AU Optronics to Add LCD Capacity

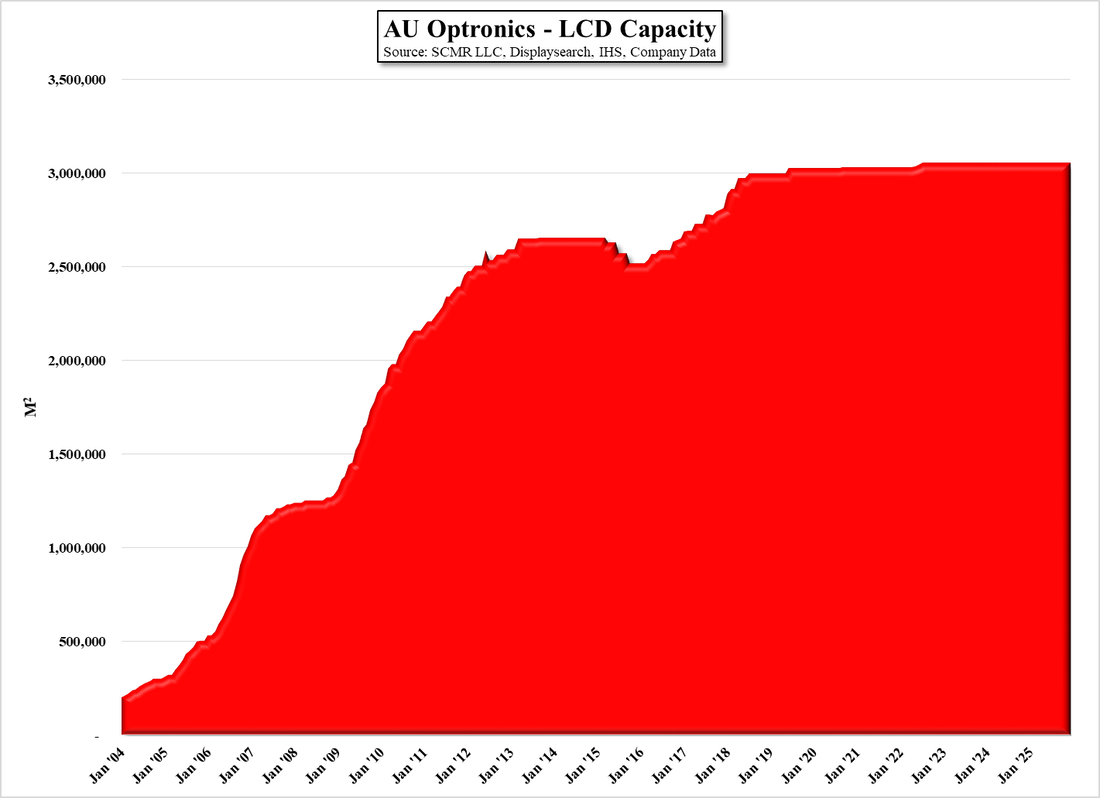

AU Optronics (AUOTY) has indicated that they will be adding a small amount of capacity to their Gen 6 line in Kunshan, China, which has been built out to 36,000 sheets/month, against a total potential capacity of 45,000 sheets/month. The increase, which will be put into production in the 3rd quarter of next year, will add another 9,000 sheets/month to the fab’s capacity or 0.45%. While that is a small amount of additional capacity, that fab is producing IT products, essentially monitor and notebook panels, so 9,000 sheets/month on an annualized basis represents 108,000 additional sheets, and if. For example, that production was split between 27” monitors and 14” notebook panels, at current panel prices that annualized increase in panel sales would come to $138.7m, or a 1.4% increase in sales for a 0.45% increase in capacity, assuming 100% utilization.

While these numbers are assuming panel prices stay at current levels, any further increase in IT panel prices would enhance the improvement, so the risk to AUO, as with all other panel capacity expansions, is when utilization starts to fall, which is usually accompanied by falling panel prices. Such a double whammy is the bane of panel producers, which is why AUO has almost always taken a more conservative stance toward panel capacity increases, focusing more on improving mix by adding more premium products. While cyclicality in the industry don’t always allow even this conservative philosophy to produce profits, it is the inverse of China’s panel producers’ philosophy, which is more focused on building share by rapidly increasing capacity.

Right now, given the high utilization rates and panel price increases seen over the last year, the Chinese philosophy wins out, but there is certainly something to be said for a more conservative approach to expansion and a greater focus on profitability. Last month the AUO board approved capex of NT$455m (~$16m US) for “factory and capacity optimization and adjustments.” Company management did note that they expected the shortage of key components to worsen in 2Q, as compared to 4Q ’20 and 1Q ’21, citing glass substrates, PCBs, and polarizers more specifically, along with ‘persistent’ IC supply issues, with component and material lead times extending to roughly eight weeks from a pre-pandemic four weeks.

While these numbers are assuming panel prices stay at current levels, any further increase in IT panel prices would enhance the improvement, so the risk to AUO, as with all other panel capacity expansions, is when utilization starts to fall, which is usually accompanied by falling panel prices. Such a double whammy is the bane of panel producers, which is why AUO has almost always taken a more conservative stance toward panel capacity increases, focusing more on improving mix by adding more premium products. While cyclicality in the industry don’t always allow even this conservative philosophy to produce profits, it is the inverse of China’s panel producers’ philosophy, which is more focused on building share by rapidly increasing capacity.

Right now, given the high utilization rates and panel price increases seen over the last year, the Chinese philosophy wins out, but there is certainly something to be said for a more conservative approach to expansion and a greater focus on profitability. Last month the AUO board approved capex of NT$455m (~$16m US) for “factory and capacity optimization and adjustments.” Company management did note that they expected the shortage of key components to worsen in 2Q, as compared to 4Q ’20 and 1Q ’21, citing glass substrates, PCBs, and polarizers more specifically, along with ‘persistent’ IC supply issues, with component and material lead times extending to roughly eight weeks from a pre-pandemic four weeks.

- AU Optronics - LCD Capacity - Source: SCMR LLC, Displaysearch, IHS, Company Data

RSS Feed

RSS Feed