Display Industry Summary – June

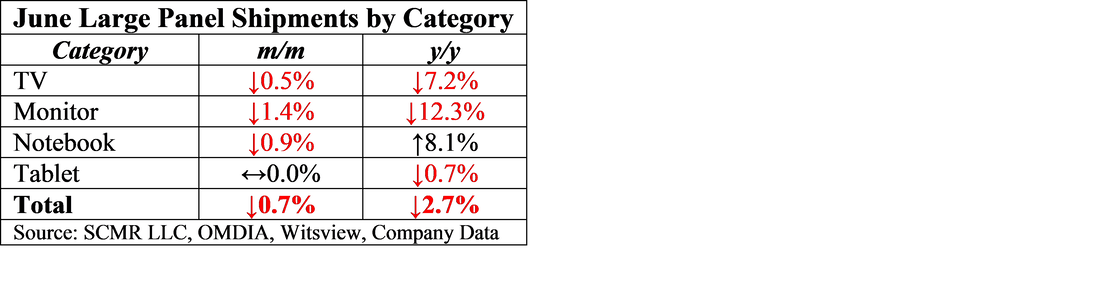

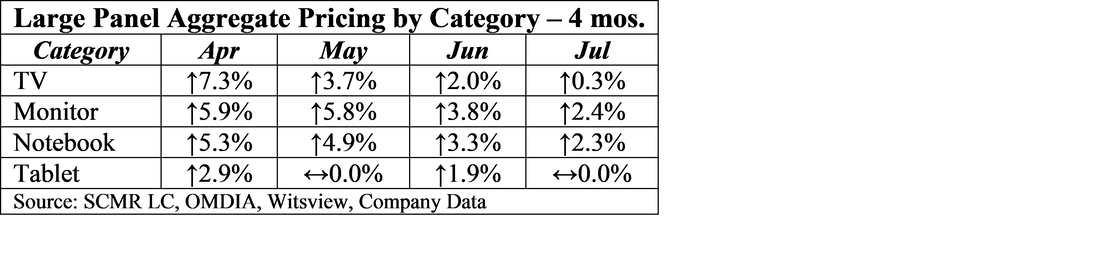

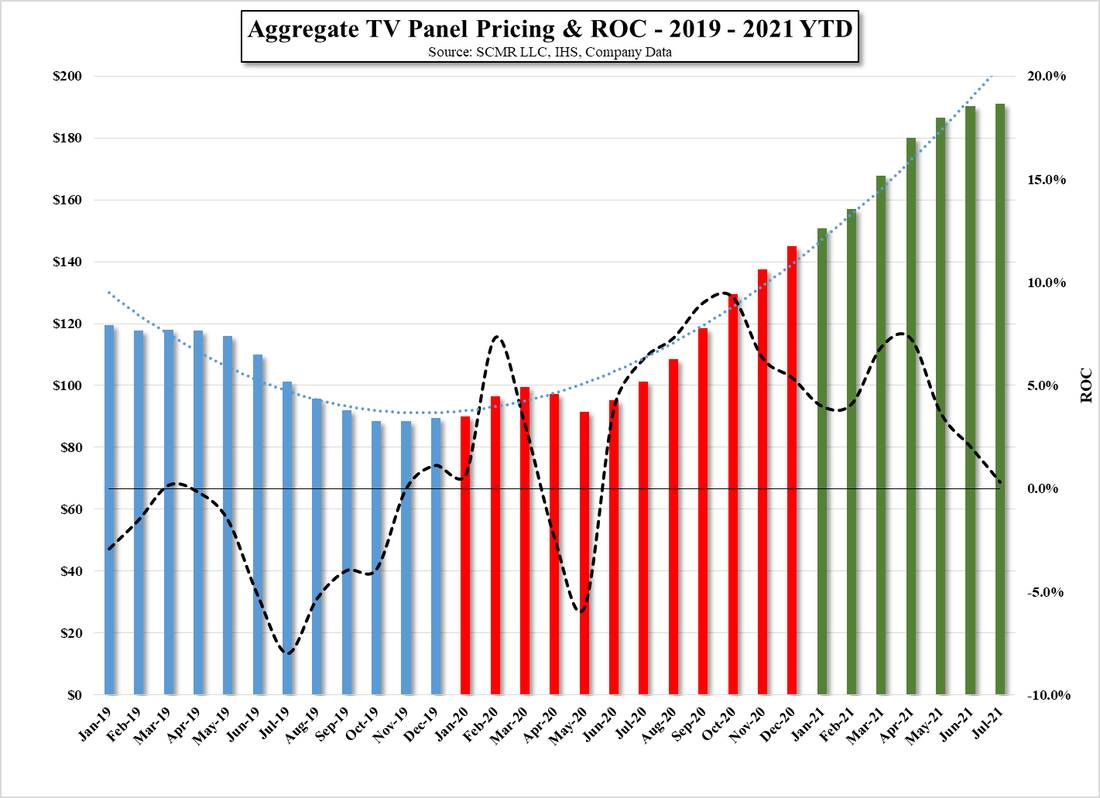

There was one statistic that stood out in June concerning the large panel display market. June was the first month that saw negative y/y large panel shipment comparisons since March of 2020, 15 months ago. While this is not something unexpected, as we have noted the potential for this occurrence a number of times, we had been expecting such comparisons to go negative first in July. June display industry sales came in at $7.47t US, 3.25% lower than our expectation but still up 42.6% y/y, and while large panel ASP’s have been rising since last May, June was the first month where they saw a decline, albeit a small one, down 0.1% with the average large panel ASP monthly increase being 3.6% this year and 3.2% over the last 12 months.

We expect panel producers will pass off the shipment and ASP issues as a function of component shortages which have limited shipments, but while we believe there are certainly component shortages that are limiting panel shipments, it is very difficult to discern whether a change in demand has also affected both industry characteristics in June. As we noted above, we would have expected slower shipments in July, but not a lower ASP as we had expected overall panel prices to continue to rise, albeit at a slower rate than in the past year.

We expect panel producers will pass off the shipment and ASP issues as a function of component shortages which have limited shipments, but while we believe there are certainly component shortages that are limiting panel shipments, it is very difficult to discern whether a change in demand has also affected both industry characteristics in June. As we noted above, we would have expected slower shipments in July, but not a lower ASP as we had expected overall panel prices to continue to rise, albeit at a slower rate than in the past year.

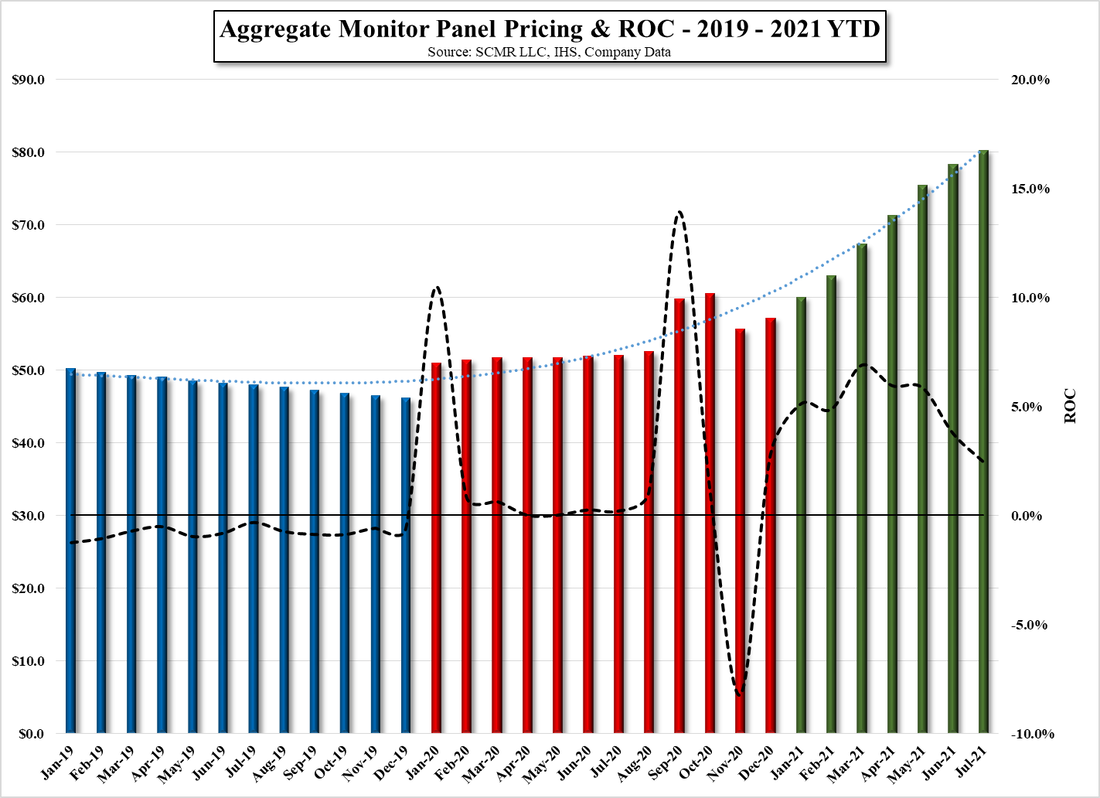

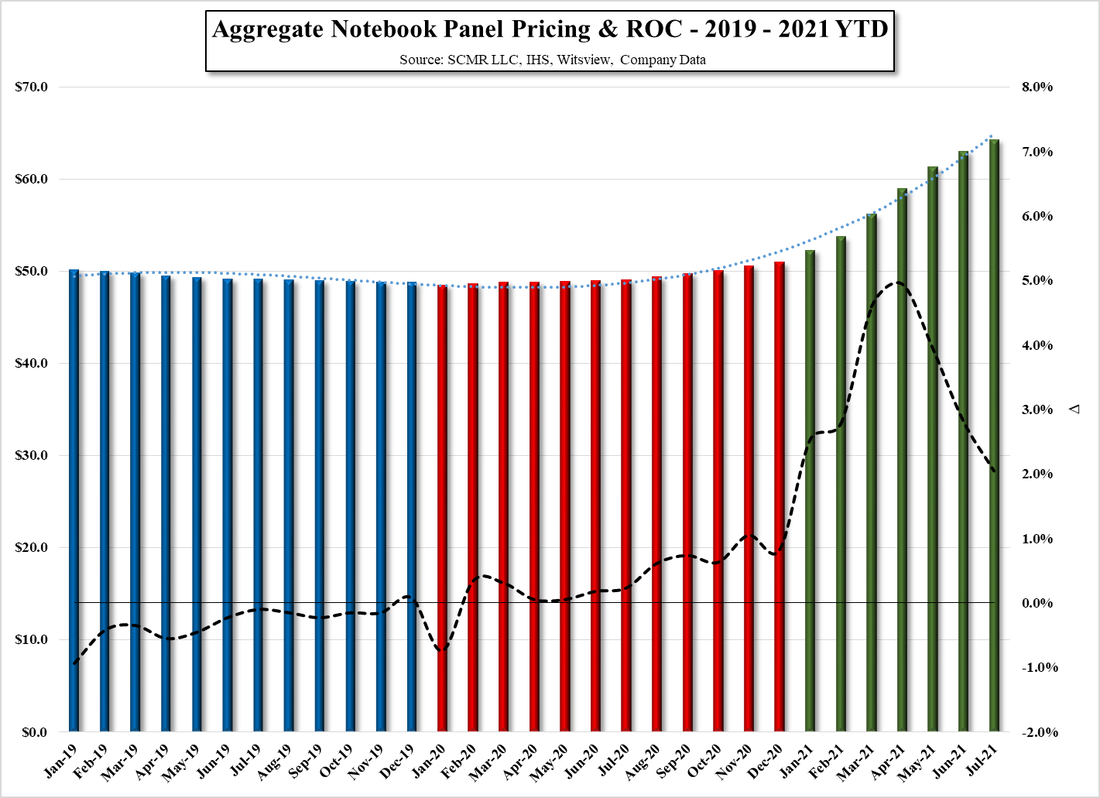

Panel prices rose in June, as we previously noted, but are expected to see more modest increases this month, as indicated below, with TV prices almost flat. We expect large panel shipments to be flat to down in July, which will put additional pressure on panel producer results, particularly TV panels. While there could be an improvement in shipments in August as back-to-school inventory buys might be needed, both component shortages and seasonally slow summer sales will likely keep the potential increase to a minimum. That said, we do expect modest price increases for notebooks and monitors, in August but not for TVs, which would keep large panel display sales flat for many panel producers.

In June many large panel producers saw negative m/m sales growth, with AU Optronics (AUOTY) in Taiwan, and Chinastar (pvt), HKC (0248.HK), and CHOT (pvt) in China, the exceptions. The purchase of Samsung’s (005930.KS) Suzhou LCD fab is helping Chinastar’s sales, and both HKC and CHOT are expanding capacity, however BOE (200725.CH), China’s largest LCD panel producer saw negative m/m growth in sales, similar to South Korean and Taiwan large panel producers, and we would expect those trends to continue into this month. We exclude those panel producers that are primarily small panel focused.

In June many large panel producers saw negative m/m sales growth, with AU Optronics (AUOTY) in Taiwan, and Chinastar (pvt), HKC (0248.HK), and CHOT (pvt) in China, the exceptions. The purchase of Samsung’s (005930.KS) Suzhou LCD fab is helping Chinastar’s sales, and both HKC and CHOT are expanding capacity, however BOE (200725.CH), China’s largest LCD panel producer saw negative m/m growth in sales, similar to South Korean and Taiwan large panel producers, and we would expect those trends to continue into this month. We exclude those panel producers that are primarily small panel focused.

Large Panel Display Shipments - 2019 - 2021 YTD - Source: SCMR LLC, OMDIA, Company Data

Large Panel Display Sales - 2019 - 2021 YTD - Source: SCMR LLC, OMDIA, Company Data

Large Panel ASP - 2019 - 2021 YTD - Source: SCMR LLC, OMDIA, Company Data

TV Panel Shipments - 2019 - 2021 YTD - Source: Source: SCMR LLC, IHS, Witsview, Company Data

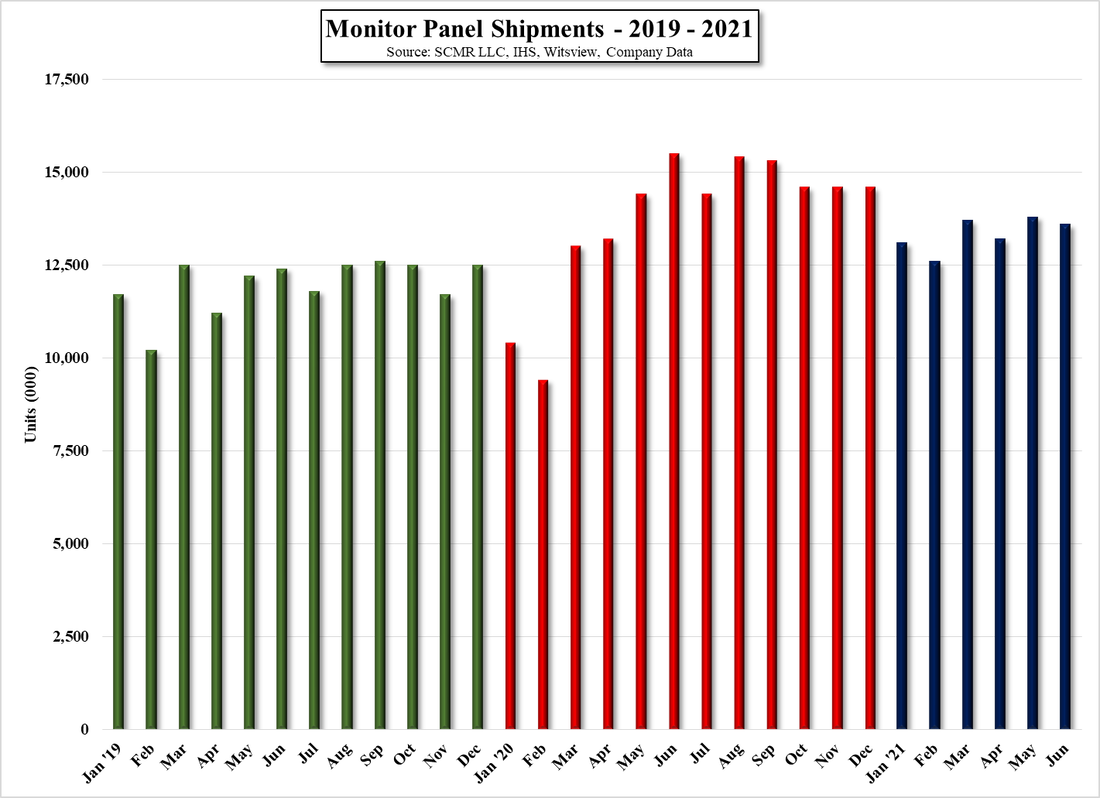

Monitor Panel Shipments - 2019 - 2021 YTD - Source: Source: SCMR LLC, IHS, Witsview, Company Data

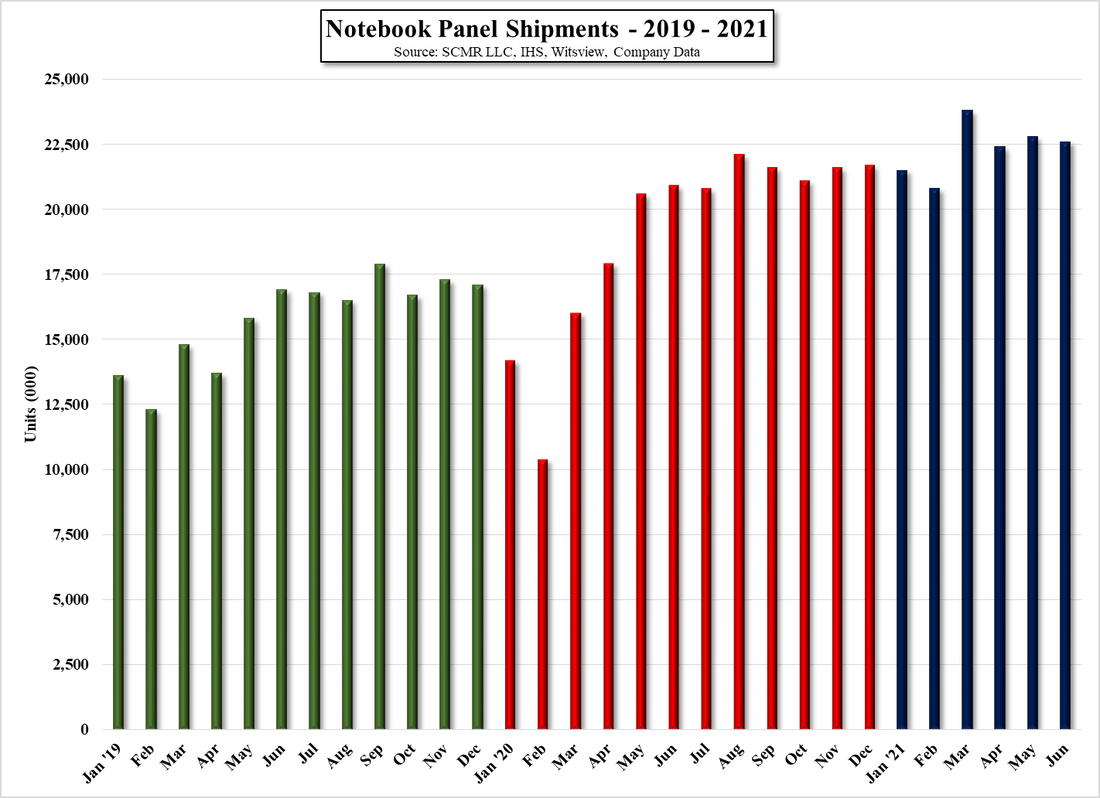

Notebook Panel Shipments - 2019 - 2021 YTD - Source: Source: SCMR LLC, IHS, Witsview, Company Data

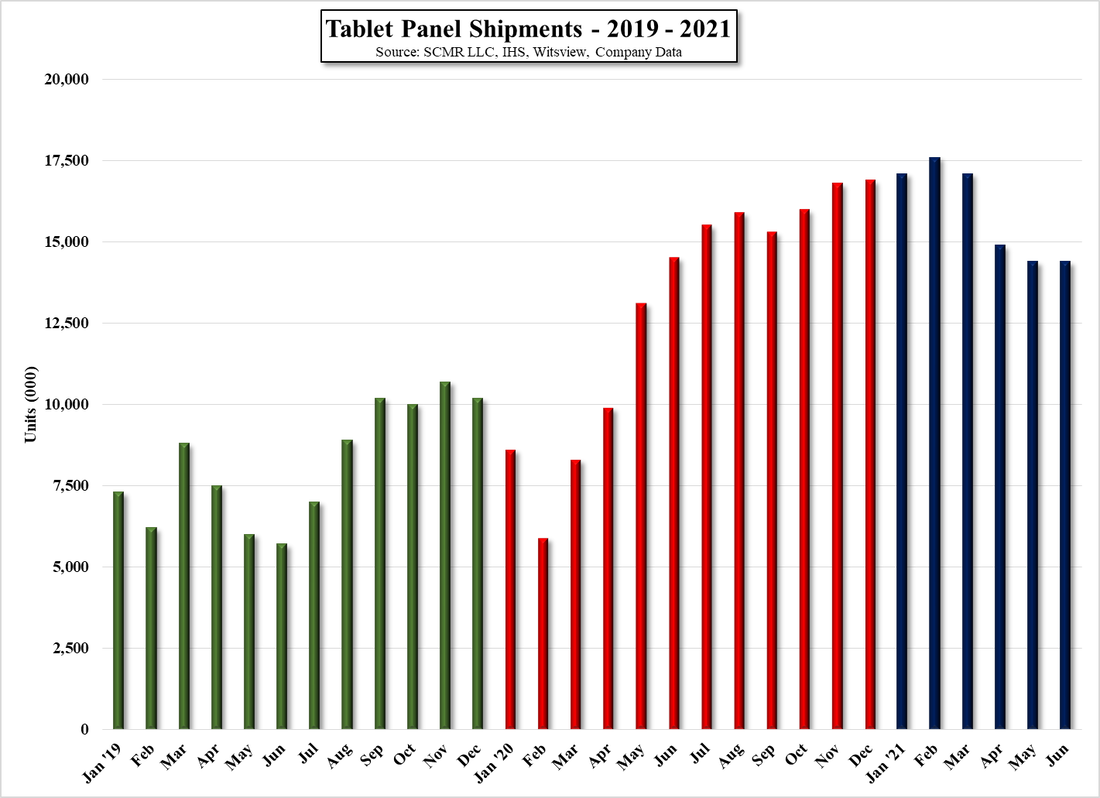

Tablet Shipments - 2019 - 2021 YTD - Source: SCMR LLC, IHS, Witsview, Company Data

Aggregate TV PAnel Pricing & ROC - 2019 - 2021 YTD - Source: SCMR LLC, IHS, Company Data

Aggregate Monitor Panel Pricing & ROC - 2019 - 2021 YTD - Source: SCMR LLC, IHS, Company Data

Aggregate Notebook Panel Pricing &ROC - 2019 - 2021 YTD - Source: SCMR LLC, IHS, Company Data

RSS Feed

RSS Feed