China Smartphone Shipments – January & 2022 Forecast

In January China shipped 33.02m mobile phones, down 1.1% m/m and down 17.7% y/y, with domestic brands making up 25.65m units, or 77.7% and smartphones making up 98.0% of the total, a share consistent with much of 2021. 26.3m of the mobile total were 5G phones, for a 79.6% share of the total, and 30 new models were released into the domestic Chinese market of which 50% were 5G. Mobile phone Shipments in China have returned to pre-COVID-19 levels for the last four months and we expect a continuation of that trend for much of this year, seasonality aside.

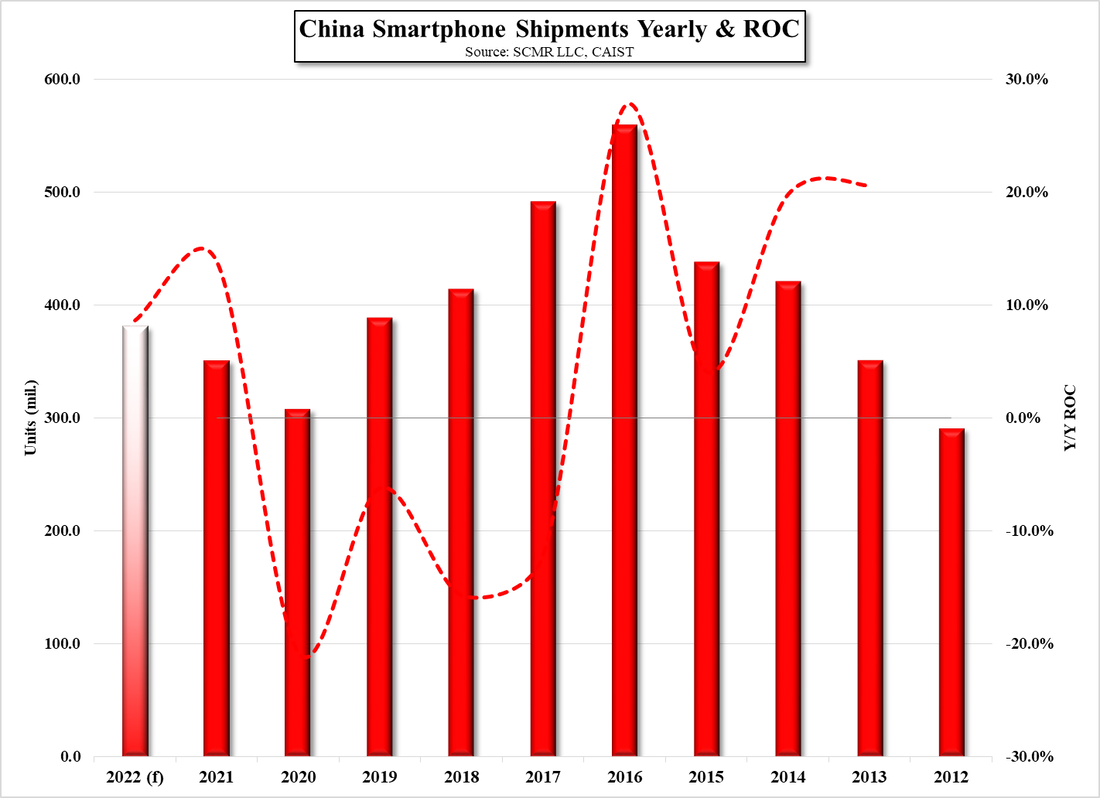

We expect the most significant mitigating factor will be component shortages that could limit shipments or push back model release dates, which leads us to forecast full year mobile phone shipments in China to be 381.24m units, up a relatively conservative 8.7% y/y. We expect 5G phones to continue to grow share, reaching an average of 80.7% for the year, which would imply shipments of 307.67m 5G units this year, unit growth of 15.6% over 2021’s 266.2m 5G shipments on the Mainland. While we expect there could be considerable play in all of our shipment estimates for China, we expect that on an overall basis 2022 will be a less volatile year than the last two.

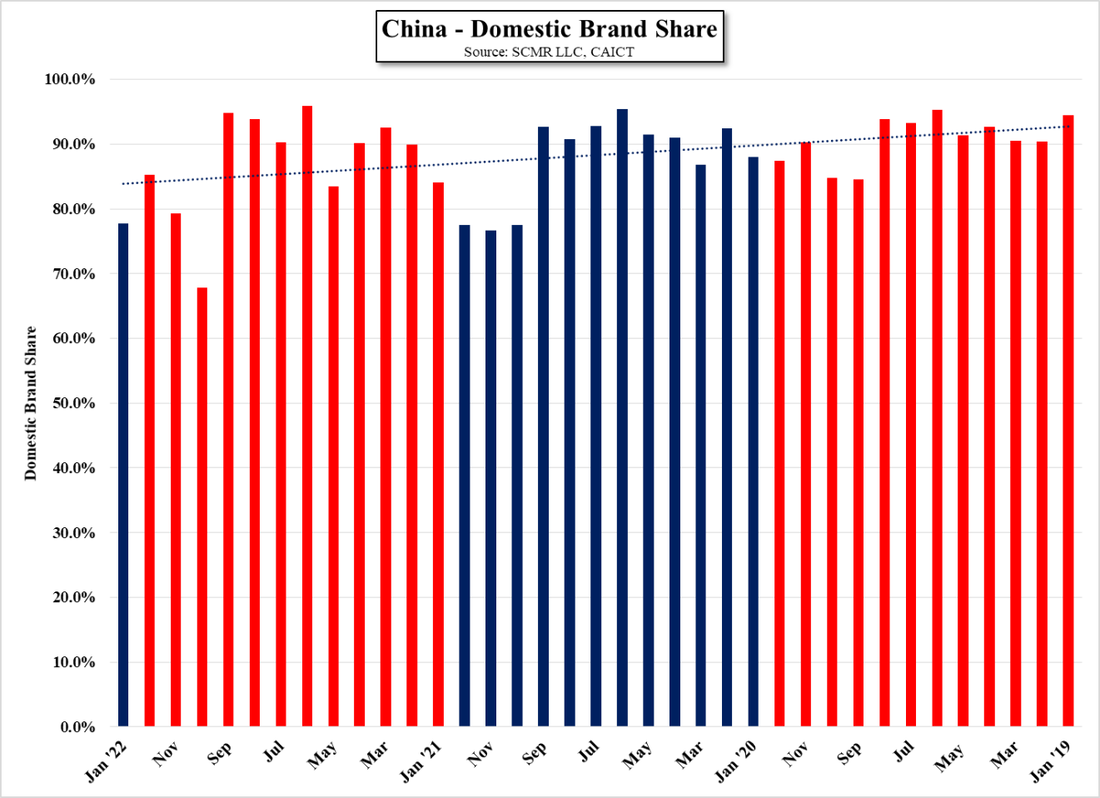

We have noticed a trend that seems to be maintaining itself over the last few years and that is a decline in the share of the Chinese market by domestic brands as seen in Figure 6, which has declined (trendline) since 2019. That said, there have been some monthly domestic brand share increases that have made such data look less valid, such as the peak in June ’21 of 95.9% domestic brand share, but we expect much of that has to do with the timing of domestic brand releases versus foreign brand release schedules. Chinese brands certainly have the largest share of the domestic market, but the impact of trade sanctions against former share leader Huawei (pvt) by the US has reduced their share both globally and in China, and while domestic brands have picked up much of that slack, it has opened the door a bit wider for foreign brands such as Apple (AAPL) and Samsung (005930.KS).

We expect the most significant mitigating factor will be component shortages that could limit shipments or push back model release dates, which leads us to forecast full year mobile phone shipments in China to be 381.24m units, up a relatively conservative 8.7% y/y. We expect 5G phones to continue to grow share, reaching an average of 80.7% for the year, which would imply shipments of 307.67m 5G units this year, unit growth of 15.6% over 2021’s 266.2m 5G shipments on the Mainland. While we expect there could be considerable play in all of our shipment estimates for China, we expect that on an overall basis 2022 will be a less volatile year than the last two.

We have noticed a trend that seems to be maintaining itself over the last few years and that is a decline in the share of the Chinese market by domestic brands as seen in Figure 6, which has declined (trendline) since 2019. That said, there have been some monthly domestic brand share increases that have made such data look less valid, such as the peak in June ’21 of 95.9% domestic brand share, but we expect much of that has to do with the timing of domestic brand releases versus foreign brand release schedules. Chinese brands certainly have the largest share of the domestic market, but the impact of trade sanctions against former share leader Huawei (pvt) by the US has reduced their share both globally and in China, and while domestic brands have picked up much of that slack, it has opened the door a bit wider for foreign brands such as Apple (AAPL) and Samsung (005930.KS).

- China Smartphone Shipments % Y/Y ROC - 2019 - 2022 YTD - Source: SCMR LLC, CAIST

China 5G Smartphone Shipments & Share - Source: SCMR LLC, CAIST

China - 5G Smartphones - Share - Total Shipped & New Models - Source: SCMR LLC, CAIST

China Smartphone Shipment Share By Technology - Source: SCMR LLC, CAIST

China Smartphone Shipments Yearly & ROC - Source: SCMR LLC, CAIST

China - Domestic Brand Share - Source: SCMR LLC, CAIST

RSS Feed

RSS Feed