Samsung’s Take on AR/VR

As the 2nd largest CE company globally, Samsung Electronics has considerable influence over the direction of consumer products and CE technology, yet when in AR/VR circles, little is said about Samsung’s efforts, with much attention given to Meta (FB), who dominates the VR hardware space, and Apple, whose intentions for an Xr device in 2023 or 2024 seem to be well-known to all. Yet Samsung has been working in the shadows toward developing an AR/VR business plan, although from a slightly different angle than one would expect.

Rather than rush to market with a consumer oriented AR or VR device, Samsung is taking the path of building an AR/VR ecosystem, and working to entice software developers to work with the company, rather than flooding the market with devices and hoping that they become dominant enough to become profitable. This strategy is a bit different from Samsung’s foldable strategy, which was a race to become the first to commercialize such a technology, given a relatively open field and a well-understood smartphone market. AR/VR, especially VR, is a new market and one that has considerable issues as to its growth path. With Meta the dominant player, Samsung would be a catch-up company, having to spend vast sums to advertise that it has the ‘best’ device in the market, and no assurance that the market would accept that notion.

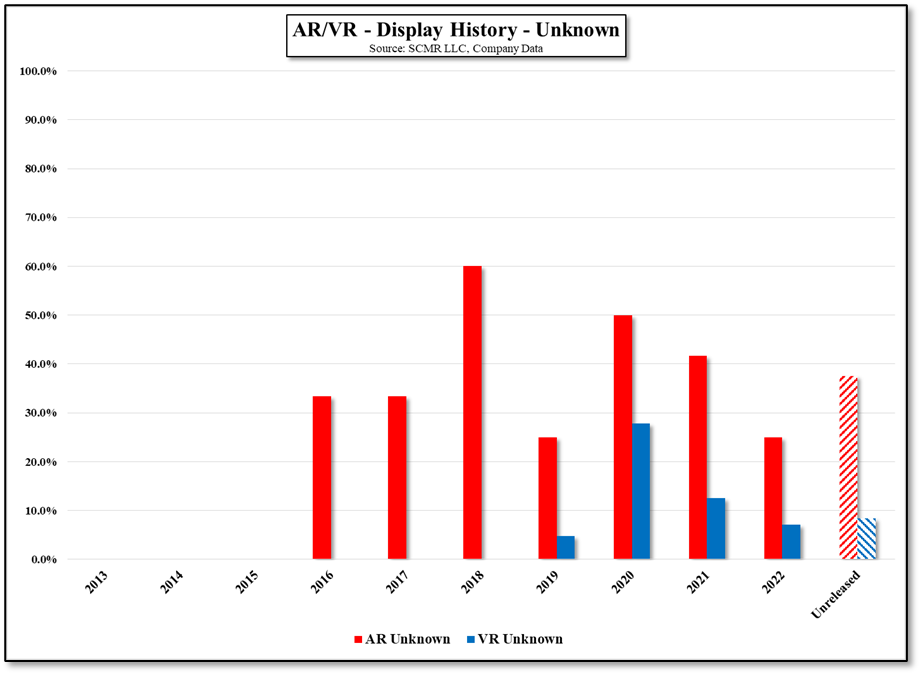

Instead, Samsung seems to be developing an ecosystem around the potential AR/VR markets, starting with a developer system assumedly next year, and aligning the direction of its affiliates and suppliers toward being able to provide as much of the potential ecosystem it would need for a high volume AR/VR production plan. But Samsung’s focus is more toward creating the content that is necessary to develop the XR market into the high volume markets that Samsung handles well, and that means it needs to coordinate content development rather than flood the market and hope that existing content attracts consumers. It is not to say that the company does not have hardware under development, with prototypes and models working through R&D, but having released a product in 2018 that saw little volume seems to have shifted Samsung’s attention away from hardware and toward software in this instance.

This is a challenge for Samsung, known for its hardware expertise, and the company faces the relatively meager adoption of its Exynos OS as a blow to its potential for building its software business, but the company does have a massive developer following given its top rankings in many DE categories, which gives them a platform from which to work. We doubt Samsung is expecting its own developers to generate such content but will incentivize the communities built around its products to build content for whatever AR/VR platform it releases. This will be similar to Apple’s AR/VR approach, where Apple knows that despite the ‘coolness’ that an Apple AR/VR device might have, if there is little to do with it, it will see strong initial sales and weak long-term growth.

Both Samsung and Apple seem to be focused more on AR than VR, with the understanding that Meta has been seeding the market for VR to gain share, while losing a considerable amount of money. W expect that neither company wants to enter into that scenario and are willing to let Meta rule the consumer market, while picking niches in both AR and VR that can carry higher ASP’s. That is where we expect both to concentrate in the first two year’s of entry into the XR market, and both have the capabilities to ‘encourage’ developers to create applications and content for their platforms, rather than pin hopes on the blossoming of the Metaverse. It is going to be a long battle for XR supremacy, but if we had to bet we would expect both companies to pursue similar paths toward such product development.

Rather than rush to market with a consumer oriented AR or VR device, Samsung is taking the path of building an AR/VR ecosystem, and working to entice software developers to work with the company, rather than flooding the market with devices and hoping that they become dominant enough to become profitable. This strategy is a bit different from Samsung’s foldable strategy, which was a race to become the first to commercialize such a technology, given a relatively open field and a well-understood smartphone market. AR/VR, especially VR, is a new market and one that has considerable issues as to its growth path. With Meta the dominant player, Samsung would be a catch-up company, having to spend vast sums to advertise that it has the ‘best’ device in the market, and no assurance that the market would accept that notion.

Instead, Samsung seems to be developing an ecosystem around the potential AR/VR markets, starting with a developer system assumedly next year, and aligning the direction of its affiliates and suppliers toward being able to provide as much of the potential ecosystem it would need for a high volume AR/VR production plan. But Samsung’s focus is more toward creating the content that is necessary to develop the XR market into the high volume markets that Samsung handles well, and that means it needs to coordinate content development rather than flood the market and hope that existing content attracts consumers. It is not to say that the company does not have hardware under development, with prototypes and models working through R&D, but having released a product in 2018 that saw little volume seems to have shifted Samsung’s attention away from hardware and toward software in this instance.

This is a challenge for Samsung, known for its hardware expertise, and the company faces the relatively meager adoption of its Exynos OS as a blow to its potential for building its software business, but the company does have a massive developer following given its top rankings in many DE categories, which gives them a platform from which to work. We doubt Samsung is expecting its own developers to generate such content but will incentivize the communities built around its products to build content for whatever AR/VR platform it releases. This will be similar to Apple’s AR/VR approach, where Apple knows that despite the ‘coolness’ that an Apple AR/VR device might have, if there is little to do with it, it will see strong initial sales and weak long-term growth.

Both Samsung and Apple seem to be focused more on AR than VR, with the understanding that Meta has been seeding the market for VR to gain share, while losing a considerable amount of money. W expect that neither company wants to enter into that scenario and are willing to let Meta rule the consumer market, while picking niches in both AR and VR that can carry higher ASP’s. That is where we expect both to concentrate in the first two year’s of entry into the XR market, and both have the capabilities to ‘encourage’ developers to create applications and content for their platforms, rather than pin hopes on the blossoming of the Metaverse. It is going to be a long battle for XR supremacy, but if we had to bet we would expect both companies to pursue similar paths toward such product development.

RSS Feed

RSS Feed