Display in May

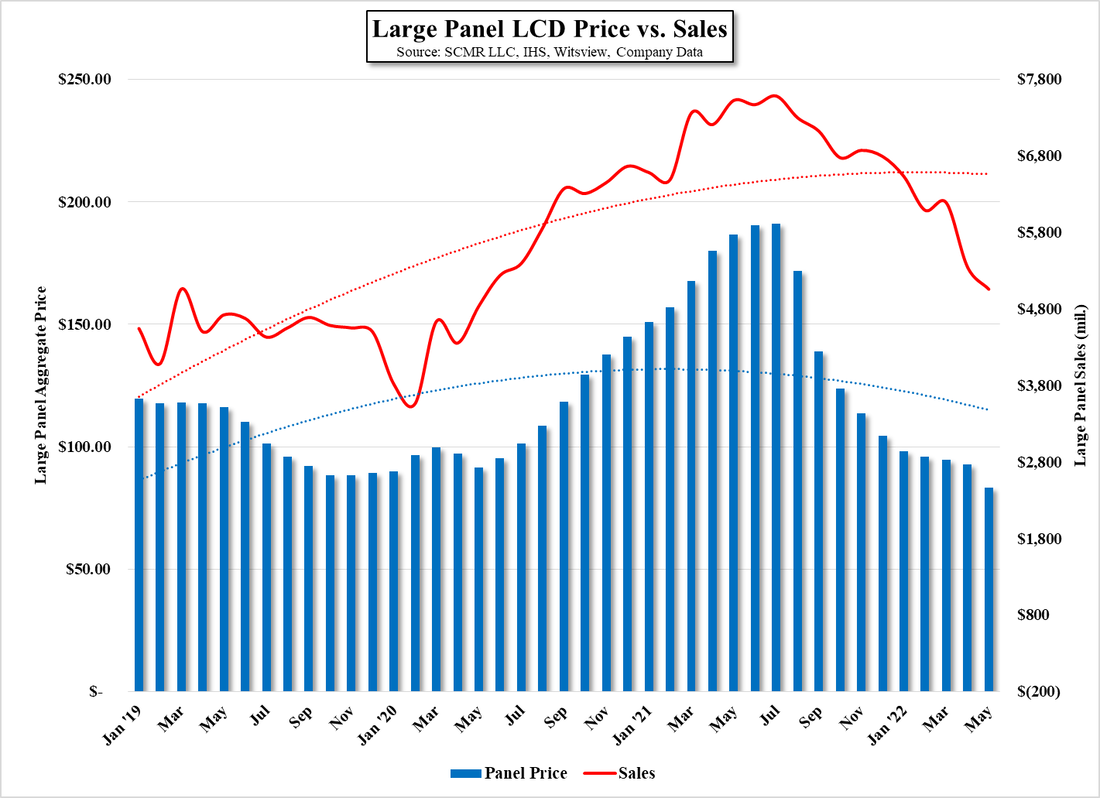

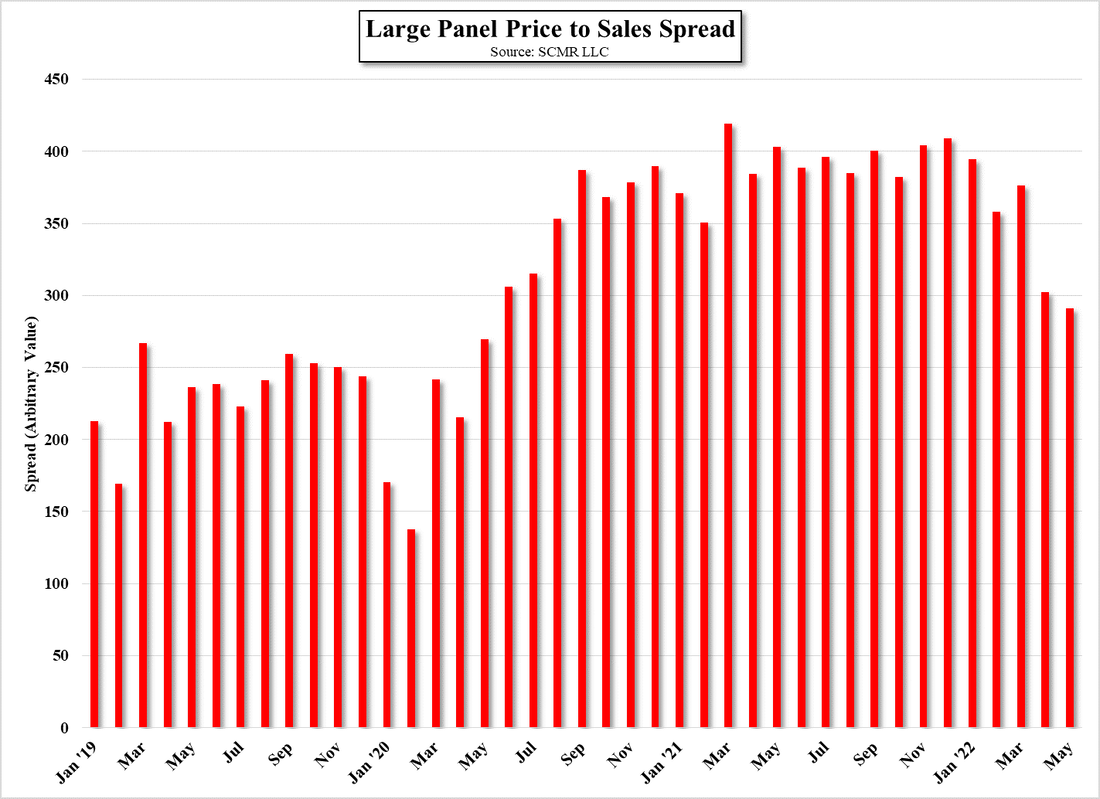

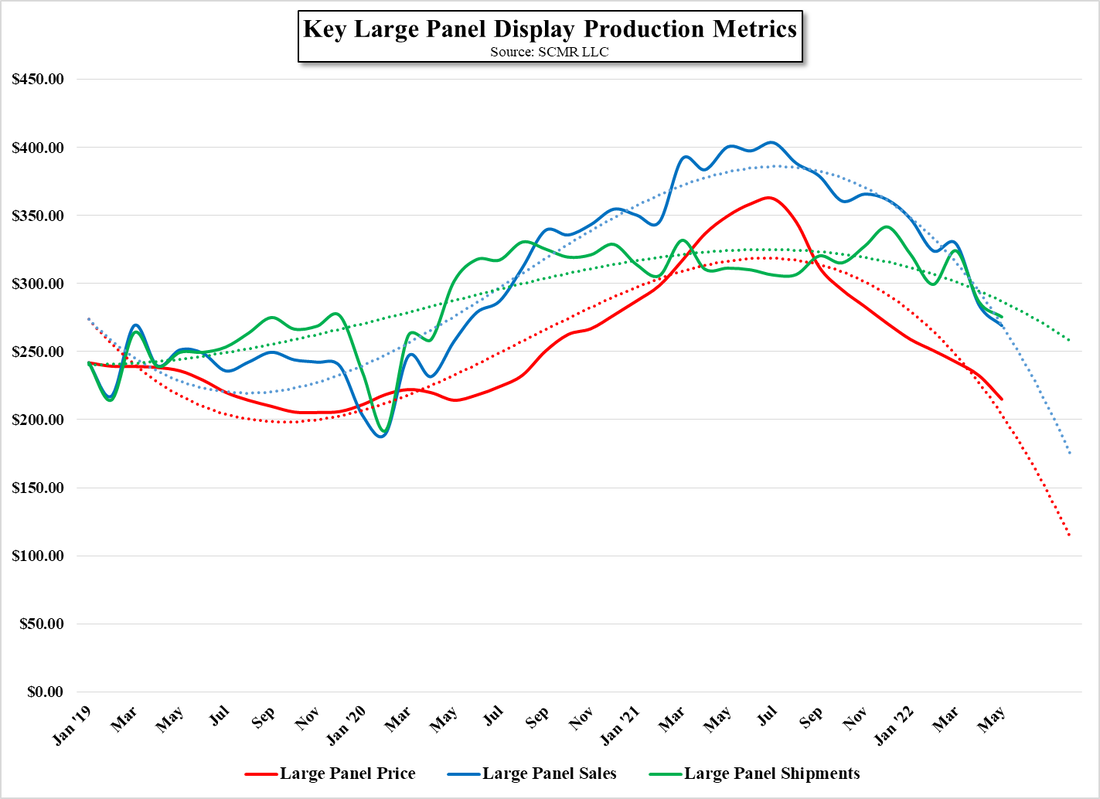

Since July of last year the revenue generated by large panel display producers has been on the decline, tracking closely to the decline in large panel display prices, however the spread between the two, which we plot as an arbitrary value in Figure 2, shows that the spread between the two has yet to reach pre-pandemic levels (avg. 2019 spread = 233), which would seemingly forecast a contraction in the spread going forward. Taking it one step further, we plot three key large panel display metrics for the same period, Price, Shipments, and sales, adjusting vales to a common starting point, and projecting out three months to see the result, which is shown in Figure 3, which indicates that by the end of August shipments will decline but sales will decline more rapidly as prices continue to decline, which would follow the utilization cuts at major LCD large panel suppliers that have been rumored in the trade press.

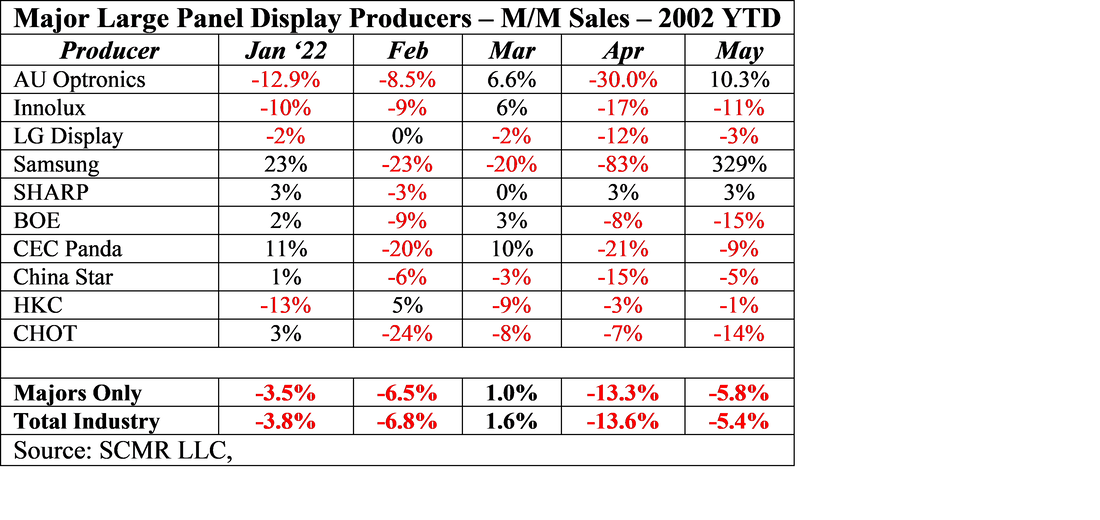

Making the scenario a bit more difficult is the fact that panel producers waited until June to make such utilization cuts, and the data for shipments in June will not be available for a few weeks, and with Chinese producers representing ~50% of industry large panel sales, the utilization reductions at BOE (200725.CH), Chinastar (pvt) and HKC (248.HK), who together represent 45.4% of total industry large panel display sales, and May large panel industry sales were down 5.4% m/m and 32.8% y/y, shipments were down less at -3.9% m/m and -11.5% y/y. Some producers have done better than others during this year, as shown in the table below, which shows only those producers that are primarily large panel suppliers. We note that Samsung Display (pvt) has been winding down its remaining LCD large panel production which accounts for the large swings shown below.

While orders from customers can make a substantial difference to m/m data for individual producers, we expect much of the negative growth for large panel LCD producers seen this year is a function of declining large panel prices, however in June we expect both large panel prices to decline and to also see the effects of utilization cut backs that have been rumored across much of the industry. If the cuts are substantial enough, they will have some effect on high inventory levels over the next two months, but if they are less than expected, and seasonal builds begin in August, we expect panel producers will face a very rocky 3rd and possibly 4th quarter this year. If that turns out to be the case, we would expect January/February ’23 to be especially week, as many fabs will essentially shut down for the latter part of January during the Chinese New Year holiday, which occurs on January 22

Making the scenario a bit more difficult is the fact that panel producers waited until June to make such utilization cuts, and the data for shipments in June will not be available for a few weeks, and with Chinese producers representing ~50% of industry large panel sales, the utilization reductions at BOE (200725.CH), Chinastar (pvt) and HKC (248.HK), who together represent 45.4% of total industry large panel display sales, and May large panel industry sales were down 5.4% m/m and 32.8% y/y, shipments were down less at -3.9% m/m and -11.5% y/y. Some producers have done better than others during this year, as shown in the table below, which shows only those producers that are primarily large panel suppliers. We note that Samsung Display (pvt) has been winding down its remaining LCD large panel production which accounts for the large swings shown below.

While orders from customers can make a substantial difference to m/m data for individual producers, we expect much of the negative growth for large panel LCD producers seen this year is a function of declining large panel prices, however in June we expect both large panel prices to decline and to also see the effects of utilization cut backs that have been rumored across much of the industry. If the cuts are substantial enough, they will have some effect on high inventory levels over the next two months, but if they are less than expected, and seasonal builds begin in August, we expect panel producers will face a very rocky 3rd and possibly 4th quarter this year. If that turns out to be the case, we would expect January/February ’23 to be especially week, as many fabs will essentially shut down for the latter part of January during the Chinese New Year holiday, which occurs on January 22

Large Panel LCD Prices vs. Sales - 2019 - 2022 - Source: SCMR LLC, IHS, WItsview, Company Data

Large Panel Price to Sales Spread - Source: SCMR LLC

Key Large Panel Display Production Metrics - Source: SCMR LLC

RSS Feed

RSS Feed