Putting Oliver Through College

The rivalry between South Korean panel producers (Samsung Display (pvt) and LG Display (LPL)) and Chinese panel producers has been ongoing for a number of years as Chinese producers have pushed South Korean producers out of the large panel LCD business. As it became obvious that Chinese producers had the advantage of significant government construction and operating subsidies, South Korean producers began shifting from LCD display production to OLED production, a relatively new technology at the time. While Chinese large panel producers eventually won the battle for LCD display domination, South Korean producers went on to establish OLED as a higher quality technology, particularly for small panel displays. Not to be outdone, Chinese panel producers have been building OLED capacity to challenge South Korean dominance in the OLED space, and while there are a multitude of CE brands that use OLED displays, the top of that list is Apple (AAPL).

Apple’s transition from LCD to OLED starting with the iPhone X, released om November 3, 2017, is expected to continue for the next few years as they migrate much of their product line to OLED. Samsung Display and LG Display have been the primary small panel OLED suppliers to Apple but are continuingly being challenged by China’s largest panel producer BOE (200725.CH), who has made some inroad with Apple, supplying replacement displays for earlier iPhones and as a 3rd supplier for some later models. While BOE has had its own issues with Apple, they continue to challenge SDC and LGD, along with a number of smaller Chinese OLED producers, and SDC has gone to the US ITC alleging patent infringement, with BOE, and other Chinese OLED producers (Chinastar (pvt), Tianma (000050.CH), and Visionox (002387.CH)) responding by challenging the validity of those patents in US Patent Court.

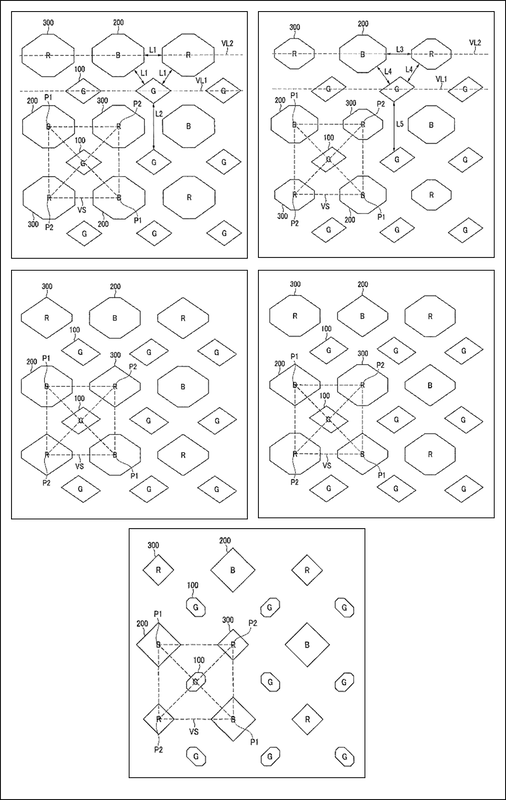

As the ITC investigation continues (target date 3/17/25) the patent challenges also continue, and the US Patent Review Board has ruled on one of the 4 patents that Samsung claims were infringed upon. The ‘683’ patent, filed by Samsung Display on 11/13/17 in the US and 3/6/12 in Korea makes 15 claims concerning OLED pixel structure, particularly Samsung’s ‘diamond’ pixel structure shown on the left side of Figure 1. The PTAB has decided that 10 of the 15 claims made in the original patent are not valid, while leaving 5 intact. Samsung will have the opportunity to appeal that decision.

Limiting the broad scope of a patent is not an unusual outcome in patent review cases, but narrowing the patent will also narrow the ITC’s investigation scope, making SDC’s case a bit harder, and could open one of the other patents included in the investigation to further scrutiny as it is essentially a continuation of the ‘683’ patent mentioned above.

All in, the validity of the ‘shape’ characteristics of the pixels (polygon, Octagon, or non-quadrilateral) as specified in the ‘683’ patent, remain in effect, which is a key point in terms of the infringement, but spacing between pixels, size, and arrangement, the other ‘683’ claims, are invalidated, reducing the points that SDC can cite in the ITC investigation. We expect SDC will appeal the PTAB decision, but this ruling and any potential appeal will likely push out the final ITC decision and the battle for OLED supremacy will continue in both the consumer space and the courts for another year. That’s how lawyers put their kids through college.

Apple’s transition from LCD to OLED starting with the iPhone X, released om November 3, 2017, is expected to continue for the next few years as they migrate much of their product line to OLED. Samsung Display and LG Display have been the primary small panel OLED suppliers to Apple but are continuingly being challenged by China’s largest panel producer BOE (200725.CH), who has made some inroad with Apple, supplying replacement displays for earlier iPhones and as a 3rd supplier for some later models. While BOE has had its own issues with Apple, they continue to challenge SDC and LGD, along with a number of smaller Chinese OLED producers, and SDC has gone to the US ITC alleging patent infringement, with BOE, and other Chinese OLED producers (Chinastar (pvt), Tianma (000050.CH), and Visionox (002387.CH)) responding by challenging the validity of those patents in US Patent Court.

As the ITC investigation continues (target date 3/17/25) the patent challenges also continue, and the US Patent Review Board has ruled on one of the 4 patents that Samsung claims were infringed upon. The ‘683’ patent, filed by Samsung Display on 11/13/17 in the US and 3/6/12 in Korea makes 15 claims concerning OLED pixel structure, particularly Samsung’s ‘diamond’ pixel structure shown on the left side of Figure 1. The PTAB has decided that 10 of the 15 claims made in the original patent are not valid, while leaving 5 intact. Samsung will have the opportunity to appeal that decision.

Limiting the broad scope of a patent is not an unusual outcome in patent review cases, but narrowing the patent will also narrow the ITC’s investigation scope, making SDC’s case a bit harder, and could open one of the other patents included in the investigation to further scrutiny as it is essentially a continuation of the ‘683’ patent mentioned above.

All in, the validity of the ‘shape’ characteristics of the pixels (polygon, Octagon, or non-quadrilateral) as specified in the ‘683’ patent, remain in effect, which is a key point in terms of the infringement, but spacing between pixels, size, and arrangement, the other ‘683’ claims, are invalidated, reducing the points that SDC can cite in the ITC investigation. We expect SDC will appeal the PTAB decision, but this ruling and any potential appeal will likely push out the final ITC decision and the battle for OLED supremacy will continue in both the consumer space and the courts for another year. That’s how lawyers put their kids through college.

[Note: The US Patent Office considers a patent unpatentable when the difference between claimed subject matter and prior art would have been obvious at the time of invention by a person having ordinary skill in the art to which subject matter pertains, where ‘ordinary skill’ means a degree in electrical engineering, material science, physics, or similar disciplines, along with 2 years of professional experience working with display design, including OLED displays or an equivalent level of skill, knowledge, or experience.]

Figure 1 - Diamond Pixel Pattern & BOE Comparison - Source: USPO

Figure 2 - '683' Patent - Pixel shapes, sizes, & configurations - Source: SCMR LLC, USPO

RSS Feed

RSS Feed