China PCB Suppliers Holding Back

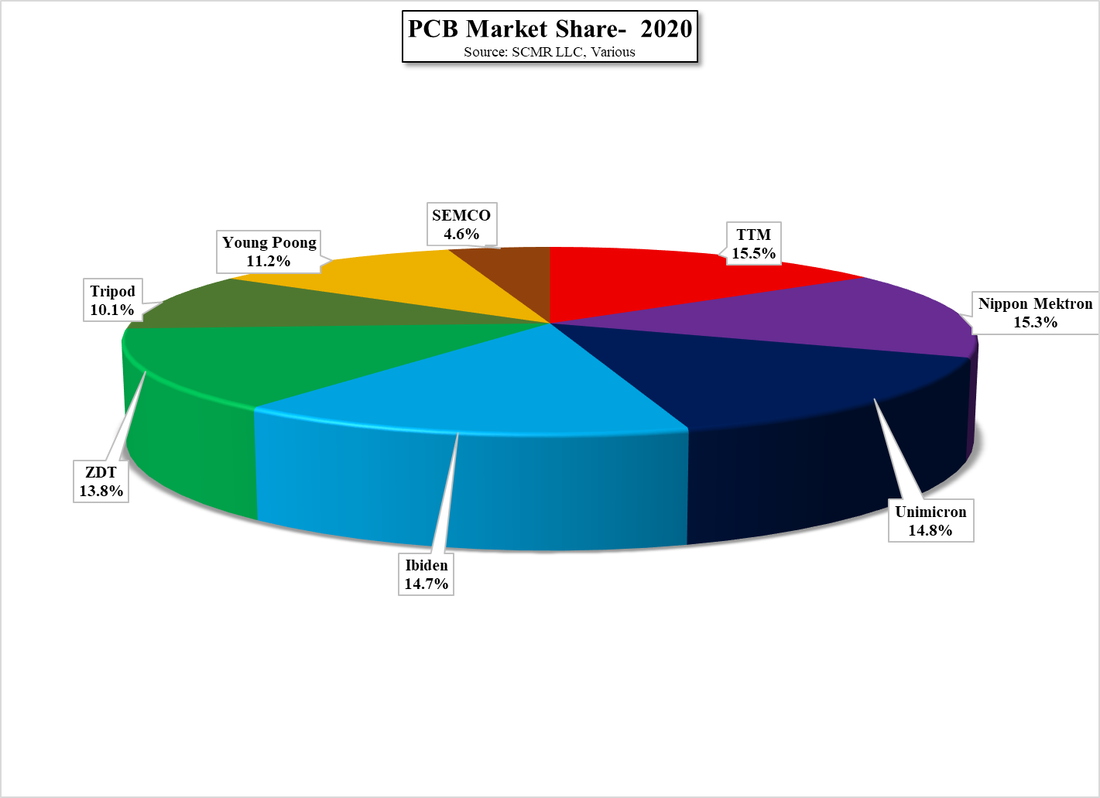

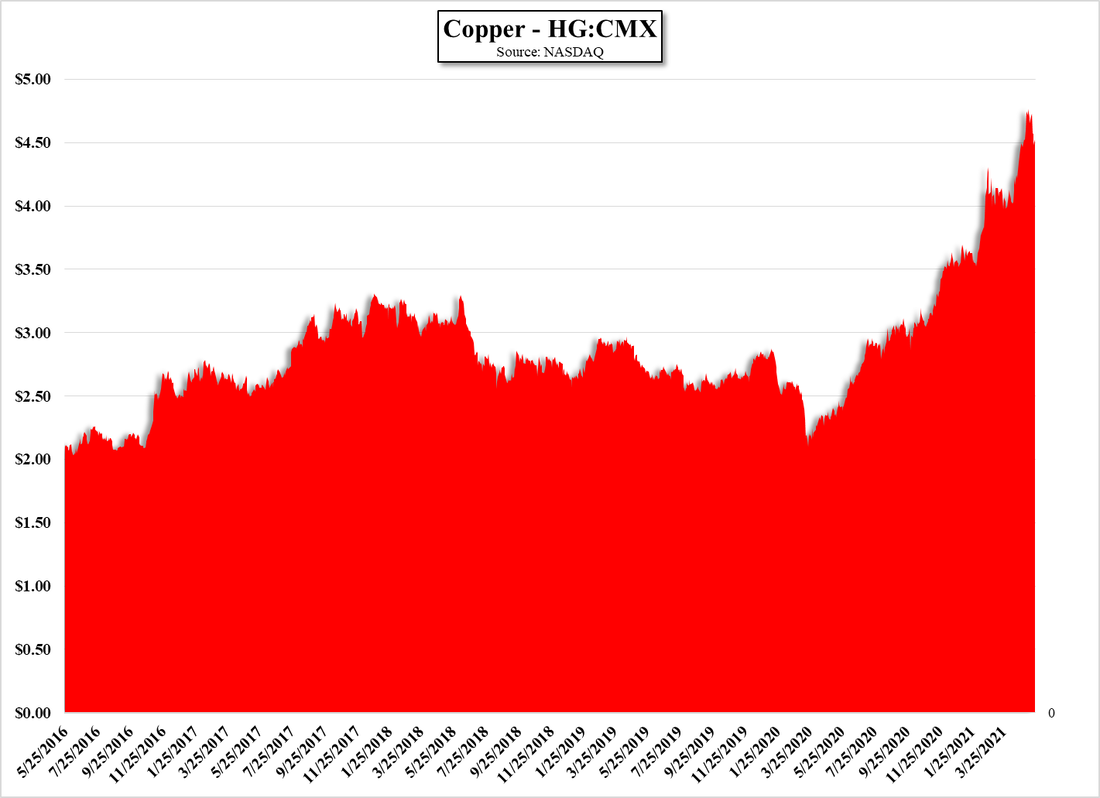

The generic PCB (Printed Circuit Board) business is mature, albeit highly competitive, with a number of companies with similar market share (Fig. 1). While PCBs seem like simple structures, depending on the application, they can become complex, with multiple interconnects, flexibility, and high density being determining factors. That said, the primary components of PCB boards themselves are a material called prepreg, which is a glass fiber fabric similar to what is used to make fiberglass boats, resin to harden the prepreg and laminate layers, copper for etched connections, and smaller amounts of nickel, gold, silver, or tin/lead. Unfortunately many of these materials are not specific to the manufacture of PCB boards but are in demand from a number of other industries. Copper is in particularly strong demand for lithium battery production and capacity is relatively static, leading to rapidly increasing prices for copper and copper foil (Fig. 2). Glass fiber is in demand from green energy applications, particularly in China, and manufacturers tend to favor those applications, which command higher prices, than those related to PCBs, and even epoxy resins have seen strong demand from similar applications (wind turbine blades), again from China.

While the highest share of PCB cost is in the design and layout of the board before it is produced, PCB manufacturers are seeing these material price increases eat away at margins. In most cases the price increases instituted by PCB producers lag the raw material price increases which leaves board manufacturers questioning whether they will see positive margins on orders, with some smaller producers in China refusing to take orders based on their evaluation of that particular order’s price structure, particularly at the low end of the market. Some of the larger producers are better able to negotiate with material suppliers, but we expect considerable consolidation in the industry among smaller players this year if material prices continue to rise. We do expect PCB material prices to continue to rise on a long-term basis, due to demand from some of the newer applications mentioned above, but the recent momentum is putting considerable strain on an industry that rarely has to compete with others for what are basic materials on which it functions.

While the highest share of PCB cost is in the design and layout of the board before it is produced, PCB manufacturers are seeing these material price increases eat away at margins. In most cases the price increases instituted by PCB producers lag the raw material price increases which leaves board manufacturers questioning whether they will see positive margins on orders, with some smaller producers in China refusing to take orders based on their evaluation of that particular order’s price structure, particularly at the low end of the market. Some of the larger producers are better able to negotiate with material suppliers, but we expect considerable consolidation in the industry among smaller players this year if material prices continue to rise. We do expect PCB material prices to continue to rise on a long-term basis, due to demand from some of the newer applications mentioned above, but the recent momentum is putting considerable strain on an industry that rarely has to compete with others for what are basic materials on which it functions.

PCB Market Share - 2020 - Source: SCMR LLC, Various

Copper - HG:CMX - Source: NASDAQ

RSS Feed

RSS Feed