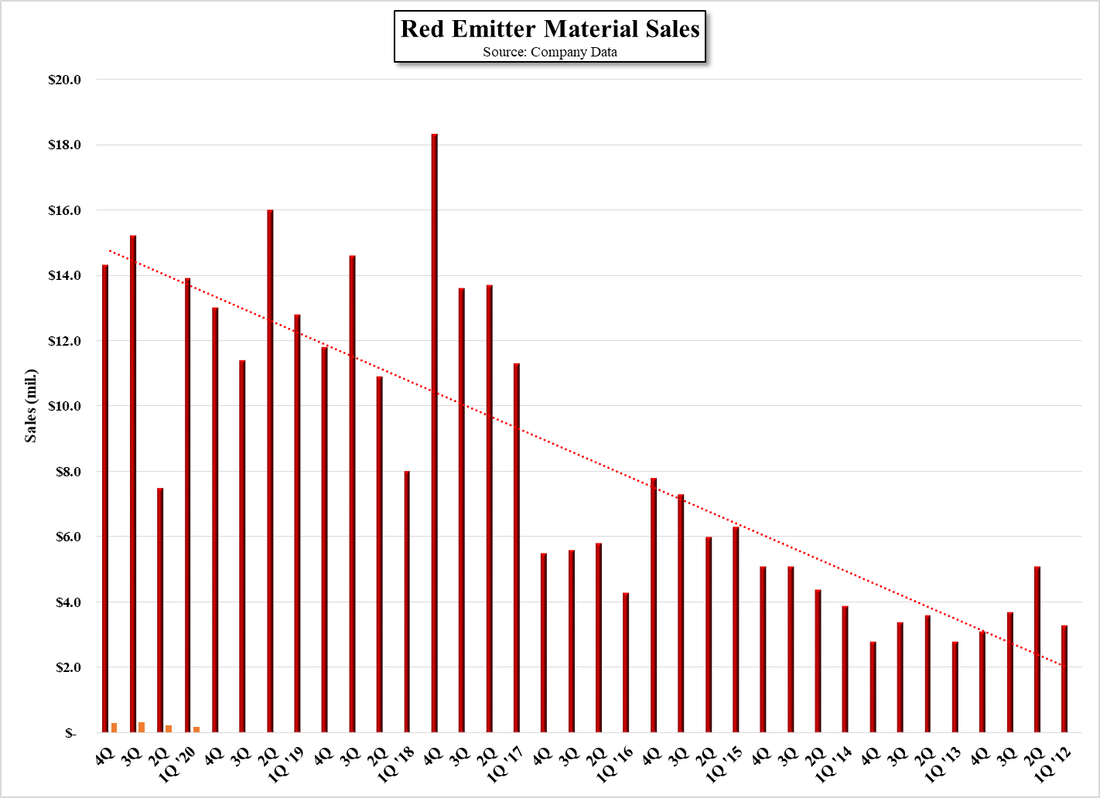

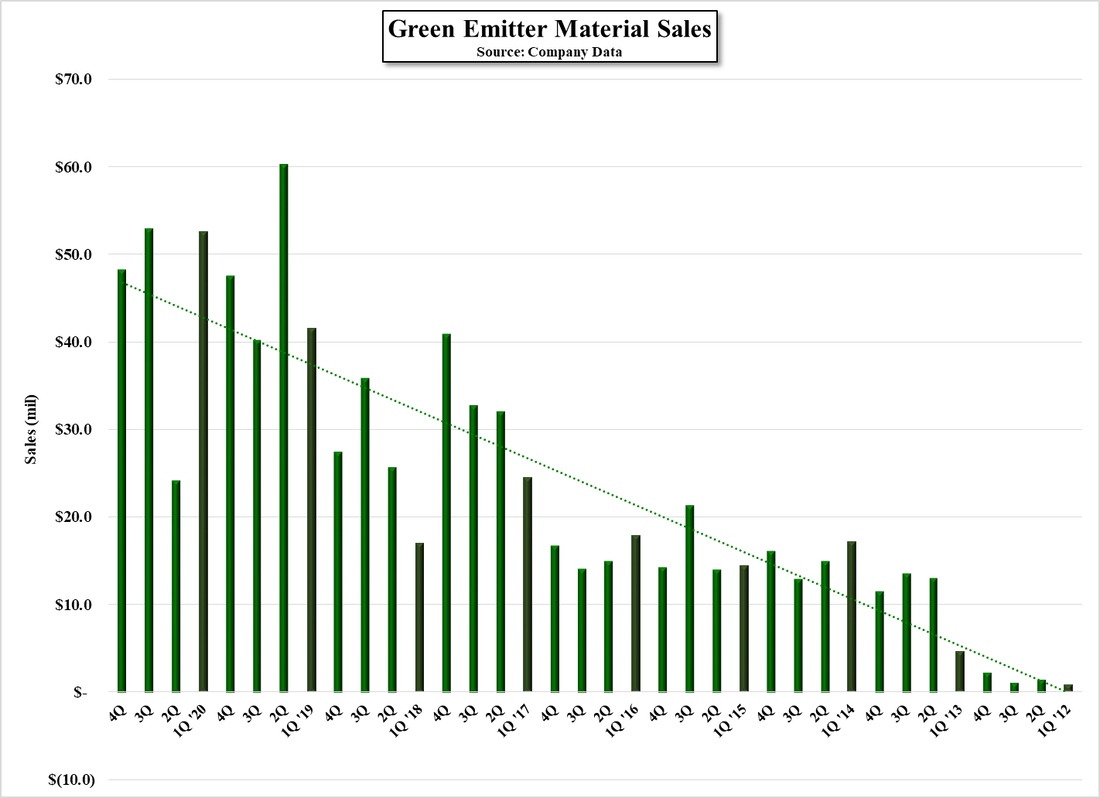

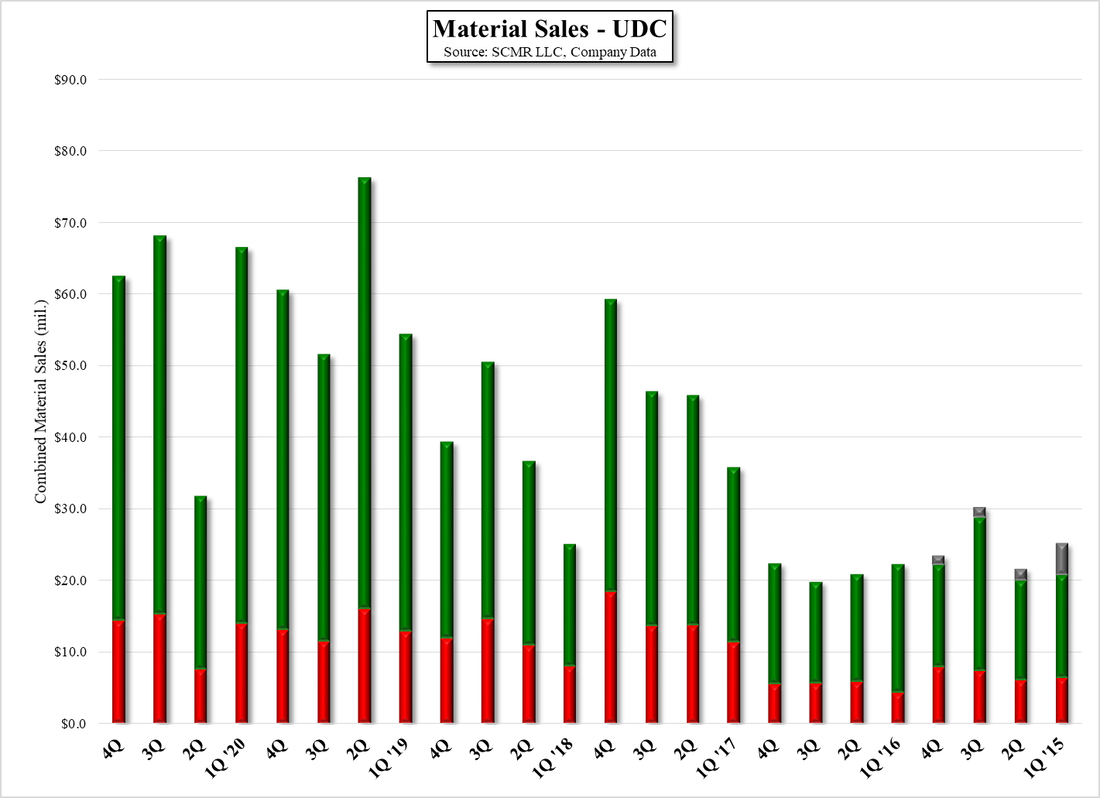

Material sales, however give far more insight into how UDC is performing, after taking into consideration the variability of customer ordering patterns, the red and green emitter trend lines seen in Figs. 3 & 4 are indicative of the expansion of the OLED display space, and 4Q results are close to both trend lines. Based on the sales guidance mentioned above and the return to the 1.5 material/L&R mix, the implication would be for material sales to grow ~38% and L&R sales to grow by 14.6%. Again this is based on ASC 606 and a 1.5 ratio, but in terms of actual L&R payments, rather than recognized L&R, we would expect L&R to grow more quickly, due to the expansion of LG Display’s (LPL) OLED TV production schedule, which is expected to rise from ~4.5m in 2020 to between 7m and 8m this year. As LG Display pays a unit price based royalty (Samsung pays a flat fee), the dollar value of the increasing number of OLED TV sets sales will rise quickly relative to material usage, as we expect LGD to continue to drive up its material usage efficiency, and with the increasing volumes, see a lower per kilogram material cost.

Red Emitter Material Sales - Source: SCMR LLC, Company Data

Green Emitter Material Sales - Source: SCMR LLC, Company Data

UDC - Combined Material Sales - Source: SCMR LLC, Company Data

One point that should be noted is that while the differential between 1H and 2H material sales is normally a function of the 2H holiday season (2H share average is 57.7% over 5 years), the split in 2020 was affected by the COVID-19 outbreak, which caused 2Q, normally a sequentially better quarter than 1Q, to be one where companies were so unsure as to how the pandemic would affect consumers, that they were unusually cautious about production and material purchases. While final TV set sales data is not complete, we expect the 1H/2H ratio to be above the norm, possibly a record for 2H share, so we note that while dealing with the pandemic has become the norm for many people and companies, UDC is expecting 2H to be better than 1H, although no ratio was given.

While this seems quite logical, we caution investors that if the pandemic subsides, either due to a more careful society (not likely) or increasing immunity from vaccines, there is the possibility that a return to a more ‘external’ lifestyle could reduce the demand for TV set purchases. This caveat is less of an influence for TVs however, as while North America saw overall strength in TV sales last year, less was seen in other regions, leading to the possibility that while North American TV set sales last year could have included pull-ins of this year’s TV set sales and could see slow growth under a ‘COVID-19 recovery’ scenario, China could offset that with stronger growth. In either case, we expect UDC material sales, especially those to OLED TV manufacturers, will be greater in 2H again, but there are some scenarios where the 2nd half could see more moderate growth.

UDC’s regional and key customer breakdown also gives some insight into 4Q and full year results. The regional breakdown shows that in 4Q sales to the company’s Korean customers increased markedly, with both Samsung Display and LG Display seeing increased sales. We note that the $17m true-up mentioned above is embedded in the overall sales number and likely weighted toward at least one if not both South Korean customers, so 4Q in Fig. 7 might be a bit exaggerated and less reflective of absolute material sales to those customers. China sales on an overall basis were down a bit in 4Q, but the drop in sales to BOE (200725.CH) (down 63% q/q and 67.8% y/y), while not totally out of the ordinary, was a bit disconcerting, although the $6.4m q/q drop in sales to BOE was offset by an increase in sales to other Chinese customers of ~$3m, the net effect, a $3.5m drop in overall China sales in 4Q. While it is always concerning to see negative q/q growth in a top customer, variations in ordering patterns, especially from Chinese customers are commonplace and would only become a real concern if they extend for two or more quarters. That said, as a supplier to Huawei (pvt), we expect it could take BOE a bit to fill the lack of Huawei volume with long-term customers.

While this seems quite logical, we caution investors that if the pandemic subsides, either due to a more careful society (not likely) or increasing immunity from vaccines, there is the possibility that a return to a more ‘external’ lifestyle could reduce the demand for TV set purchases. This caveat is less of an influence for TVs however, as while North America saw overall strength in TV sales last year, less was seen in other regions, leading to the possibility that while North American TV set sales last year could have included pull-ins of this year’s TV set sales and could see slow growth under a ‘COVID-19 recovery’ scenario, China could offset that with stronger growth. In either case, we expect UDC material sales, especially those to OLED TV manufacturers, will be greater in 2H again, but there are some scenarios where the 2nd half could see more moderate growth.

UDC’s regional and key customer breakdown also gives some insight into 4Q and full year results. The regional breakdown shows that in 4Q sales to the company’s Korean customers increased markedly, with both Samsung Display and LG Display seeing increased sales. We note that the $17m true-up mentioned above is embedded in the overall sales number and likely weighted toward at least one if not both South Korean customers, so 4Q in Fig. 7 might be a bit exaggerated and less reflective of absolute material sales to those customers. China sales on an overall basis were down a bit in 4Q, but the drop in sales to BOE (200725.CH) (down 63% q/q and 67.8% y/y), while not totally out of the ordinary, was a bit disconcerting, although the $6.4m q/q drop in sales to BOE was offset by an increase in sales to other Chinese customers of ~$3m, the net effect, a $3.5m drop in overall China sales in 4Q. While it is always concerning to see negative q/q growth in a top customer, variations in ordering patterns, especially from Chinese customers are commonplace and would only become a real concern if they extend for two or more quarters. That said, as a supplier to Huawei (pvt), we expect it could take BOE a bit to fill the lack of Huawei volume with long-term customers.

Universal Display - Regional Sales - Source: SCMR LLC, COmpany Data

UDC - Top 3 Customers - Sales - Source: SCMR LLC, Company Data

Universal Display - China Sales - Source: SCMR LLC, Company Data

There were two other points of significance mentioned during the 4Q call, both worth mentioning. First, UDC expects to see spending toward the development of the company’s OVJP (Organic Vapor Jet Printing) system increase this year as the spin-off created last July works toward developing an ‘alpha’ version of the tool by 2022. While we are less concerned about the spending associated with the development of this project, we share some of the concerns expressed on the call about whether the timeline for a commercialized OVJP tool could allow for alternative display process technologies (such as micro-LED) to gain a foothold in the industry and lessen the need for the OVJP tool. We understand that such a tool will take time to develop, but we also note that technological development in the display space are moving quickly and while we expect micro-LED onr a commercialized mass production level will not be available before 2023, the resources behind this self-emissive technology are large and well financed.

The other point that is of concern are margins, specifically material margins. UDC has indicated that it expects material margins to be in the range of 65% to 70% for the 2021 year. This is lower than the previous year’s expectations of 70% to 75% for material margins, and while overall company GM’s will still be ~80%, we believe the cost of some of the materials used in the formulation of UDC’s products have been rising. The price of Iridium, the metal that binds UDC’s organics together, has gone from $1,670/troy oz. on December 1, 2020 to $4,400 currently, and while the amounts are small that PPG (PPG), UDC’s material supplier would use, that is a very large increase.

UDC also stated that as their customer base continues to grow, customers demand customized materials that have to be developed by UDC in relatively small quantities until qualified and accepted by the customer. These ‘developmental’ materials are expensive to produce and as the expanding customer base requires more such projects, lower material margins are a result. While this is an acceptable explanation for lower material margins, along with higher raw material costs, even with UDC’s IP lock on phosphorescent OLED emitters OLED panel producers are pressing all of their suppliers for lower prices, and we expect UDC is no exception. UDC’s customers know there are many OLED material development projects underway, with some trying to develop alternative materials that do not have license or royalty fees attached, so we suspect there is also some material pricing pressure across the industry that could also lower UDC’s material margins in 2021. We also note that based on what we know of UDC’s pricing scale, as their customers grow their OLED material capacity and consequently their OLED material consumption, it takes less time for customers to reach price reduction goals, and while the volume is certainly the most important part of that equation, it also means less time at the higher price points.

While we always have our concerns about some of the blind sighted optimism the display industry and some investors have toward OLED (the segment and the company), our concerns are, at least currently, overridden by the overall growth in the OLED space, which is fueled by greater penetration in existing display markets and expanding capacity, both of which tend to override the nuances we mention each quarter. All in it was a good quarter for UDC and we expect the overall picture for OLED to continue to improve throughout the year, but we also note that technologies are shuffled around mare aggressively each year and every investor should keep their eyes wide open.

The other point that is of concern are margins, specifically material margins. UDC has indicated that it expects material margins to be in the range of 65% to 70% for the 2021 year. This is lower than the previous year’s expectations of 70% to 75% for material margins, and while overall company GM’s will still be ~80%, we believe the cost of some of the materials used in the formulation of UDC’s products have been rising. The price of Iridium, the metal that binds UDC’s organics together, has gone from $1,670/troy oz. on December 1, 2020 to $4,400 currently, and while the amounts are small that PPG (PPG), UDC’s material supplier would use, that is a very large increase.

UDC also stated that as their customer base continues to grow, customers demand customized materials that have to be developed by UDC in relatively small quantities until qualified and accepted by the customer. These ‘developmental’ materials are expensive to produce and as the expanding customer base requires more such projects, lower material margins are a result. While this is an acceptable explanation for lower material margins, along with higher raw material costs, even with UDC’s IP lock on phosphorescent OLED emitters OLED panel producers are pressing all of their suppliers for lower prices, and we expect UDC is no exception. UDC’s customers know there are many OLED material development projects underway, with some trying to develop alternative materials that do not have license or royalty fees attached, so we suspect there is also some material pricing pressure across the industry that could also lower UDC’s material margins in 2021. We also note that based on what we know of UDC’s pricing scale, as their customers grow their OLED material capacity and consequently their OLED material consumption, it takes less time for customers to reach price reduction goals, and while the volume is certainly the most important part of that equation, it also means less time at the higher price points.

While we always have our concerns about some of the blind sighted optimism the display industry and some investors have toward OLED (the segment and the company), our concerns are, at least currently, overridden by the overall growth in the OLED space, which is fueled by greater penetration in existing display markets and expanding capacity, both of which tend to override the nuances we mention each quarter. All in it was a good quarter for UDC and we expect the overall picture for OLED to continue to improve throughout the year, but we also note that technologies are shuffled around mare aggressively each year and every investor should keep their eyes wide open.

RSS Feed

RSS Feed