More on March Panel Results…These times are a changin'

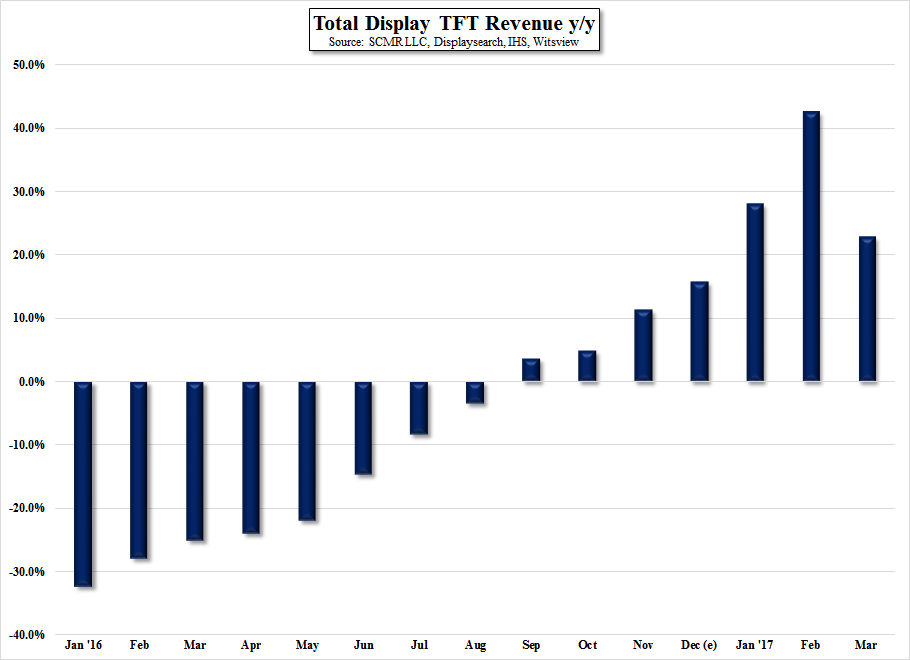

As we have noted in the past, panel demand and consequently panel pricing was extremely weak in the 1st half of 2016. This makes 2017 y/y comparisons a bit less relevant, as the gains will be greater than normal until 2H 2017. It can be seen in Fig. 1 how the comparisons turn positive starting in September of 2016, and have remained so thus far. The question is will they be able to sustain such positive y/y momentum for the rest of 2017, which we believe would be very difficult as we near the 2nd half. The rate of change had been increasing since January 2016, but peaked last month and should see harder comparisons for the rest of the year. Tables with March panel producer winners and losers are below.

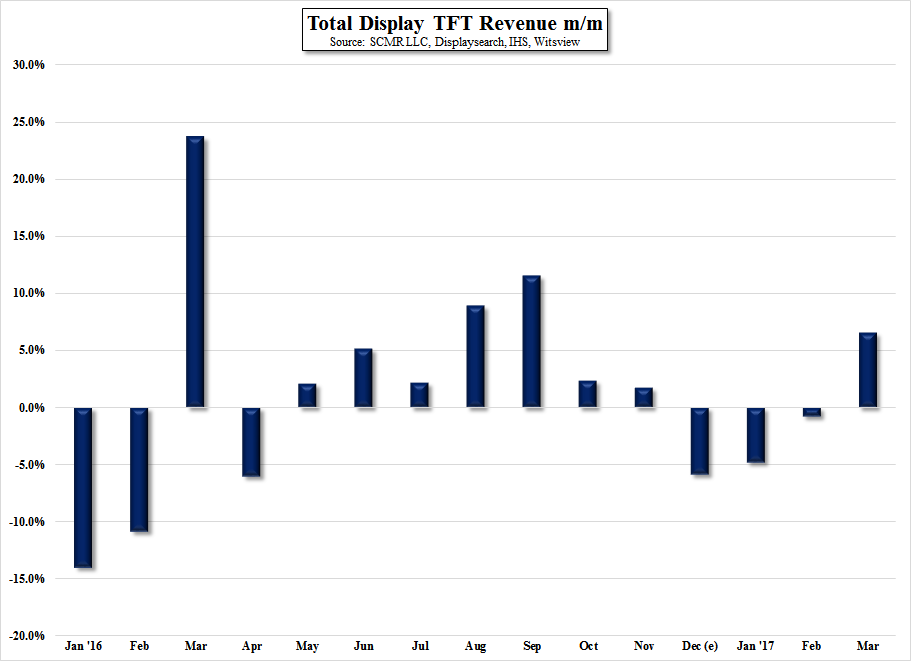

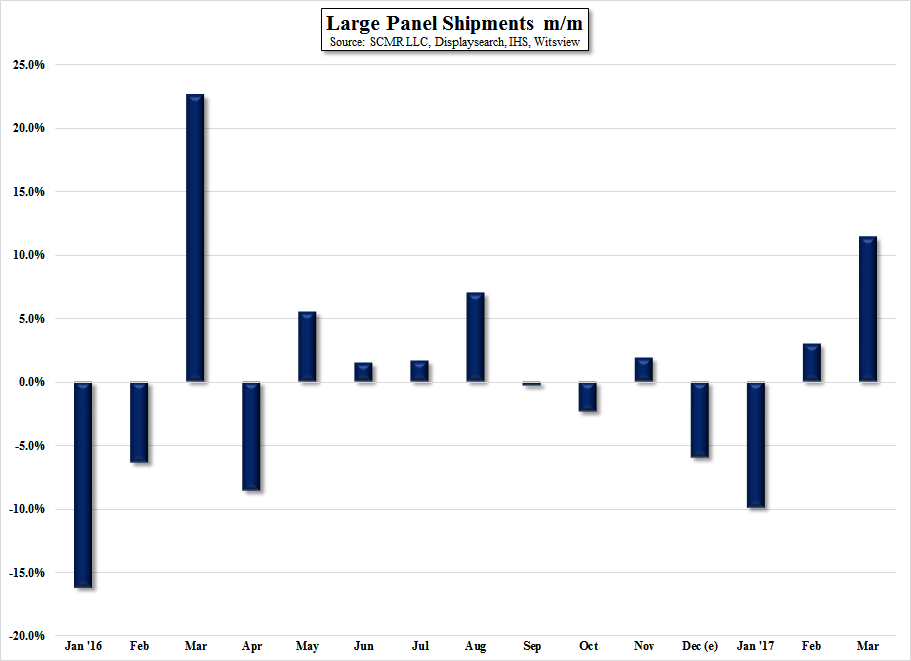

On a m/m basis, things look a bit different, with comparisons following a more seasonal pattern with January and February being weak comparisons, and March being a typical ‘bounce-back’ month. However, we note that during the previous months, panel pricing has been on the rise, while shipment growth (large panel) has been erratic. Panel pricing in April has been flat to down in all categories, so shipment growth become more important, and would be necessary to sustain positive m/m revenue gains across the industry. This leads us to expect weaker results in April from panel producers. At the brand levels, although it is a bit early to expect margin improvement, CE brands will begin to see less pressure on costs and will begin to have the ability to start being more aggressive toward retail discounting, at least in theory. That said, more likely CE brands will not start discounting to any large degree at the onset of 2Q, as they now have the chance to increase profits. If panel prices remain flat or decline going forward, the CE industry’s profitability will move from the panel producers (supply) to the CE brands (demand), a more typical scenario. This has significant implications for the industry, but given that May could be more of a defining month, we wait a bit before making assumptions for the rest of the year.

On a m/m basis, things look a bit different, with comparisons following a more seasonal pattern with January and February being weak comparisons, and March being a typical ‘bounce-back’ month. However, we note that during the previous months, panel pricing has been on the rise, while shipment growth (large panel) has been erratic. Panel pricing in April has been flat to down in all categories, so shipment growth become more important, and would be necessary to sustain positive m/m revenue gains across the industry. This leads us to expect weaker results in April from panel producers. At the brand levels, although it is a bit early to expect margin improvement, CE brands will begin to see less pressure on costs and will begin to have the ability to start being more aggressive toward retail discounting, at least in theory. That said, more likely CE brands will not start discounting to any large degree at the onset of 2Q, as they now have the chance to increase profits. If panel prices remain flat or decline going forward, the CE industry’s profitability will move from the panel producers (supply) to the CE brands (demand), a more typical scenario. This has significant implications for the industry, but given that May could be more of a defining month, we wait a bit before making assumptions for the rest of the year.

Total Display TFT Revenue y/y - Source: SCMR LLC, Displaysearch, IHS, Witsview

Total Display TFT Revenue - m/m - Source: CMR LLC, Displaysearch, IHS, Witsview

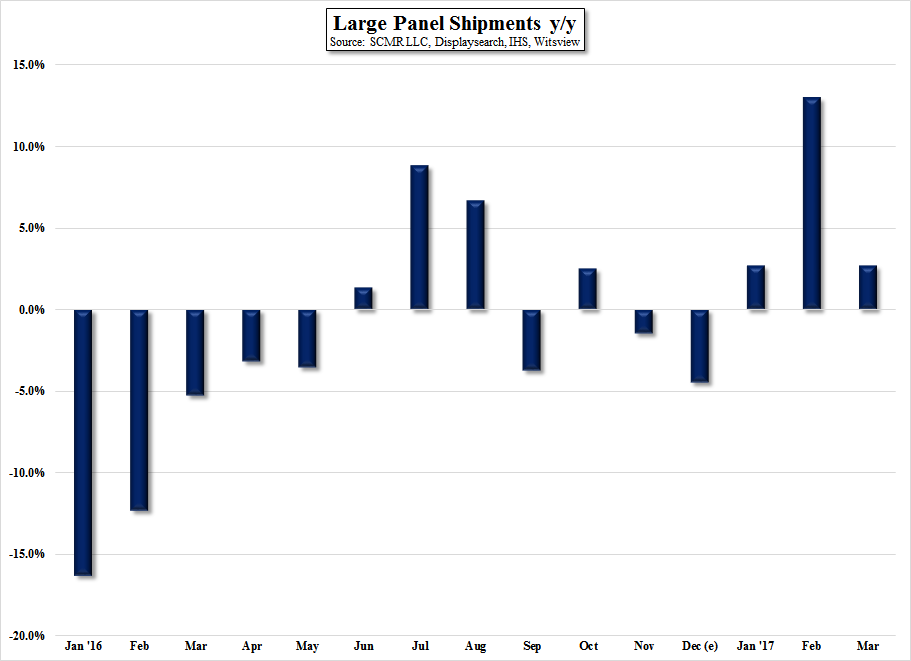

Large Panel Industry Shipments y/y - Source: SCMR LLC, Displaysearch, IHS, Witsview

Large Panel Industry Shipments m/m - Source: SCMR LLC, Displaysearch, IHS, Witsview

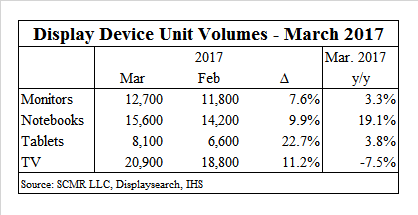

Display Device Unit Volumes - March 2017 - Source: SCMR LLC, Displaysearch, IHS

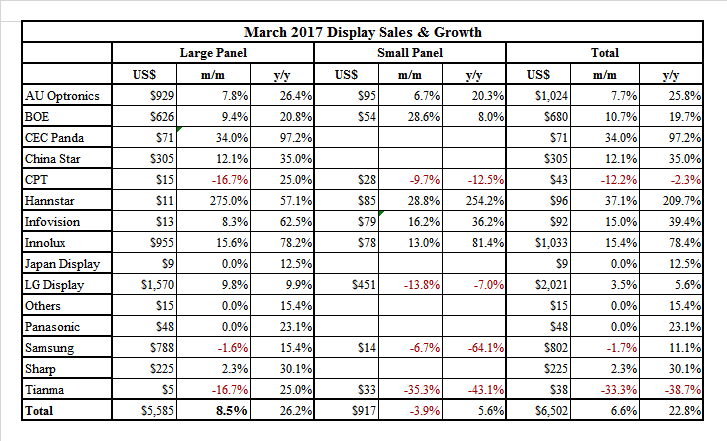

March Panel Producer Sales and Growth - Source: SCMR LLC, Displaysearch, IHS

RSS Feed

RSS Feed