April Panel Prices – Final

Another ‘unprecedented’ month for LCD panel price increases and once again those increases were higher than our expectations. As we get further into uncharted panel pricing territory, we look at the longer-term data for a better understanding of the implications that such panel price increases will have on the CE space, but even our regular panel price charts show the rapidly increasing prices and the unusually high level of m/m increases. In an additional set of charts, we look at how much of a price increase today’s panel prices are against yearly panel price highs and lows over the last 5 years.

While broad-based semiconductor shortages have plagued almost the entire CE supply chain, there have been some specific silicon issues that have continued to push panel production prices higher. Timing controllers (TCON), which control which pixel is receiving data and when, are basic necessities for displays, and remain in short supply. While there are a number of suppliers of TCONs and drivers for the display space, most are fabless, which means they are competing for foundry capacity with many other products and face the same supply issues as other semi products, which pushes foundries to both raise prices and give priority to their largest customers and products where they derive the most profit.

Glass substrate prices, which historically decline, have been relatively stable, and most recently, after a few mishaps and glass facilities, glass prices are rising, adding to the price of panel production. That said, brands continue to hold onto aggressive CE targets, which gives panel producers, usually in the lesser bargaining position, almost free reign to raise prices faster than costs increase. Chinese suppliers, who have become the dominant suppliers of LCD displays, are seeing this situation as a chance to justify their aggressive LCD capacity expansion over the last few years, and will continue to raise panel prices given their leading status. This gives them much ammunition when negotiating with provincial and local governments for capital to continue that expansion into OLED and LED based displays, albeit in a potentially cyclical space.

The result of panel price increases of the magnitude seen here are higher prices at the brand level, and as COVID-19 still seems to be a lifestyle changing factor on a global basis, the raid vaccination process in the US is beginning to have an impact on demand. In fact, demand continues strong for CE products on a global basis, but we expect a bit less demand from the US later this year if the rest of the population accepts the vaccine as readily as the first 20% of the population. We expect there will be a demand surge for certain iCE items as the US population begins to step out of what amounts to quasi-quarantine, but higher CE prices and a lesser focus on filling time in front of a display will have some effect on demand.

The global CE space however will likely stabilize less quickly and demand for educational CE (notebooks, monitors) will likely continue until new case levels on a global basis, or at least in developed countries, begin to decline in earnest, and some kind of supply/demand balance returns to the space, but the rapidly rising prices do represent a deterrent to a return to normality for CE products, as high-priced inventory will built into CE prices as 2021 progresses, leaving CE brands with margins that might not support the aggressive volume estimates they have now. While we would not expect panel producers to keep in mind such factors when deciding to raise prices, some restraint might help to sustain the length of their positive results. Just a thought…

While broad-based semiconductor shortages have plagued almost the entire CE supply chain, there have been some specific silicon issues that have continued to push panel production prices higher. Timing controllers (TCON), which control which pixel is receiving data and when, are basic necessities for displays, and remain in short supply. While there are a number of suppliers of TCONs and drivers for the display space, most are fabless, which means they are competing for foundry capacity with many other products and face the same supply issues as other semi products, which pushes foundries to both raise prices and give priority to their largest customers and products where they derive the most profit.

Glass substrate prices, which historically decline, have been relatively stable, and most recently, after a few mishaps and glass facilities, glass prices are rising, adding to the price of panel production. That said, brands continue to hold onto aggressive CE targets, which gives panel producers, usually in the lesser bargaining position, almost free reign to raise prices faster than costs increase. Chinese suppliers, who have become the dominant suppliers of LCD displays, are seeing this situation as a chance to justify their aggressive LCD capacity expansion over the last few years, and will continue to raise panel prices given their leading status. This gives them much ammunition when negotiating with provincial and local governments for capital to continue that expansion into OLED and LED based displays, albeit in a potentially cyclical space.

The result of panel price increases of the magnitude seen here are higher prices at the brand level, and as COVID-19 still seems to be a lifestyle changing factor on a global basis, the raid vaccination process in the US is beginning to have an impact on demand. In fact, demand continues strong for CE products on a global basis, but we expect a bit less demand from the US later this year if the rest of the population accepts the vaccine as readily as the first 20% of the population. We expect there will be a demand surge for certain iCE items as the US population begins to step out of what amounts to quasi-quarantine, but higher CE prices and a lesser focus on filling time in front of a display will have some effect on demand.

The global CE space however will likely stabilize less quickly and demand for educational CE (notebooks, monitors) will likely continue until new case levels on a global basis, or at least in developed countries, begin to decline in earnest, and some kind of supply/demand balance returns to the space, but the rapidly rising prices do represent a deterrent to a return to normality for CE products, as high-priced inventory will built into CE prices as 2021 progresses, leaving CE brands with margins that might not support the aggressive volume estimates they have now. While we would not expect panel producers to keep in mind such factors when deciding to raise prices, some restraint might help to sustain the length of their positive results. Just a thought…

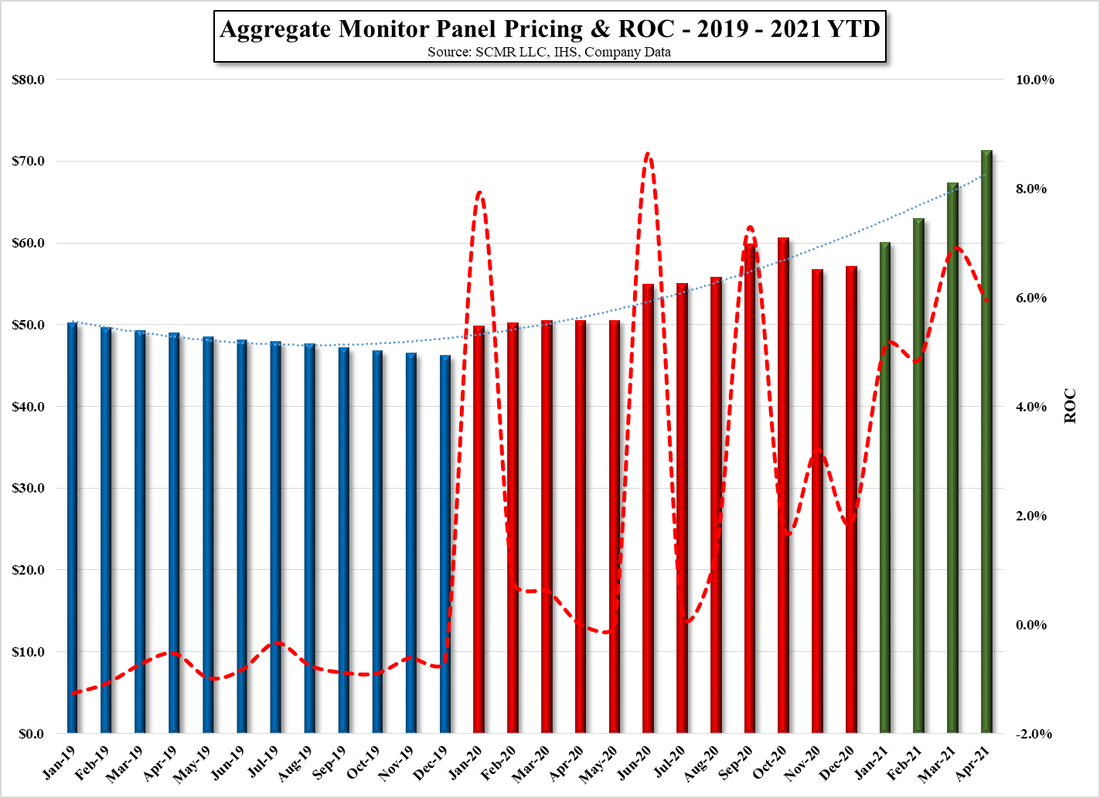

Aggregate Monitor Panel Pricing & ROC - 2019 - 2021 YTD – Source: SCMR LLC, HIS, Company Data

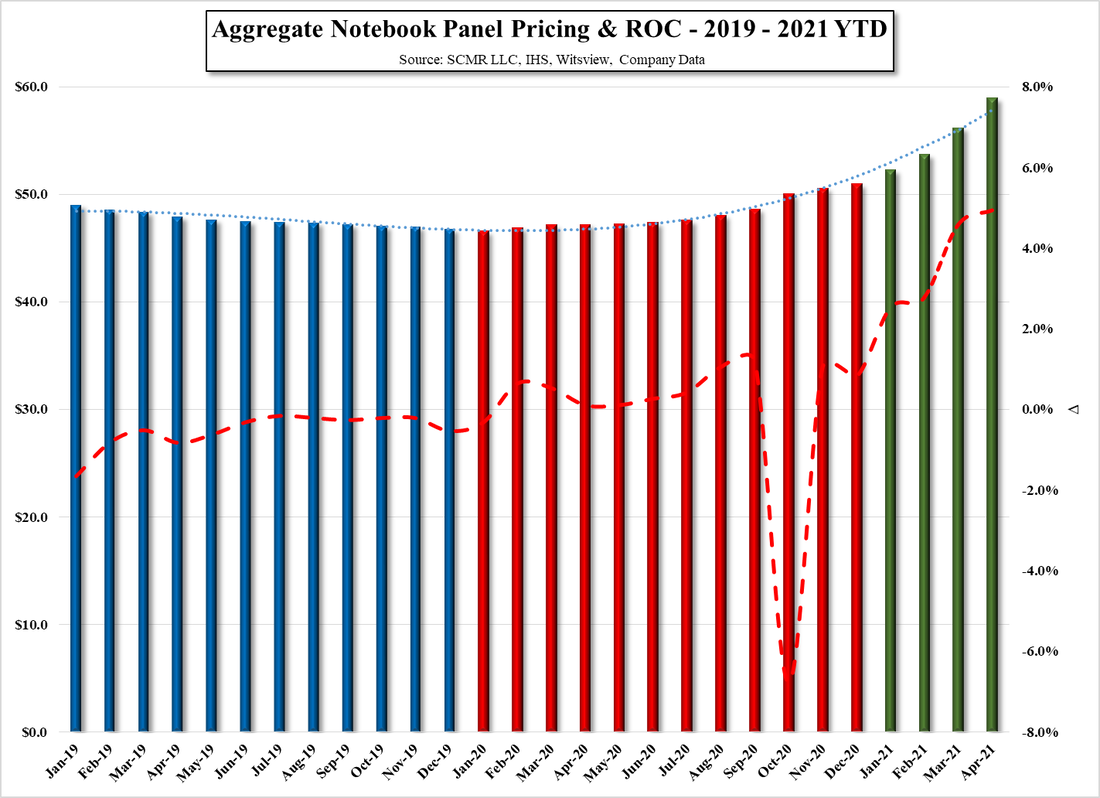

Aggregate Notebook Panel Pricing & ROC - 2019 -2021 YTD - Source: SCMR LLC, IHS, Witsview, Company Data

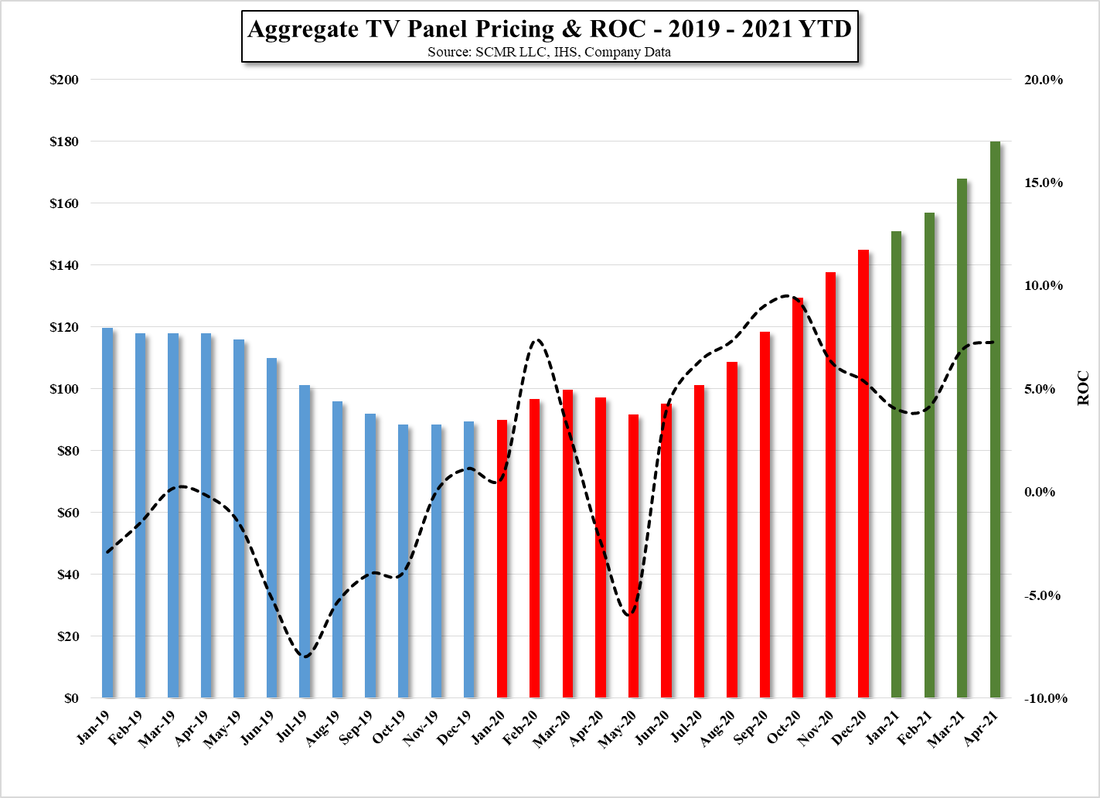

Aggregate TV Panel Pricing & ROC - 2019 - 2021 YTD - Source: SCMR LLC, IHS, Witsview, Company Data

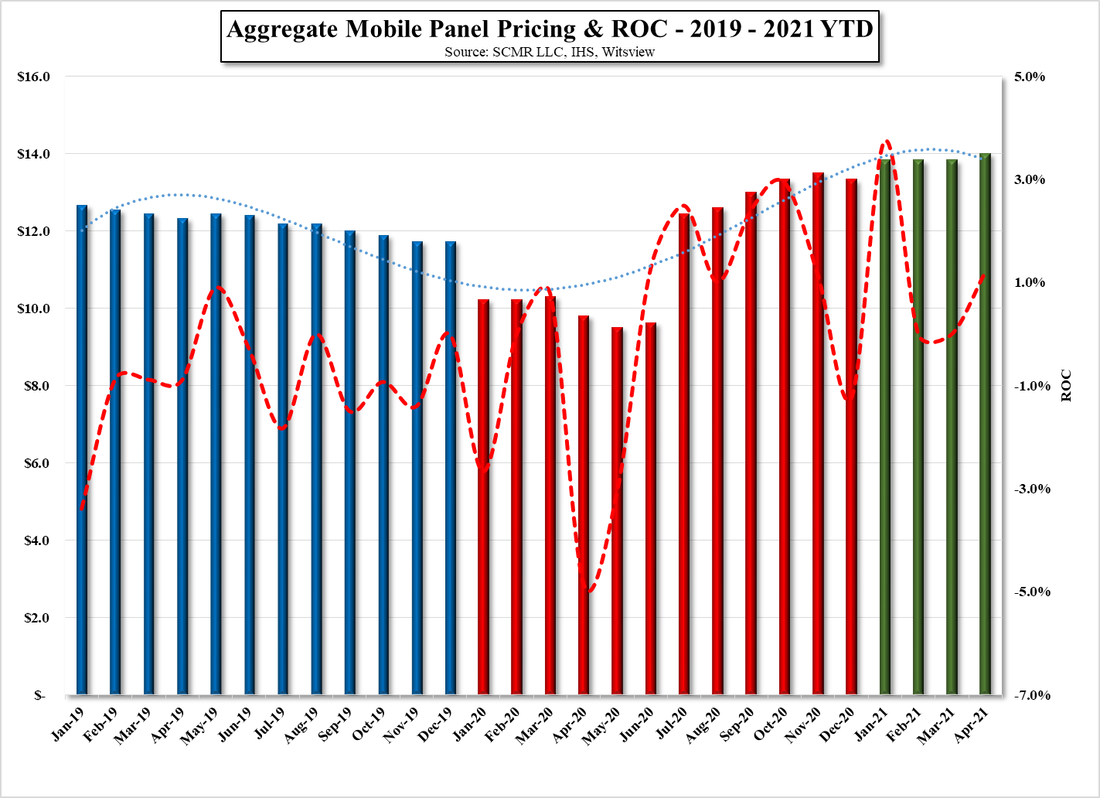

Aggregate Mobile Panel Pricing & ROC - 2019 - 2021 YTD - Source: SCMR LLC, IHS, Witsview, Company Data

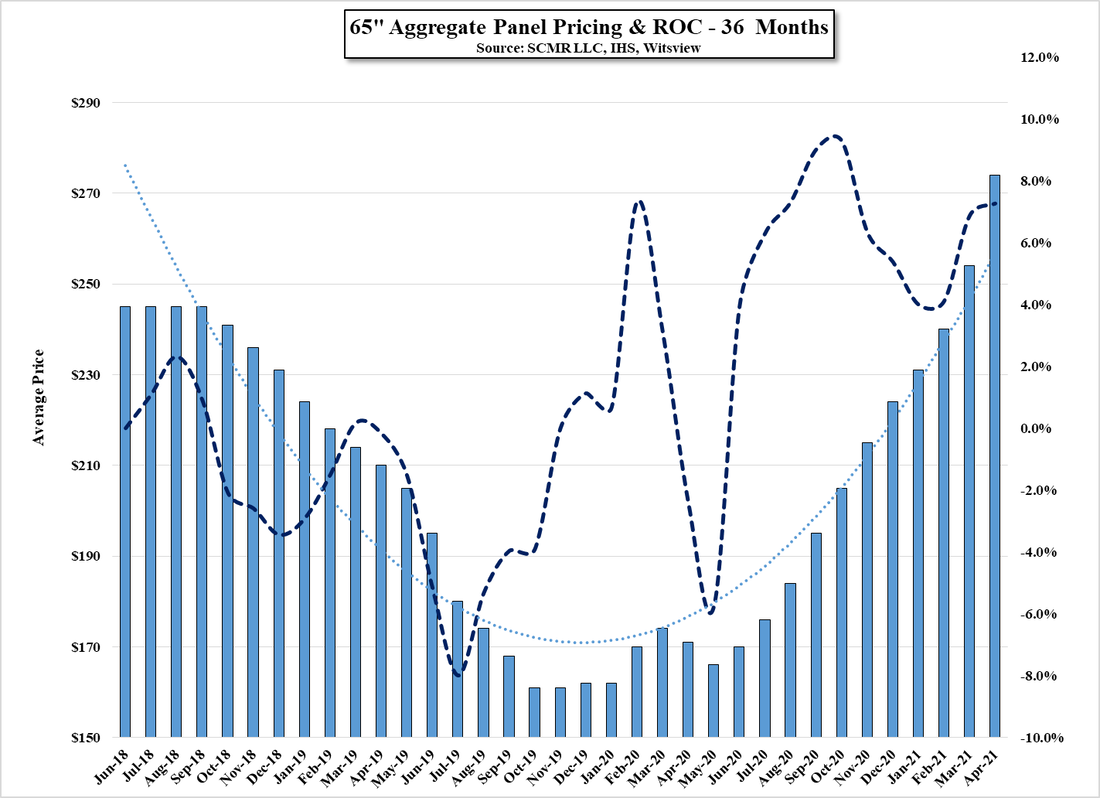

65" Aggregate Panel Pricing & ROC - 36 Months - Source: SCMR LLC, IHS, Witsview

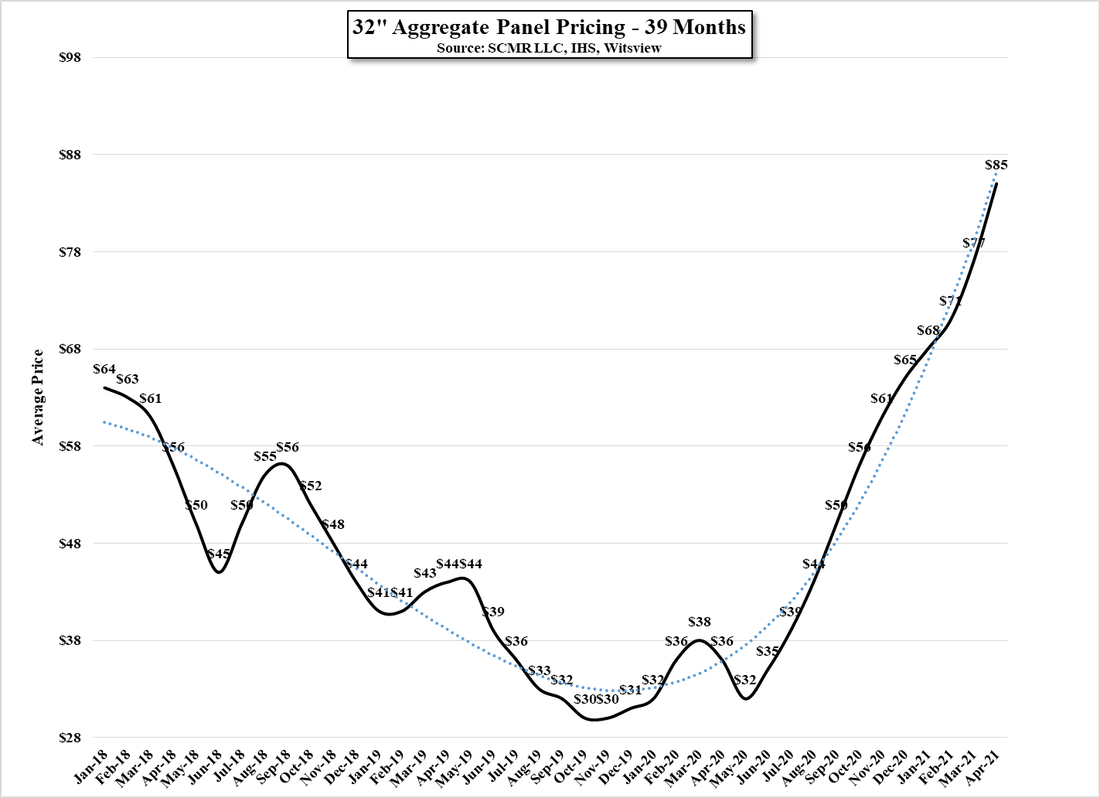

32" Aggregate Panel Pricing - 36 Months - Source: SCMR LLC, IHS, Witsview, Company Data

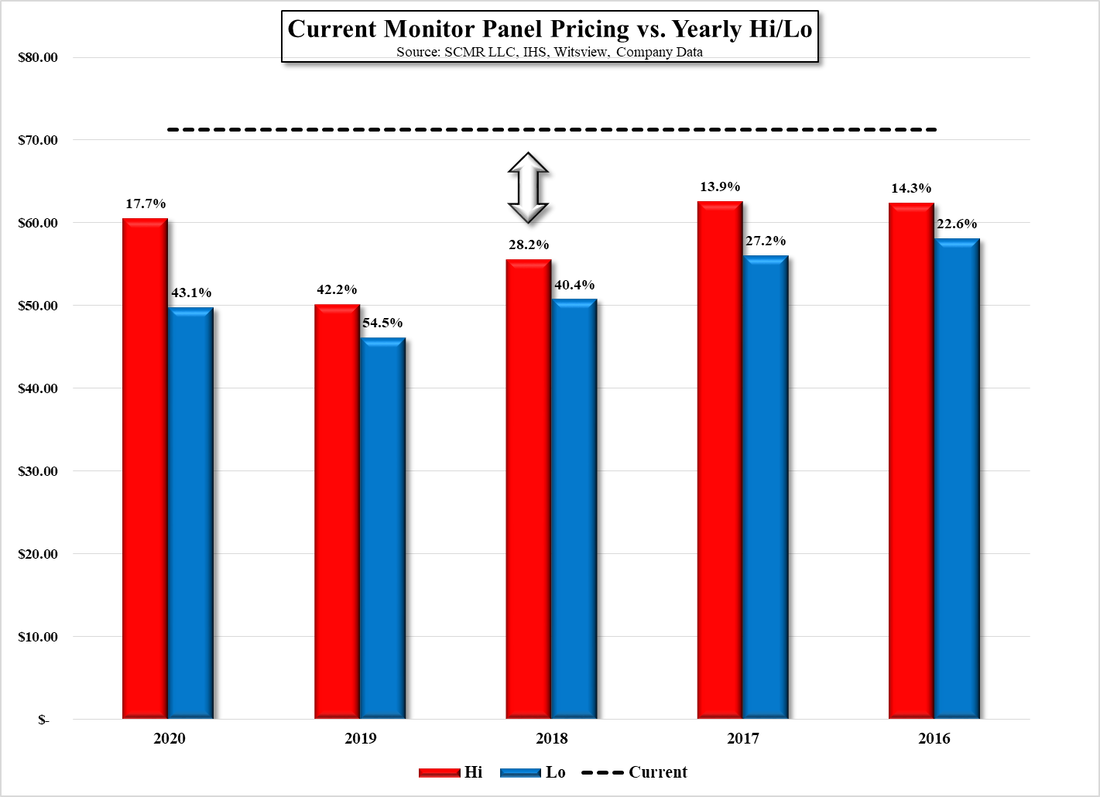

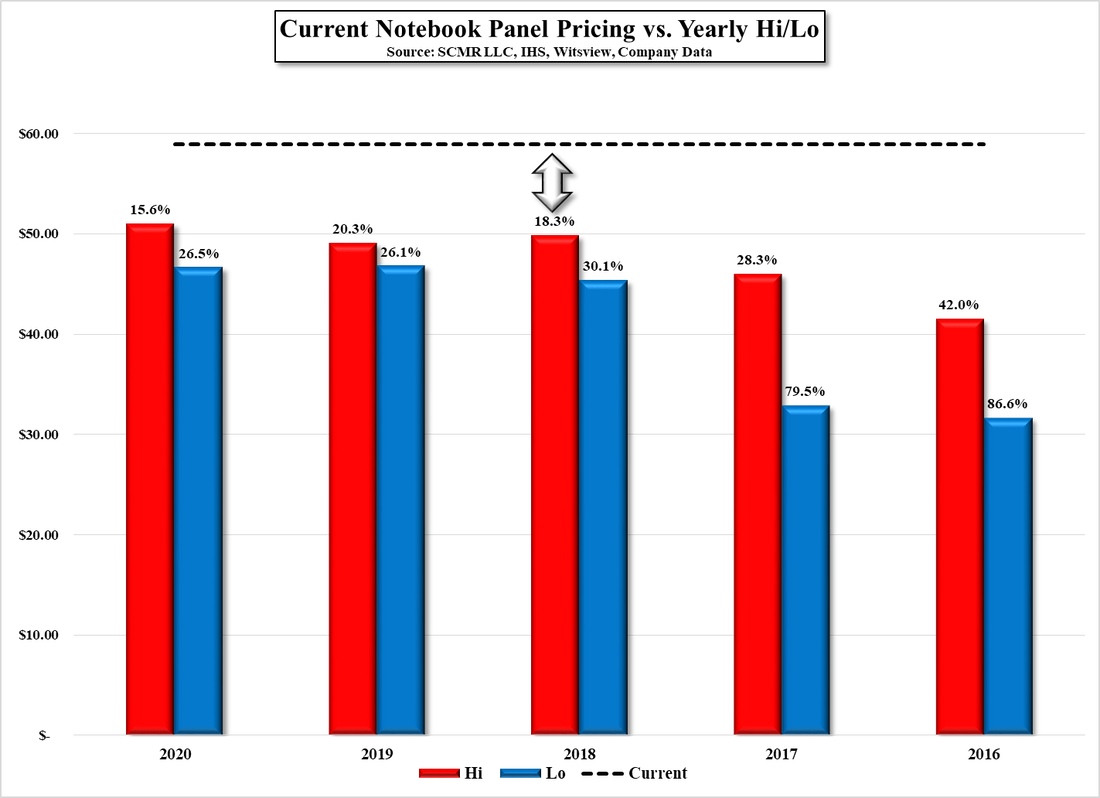

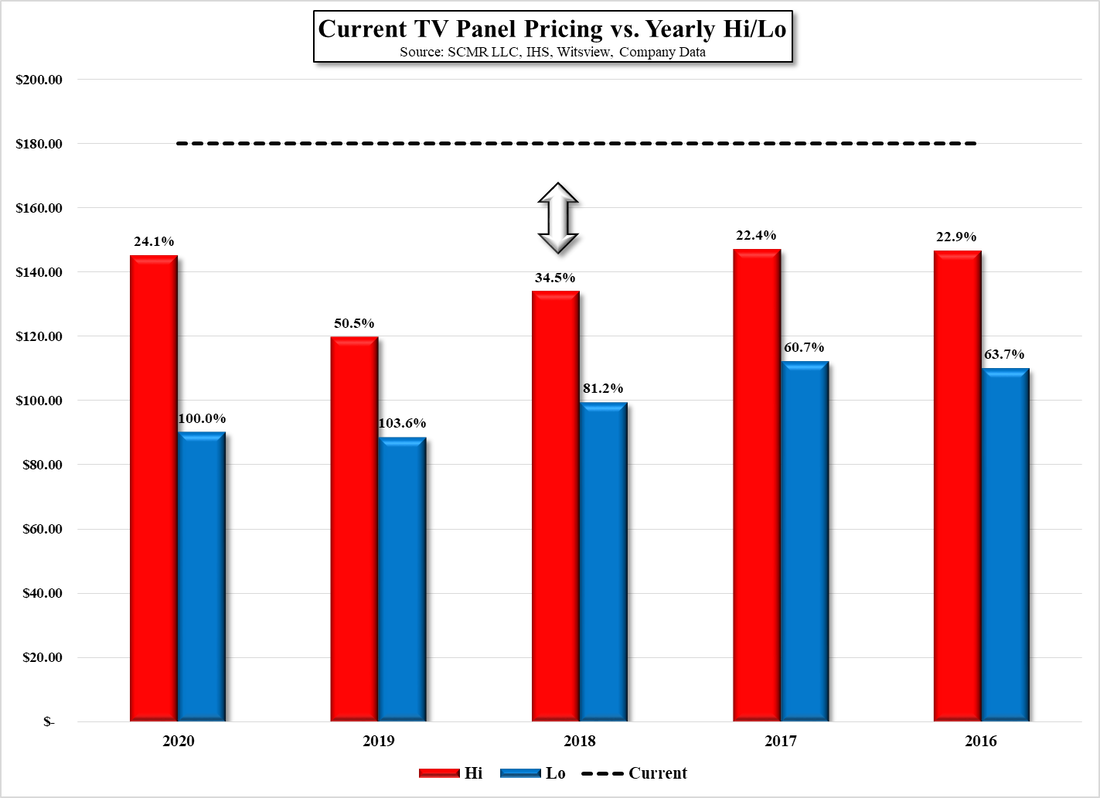

We note that the charts below show yearly high and low panel pricing and the difference between those and current panel prices in each of three categories. We exclude mobile only because the products available change so often (size, resolution, etc) that the data in past years has less relevance to current prices than other panel categories. Most telling is the difference between the current TV panel aggregate price and the low points in each year, with 2020 being the extreme due to COVID-19. That said, TV panel prices currently are also up over 100% from the 2019 low and ranges from 39.0% to 73.1% above the hi/lo average for each year, which shows that while 2020 was an anomaly, TV panel prices have still increased by very significant amount using 5 years of data.

Current Monitor Panel Pricing vs. Yearly Hi/Lo - Source: SCMR LLC, IHS, Witsview, Company Data

Current Notebook Panel Pricing vs. Yearly Hi/Lo - Source: SCMR LLC, IHS, Witsview, Company Data

Current TV Panel Pricing vs. Yearly Hi/Lo - Source: SCMR LLC, IHS, Witsview, Company Data

RSS Feed

RSS Feed