AUO in June – Hints of What’s to Come

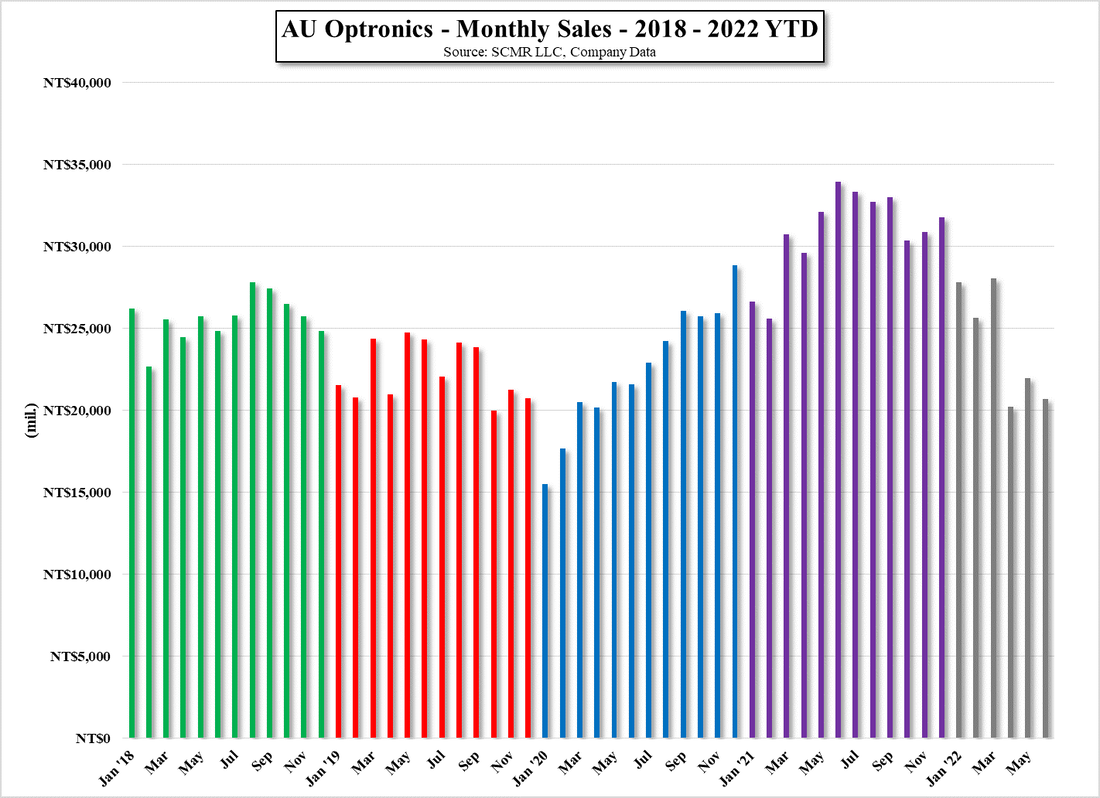

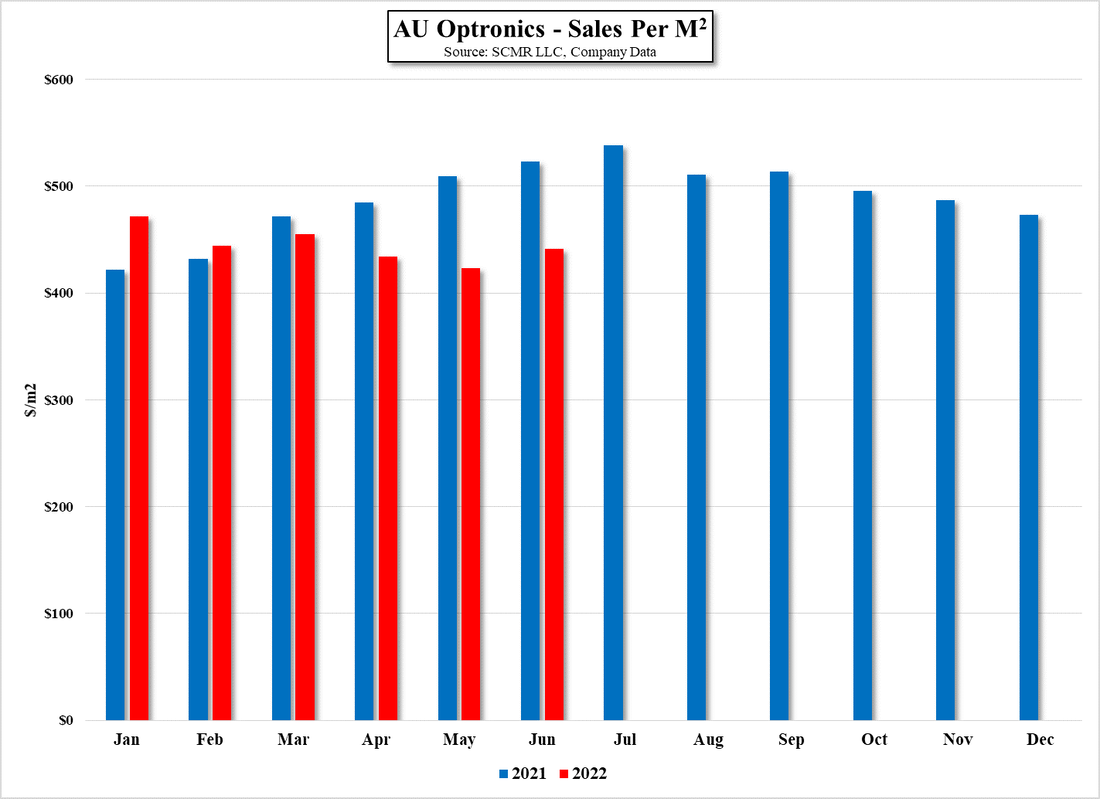

AU Optronics (2409.TT) reported June Sales of NT$20.69b ($69453m US), ↓5.8% m/m and ↓39.0% y/y, putting the 2nd quarter sales at NT$62.881b ($2.111b US), ↓22.9% q/q and ↓34.3% y/y and 1st half results are ↓19.1% y/y. Typically (5 year average) June is up 0.4% m/m and 2Q is up 7.0% q/q, so from any perspective June and 2Q were weak for AUO, although no surprising given the weakness seen across the CE space and the display space in particular, as overall display panel prices declined 12.0% during the 2nd quarter and panel orders from brands were reduced. Area shipped was 1.59m m2, ↓9.7% m/m and we do note (see Figure 2) that AUO has been able to maintain fab efficiency (not utilization), meaning the sales value of each m2 of display produced, at a reasonable level since the beginning of the year, which points to the company’s focus on high value display products rather than generic displays.

While we wait for Innolux (3481.TT) and Hannstar (6116.TT) to report June sales and shipments to complete the Taiwan panel producer data, we expect July results for most panel producers will see further declines, more weighted toward order reductions than price declines, giving a messy start to 3Q. With Samsung Electronics (005930.KS) reducing or eliminating TV panel orders from suppliers to reduce inventory, as we have previously noted, it will be difficult for panel producers to maintain production at earlier levels, unless they are willing to offer larger discounts than in previous months, which will amplify panel price declines. Our hope is that the order cuts will be enough to reduce inventory to more normal levels by mid-August, and that the panel price declines that have been evident for part of last year and the 1st half of 2022 will slow to more ‘normal’ levels as we enter September. Brand targets have been reduced but consumers have yet to jump at discounts thus far, and the macro environment leaves a bit to be desired, so again we look at such prospects as possible but less probable than an extension of the current CE malaise into 4Q. As of yet there are few signs pointing toward a better than expected outcome, but we keep looking.

While we wait for Innolux (3481.TT) and Hannstar (6116.TT) to report June sales and shipments to complete the Taiwan panel producer data, we expect July results for most panel producers will see further declines, more weighted toward order reductions than price declines, giving a messy start to 3Q. With Samsung Electronics (005930.KS) reducing or eliminating TV panel orders from suppliers to reduce inventory, as we have previously noted, it will be difficult for panel producers to maintain production at earlier levels, unless they are willing to offer larger discounts than in previous months, which will amplify panel price declines. Our hope is that the order cuts will be enough to reduce inventory to more normal levels by mid-August, and that the panel price declines that have been evident for part of last year and the 1st half of 2022 will slow to more ‘normal’ levels as we enter September. Brand targets have been reduced but consumers have yet to jump at discounts thus far, and the macro environment leaves a bit to be desired, so again we look at such prospects as possible but less probable than an extension of the current CE malaise into 4Q. As of yet there are few signs pointing toward a better than expected outcome, but we keep looking.

AU Optronics - Monthly Sales - 2018 - 2022 YTD - Source: SCMR LLC, Company Data

AU Optronics - Sales Per M2 - Source: SCMR LLC, Company Data

RSS Feed

RSS Feed