5G Ecosystem – Short Versio

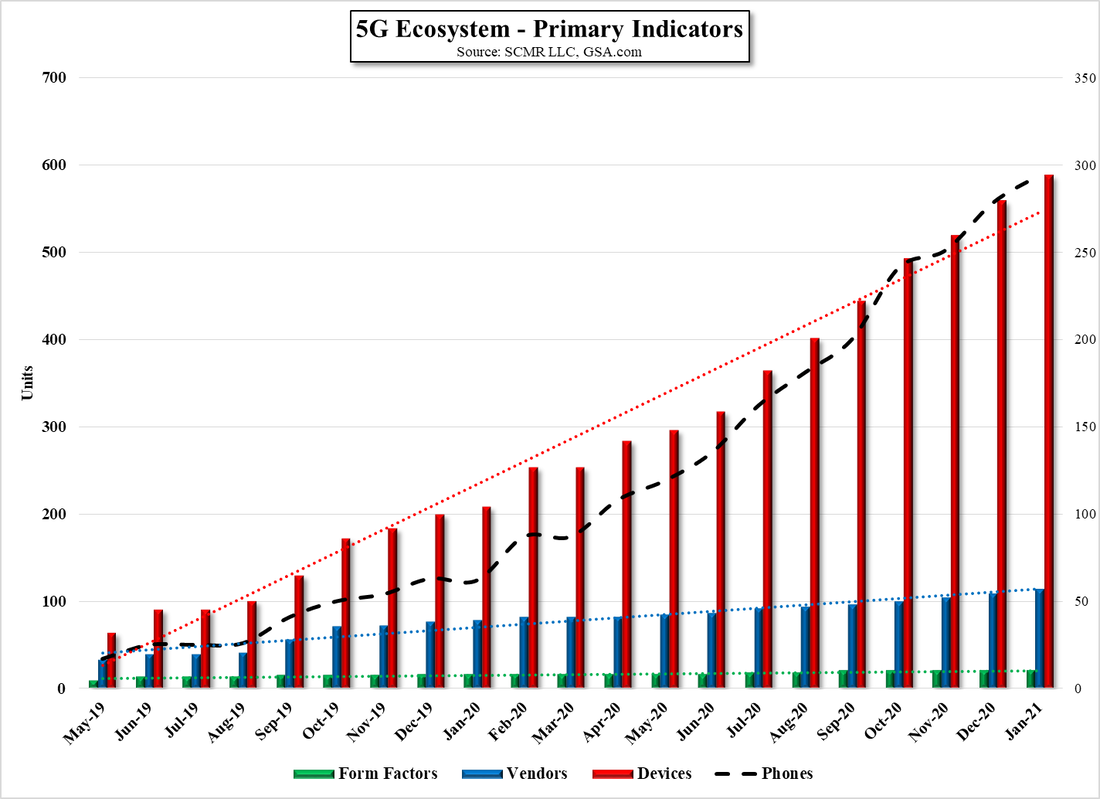

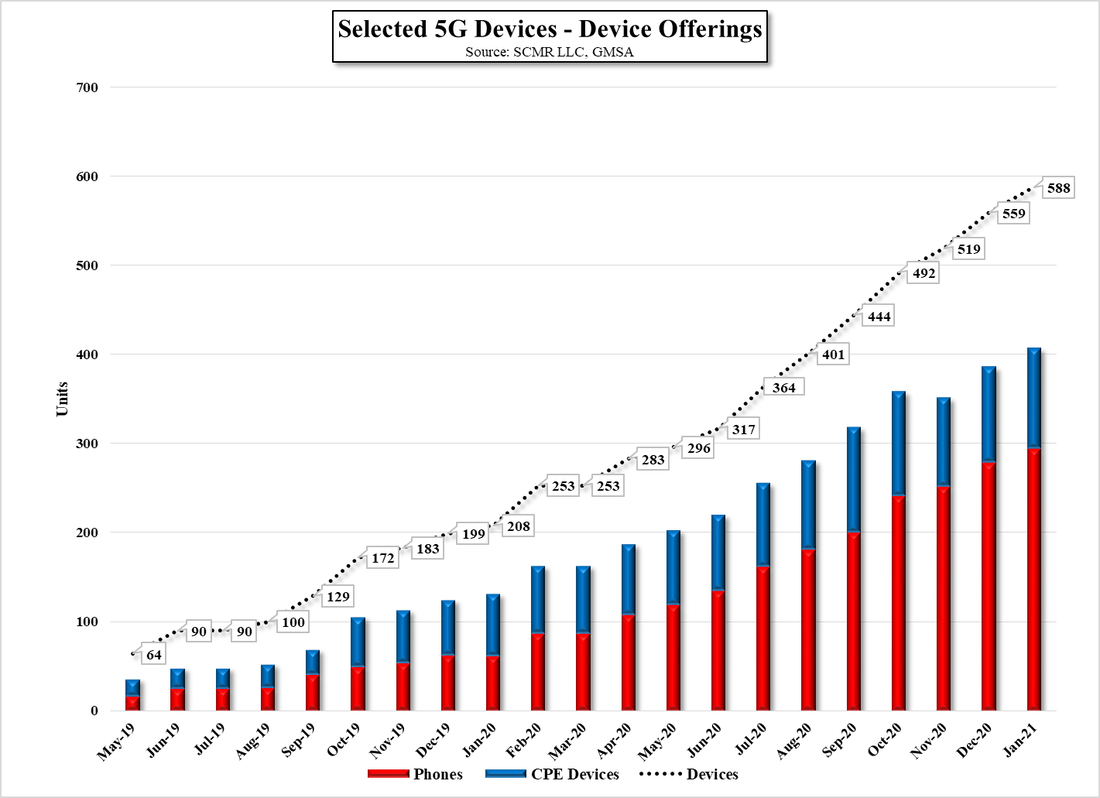

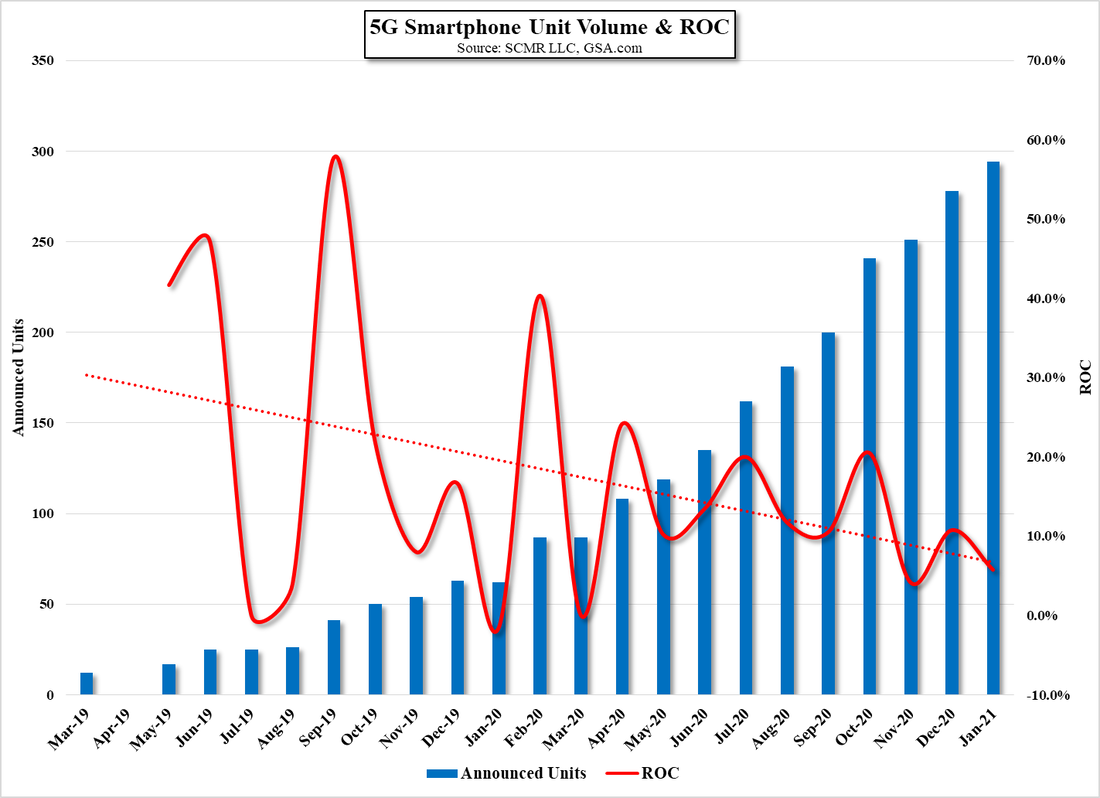

While we do not have the breakdown of new 5G devices by band yet, we do have the growth data, which we present below. The primary indicators we use to track 5G growth were all up, with vendor count up by 4.6%, device count up by 5.2%, and 5G smartphone count up by 5.8%. In particular the number of laptops with 5G availability increased from 9 in December to 11 in January against 2 in January 2020, along with a 4.6% increase in CPE (Customer Premise Equipment), which now has reached 113 models. While mobile devices are the mainstay of 5G, at least sub6 5G, FWA (Fixed Wireless Access) is where the growth in mmWave will be focused.

In order for mobile 5G to become seamless and available to a household without the problems associated with interference and building materials such as plaster lath, users should have some sort of CPE device, in the same way that optical cable has a connection device (ONT) that connects the fiber to a distribution box or internal wireless network, so the growth of CPE devices helps to understand how 5G is being used, or at least, the possibility that it can be used in other than mobile situations, even with sub6 5G. All in while we expect the ROC for 5G smartphones to continue to contract as the number of available 5G smartphones begins to approach the total number of new smartphones. In 4Q in China, approximately 50.9% of new smartphone releases were 5G smartphones, up from 42.9% in 3Q.

In order for mobile 5G to become seamless and available to a household without the problems associated with interference and building materials such as plaster lath, users should have some sort of CPE device, in the same way that optical cable has a connection device (ONT) that connects the fiber to a distribution box or internal wireless network, so the growth of CPE devices helps to understand how 5G is being used, or at least, the possibility that it can be used in other than mobile situations, even with sub6 5G. All in while we expect the ROC for 5G smartphones to continue to contract as the number of available 5G smartphones begins to approach the total number of new smartphones. In 4Q in China, approximately 50.9% of new smartphone releases were 5G smartphones, up from 42.9% in 3Q.

5G Ecosystem - Primary Indicators - Source: SCMR LLC, GSA.com

Selected 5G Devices - Device Offerings - Source: SCMR LLC, GSMA

5G Smartphone Unit Volume & ROC - Source: SCMR LLC, GSA.com

RSS Feed

RSS Feed