August Display Company Recap

Large panel shipments (Fig. 4) were up 0.1% in August while large panel sales (Fig. 5) were down 3.8%, a result of the large drop in TV panel prices (-10.1%). With July being the peak for TV panel prices and IT product panel pricing remaining stable in August (looks the same in September), but the effects of the steep TV panel price drop in August had a negative effect on LCD panel industry sales, with the price per unit of TV panels considerably greater than that of IT panels. We show both Shipments & Share in Fig. 6. To illustrate how shipments have remained flat but large panel price increases have kept sales momentum intact. Given the Significant drop in TV panel prices in August and again in September, we expect the September large panel sales results to see another drop.

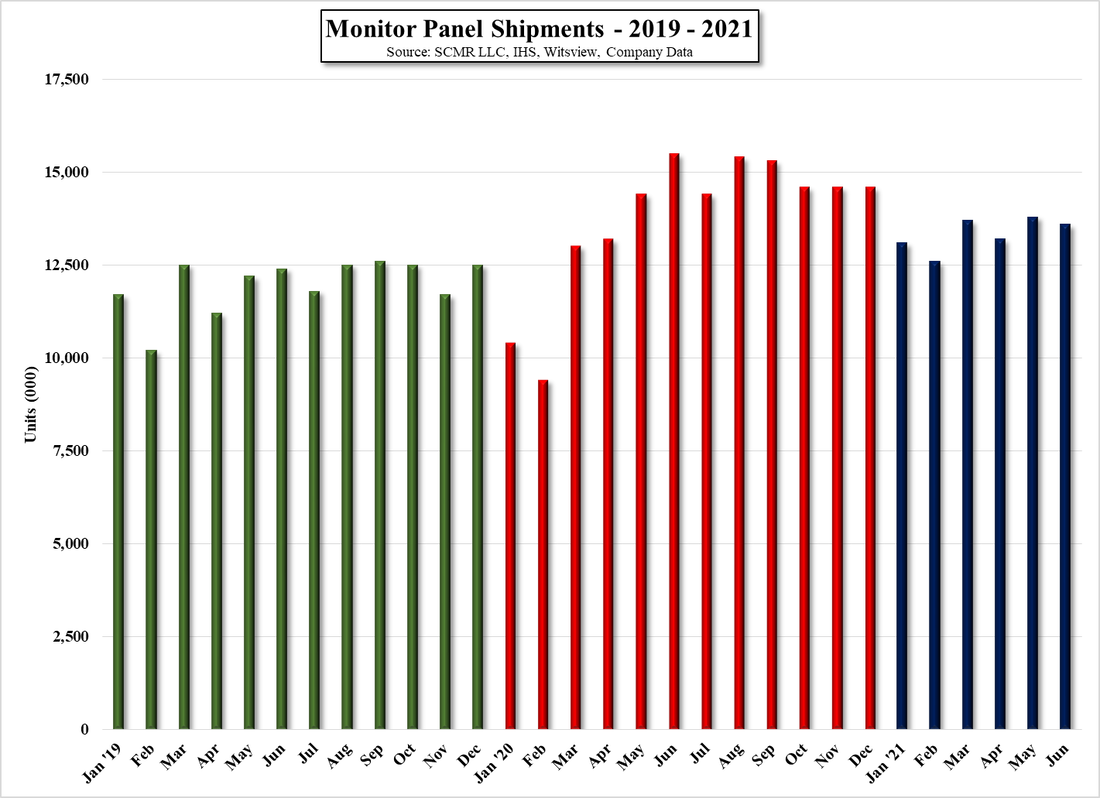

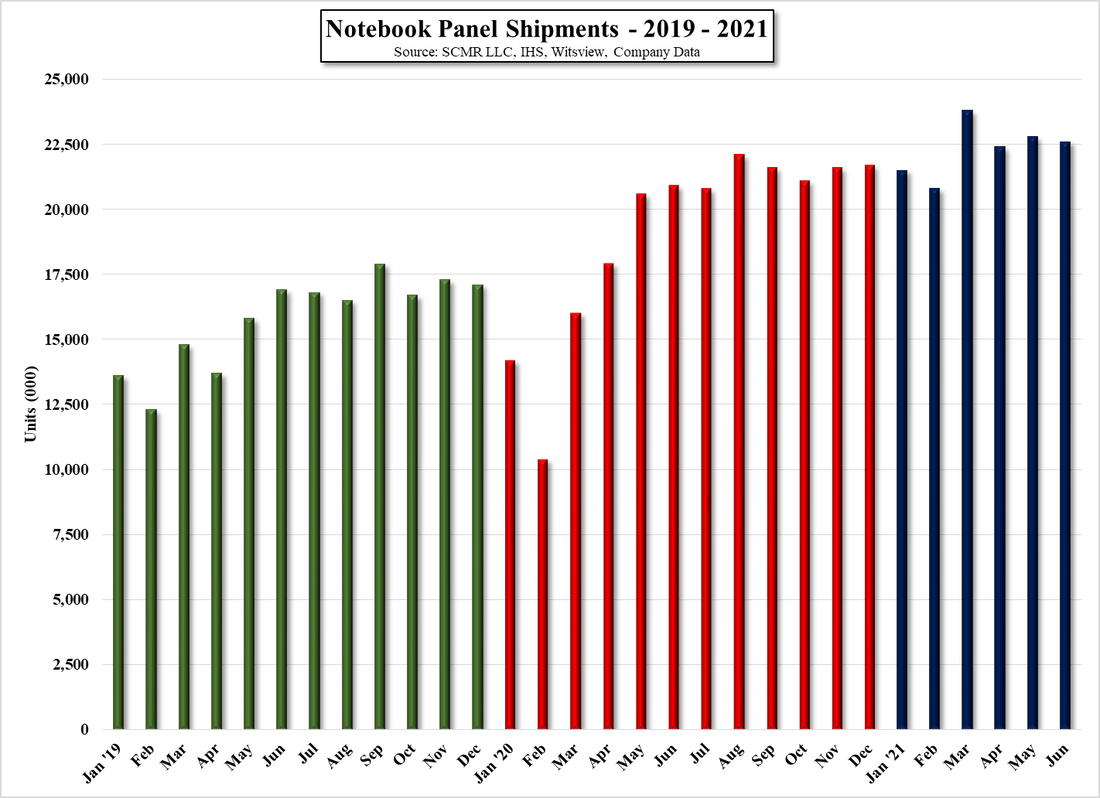

TV panel share is a monthly variable that does not get reported by many panel producers (some do quarterly) but based on our data, we believe the shipment level for LCD TV panels declined by 4.3% in August, following a 1.5% increase in July, offset by a 2.8% increase in monitor shipments, flat notebook shipments, and a 4.8% increase in tablet shipments. The shipment trends are noted in Fig. 7. Panel producers have been decreasing their share of TV panel production in lieu of IT panel products, less in anticipation of the price drop seen in August but more due to the continued demand for notebooks and monitors. While there is much talk over how this will lessen the effect on panel producer sales as TV panel prices decline, we have only seen one month of excessive TV panel price declines and therefore little cumulative negative momentum. Given that September saw an even larger decline in LCD TV panel prices and little price offset from IT panel pricing, we expect that September industry large panel sales will be down in excess of 5%.

TV panel share is a monthly variable that does not get reported by many panel producers (some do quarterly) but based on our data, we believe the shipment level for LCD TV panels declined by 4.3% in August, following a 1.5% increase in July, offset by a 2.8% increase in monitor shipments, flat notebook shipments, and a 4.8% increase in tablet shipments. The shipment trends are noted in Fig. 7. Panel producers have been decreasing their share of TV panel production in lieu of IT panel products, less in anticipation of the price drop seen in August but more due to the continued demand for notebooks and monitors. While there is much talk over how this will lessen the effect on panel producer sales as TV panel prices decline, we have only seen one month of excessive TV panel price declines and therefore little cumulative negative momentum. Given that September saw an even larger decline in LCD TV panel prices and little price offset from IT panel pricing, we expect that September industry large panel sales will be down in excess of 5%.

Large Panel Display Shipments - 2019 - 2021 YTD - Source: SCMR LLC, OMDIA, Company Data

Large Panel Display Sales & ROC - 2019 - 2021 YTD - Source: SCMR LLC, OMDIA, Company Data

Large Panel Display Shipments & Sales - 2019 - 2021 YTD - Source: SCMR LLC, OMDIA, Company Data

Large Panel Shipments - By Type - Source: SCMR LLC, OMDIA, Company Data

Translating those metrics to companies, we first look at the sales share of the top 5 large panel producers to gain insight into who might be affected most by declining large panel prices. As noted, the concentration is quite high with 83.1% of the industry’s large panel LCD sales coming from the top 5 producers. That said, given that August was the first month where TV panel prices dropped substantially, we look at the sequential change in sales for large panel producers between July and August to see who was affected most by the TV panel price drop. We note that ideally we would like to see at least one additional month of data that included substantial panel price drops, but we take what we can get until next month’s data becomes available. We note that we have added share in the second table to gain better understanding as to how much each panel producer influenced the total.

We note that Samsung Display has sold or closed much of its large panel LCD capacity, so monthly results could reflect that limited capacity (hence the 1.4% share) and the impact of large panel price declines. LG Display, to a lesser degree, has done the same.

All in, August looks to be the tip of the iceberg for large panel LCD producers in terms of the impact of decreasing TV panel prices. If September and October are any indication of the severity of such panel price drops, the effects will be felt by almost all large panel producers, especially if there is little positive offset from IT panel pricing or shipments. Given that it took only a short period for TV panel prices to trace back almost half of the gains made in the last year, it sets the stage for a weak 4th quarter for large panel producers. As noted above, we expect IT panel pricing to remain reasonably stable for the remainder of the year, and would find it difficult to assume that TV panel prices continue to fall at such a precipitous rate for the rest of the year, but we did not expect to see an almost 20% drop in TV panel prices in September. “Surprise, Surprise” – Gomer Pyle USMC (1964).

All in, August looks to be the tip of the iceberg for large panel LCD producers in terms of the impact of decreasing TV panel prices. If September and October are any indication of the severity of such panel price drops, the effects will be felt by almost all large panel producers, especially if there is little positive offset from IT panel pricing or shipments. Given that it took only a short period for TV panel prices to trace back almost half of the gains made in the last year, it sets the stage for a weak 4th quarter for large panel producers. As noted above, we expect IT panel pricing to remain reasonably stable for the remainder of the year, and would find it difficult to assume that TV panel prices continue to fall at such a precipitous rate for the rest of the year, but we did not expect to see an almost 20% drop in TV panel prices in September. “Surprise, Surprise” – Gomer Pyle USMC (1964).

RSS Feed

RSS Feed