Sharp gets OLED help from former rival

The new management of Sharp (6753.JP) has figured out that they have vast resources at their disposal, and perhaps the disparate entities owned by Hon Hai (2317.TT)/Foxconn (2354.TT) can now work together to build a better display (and crush rival Samsung Display). We believe that Innolux (3481.TT) a subsidiary of Foxconn and former rival, who now controls Sharp, has decided to send 10 OLED engineers to Sharp to help them develop their OLED display capabilities at Sharp’s Gen 4.5 OLED pilot line. Innolux itself was born from the 2003 merger of Chi Mei Optoelectronics and TPO Display Corp, with Chi Mei having one of the most forward looking OLED development units even in those early days. Chi Mei showed us a number of OLED displays way back in 2009, that were of high enough quality to be released as commercial products, however OLED funding was cut way back as Innolux faced significant financial difficulties, and the products were never realized.

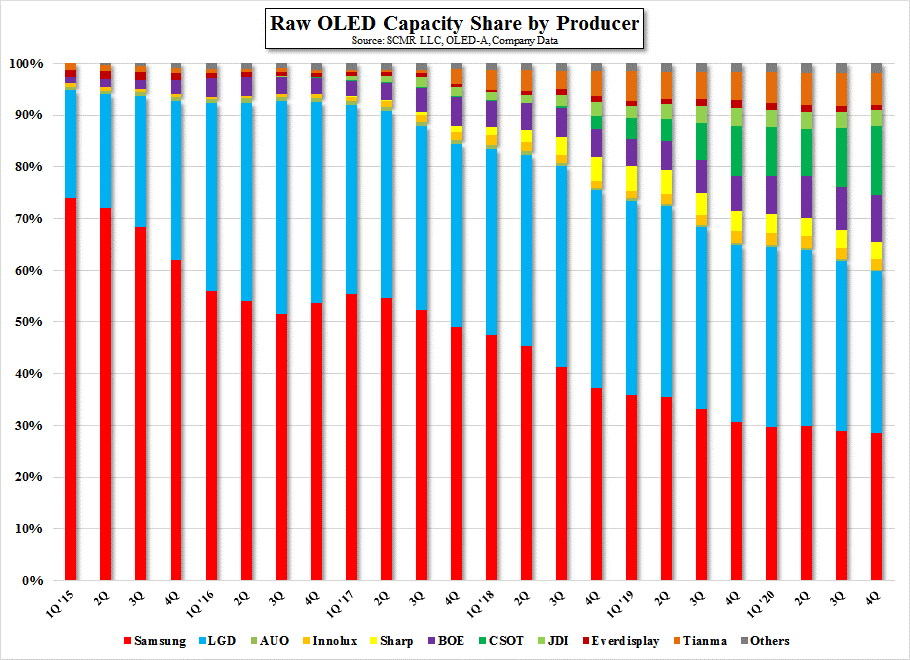

The new combination of Innolux and Sharp, in terms of gross display capacity, would be ranked just slightly behind capacity leader LG Display (22.3%) at 22.1%, and significantly above rival Samsung Display’s 12.6%, however when looking at OLED capacity, the combined Innolux and Sharp barely register at 1.4% against Samsung Display’s 54.7% and LG Display’s 36.0%. As Apple is expected to enter the OLED display space as a potential user of OLED for its iPhone line, all panel producers are scrambling to expand their efforts and prove to the industry (read, Apple) that they too can become a supplier of small panel OLED displays, despite their lack of previous funding in most cases, and certainly at Innolux and Sharp. Fig. 4[1] shows our OLED industry share expectations based on current capex, construction timelines, and producer experience, although actual available capacity would be smaller, particularly for those with little OLED mass production experience. Hopefully, the OLED engineers being sent from Innolux to Sharp will help to accelerate the combined company’s OLED R&D program, but there is a lot of ground to cover before being able to catch up to the leaders who will not be standing still.

[1] Innolux and Sharp are represented by the two yellow chart segments

The new combination of Innolux and Sharp, in terms of gross display capacity, would be ranked just slightly behind capacity leader LG Display (22.3%) at 22.1%, and significantly above rival Samsung Display’s 12.6%, however when looking at OLED capacity, the combined Innolux and Sharp barely register at 1.4% against Samsung Display’s 54.7% and LG Display’s 36.0%. As Apple is expected to enter the OLED display space as a potential user of OLED for its iPhone line, all panel producers are scrambling to expand their efforts and prove to the industry (read, Apple) that they too can become a supplier of small panel OLED displays, despite their lack of previous funding in most cases, and certainly at Innolux and Sharp. Fig. 4[1] shows our OLED industry share expectations based on current capex, construction timelines, and producer experience, although actual available capacity would be smaller, particularly for those with little OLED mass production experience. Hopefully, the OLED engineers being sent from Innolux to Sharp will help to accelerate the combined company’s OLED R&D program, but there is a lot of ground to cover before being able to catch up to the leaders who will not be standing still.

[1] Innolux and Sharp are represented by the two yellow chart segments

Raw OLED Capacity Share by Producer - Source: SCMR LLC, OLED-A

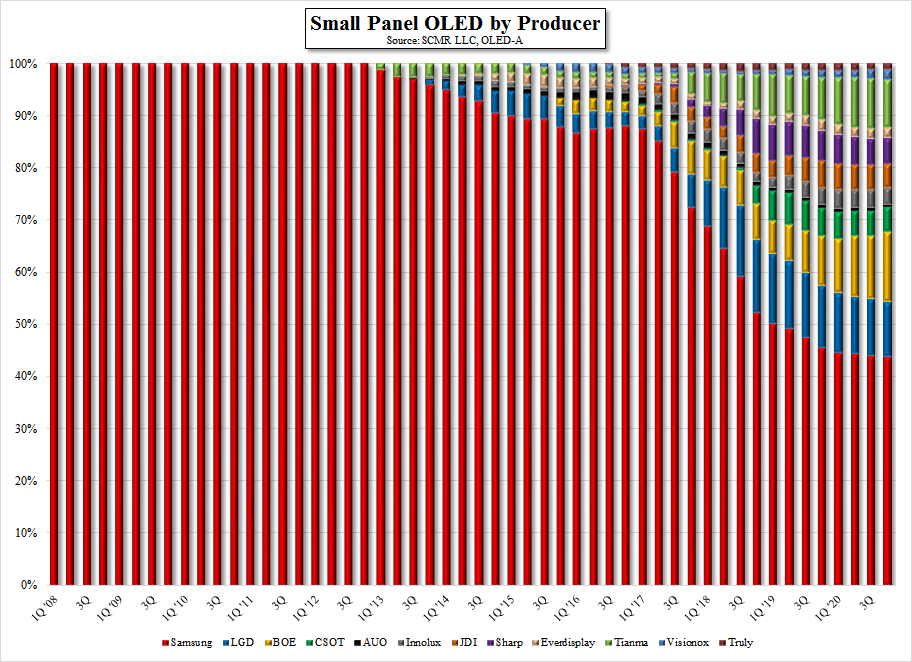

Small Panel OLED Capacity by Producer - Source: SCMR LLC, OLED-A

RSS Feed

RSS Feed