Chinese markets seem to be taking a breather

While we have not heard direct confirmation that an across-the-board slowdown in the Chinese CE market is in progress, we have heard from a number of vendors that both smartphone and TV inventories remain high after the Chinese New Year holiday, and levels will be worked down during 1Q. We note that 1Q is typically the slowest quarter in the display business, with holidays reducing factory production days and holiday goods already on retail shelves, but we have also heard little from panel producers about lower utilization levels expected for 1Q. This is an unusual situation in that while unit volumes are expected to be flat to moderately down, most panel producers are citing expectations for no change in factory utilization rates.

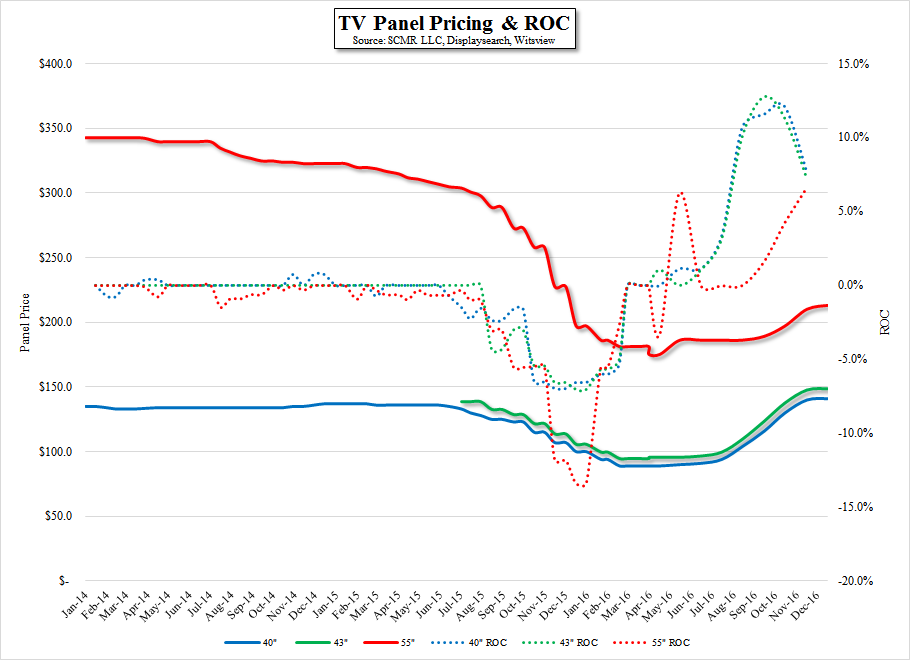

Further, in situations where inventories are above average seasonally adjusted levels, panel pricing has a tendency to decline, which has only modestly been the case most recently. We continue to focus on a number of patterns, particularly 32” TV panels, which are essentially an entry level size for emerging markets, and 55” TV panels, which have become standard to the majority of worldwide TV buyers. Neither category has seen any real price deterioration and those panel sizes (40” – 45”) that have been in short supply due to Samsung Display (pvt) issues, continue to increase in price, albeit at lower monthly increases than seen in 3Q.

So the question is, who do you believe? Panel producers, who have a vested interest in continuing the price increases that have put them back into profitability, anecdotal inventory reads, TV brands, who are for the most part are setting higher shipment goals for 2017 than in the previous year, despite lackluster TV growth, or Chinese smartphone vendors, who expect to see sales from inventory during the 1st quarter? We always go with pricing, which is why we track it on a monthly basis, but when all of the signs are pointing in different directions we become suspicious, as we are currently. At a gut level if feels like everyone is saying what they hope rather than what they expect, which usually leads to a disappointment. Maybe our gut is wrong, but the stars do not seem to align in this situation, at least for the time being.

Further, in situations where inventories are above average seasonally adjusted levels, panel pricing has a tendency to decline, which has only modestly been the case most recently. We continue to focus on a number of patterns, particularly 32” TV panels, which are essentially an entry level size for emerging markets, and 55” TV panels, which have become standard to the majority of worldwide TV buyers. Neither category has seen any real price deterioration and those panel sizes (40” – 45”) that have been in short supply due to Samsung Display (pvt) issues, continue to increase in price, albeit at lower monthly increases than seen in 3Q.

So the question is, who do you believe? Panel producers, who have a vested interest in continuing the price increases that have put them back into profitability, anecdotal inventory reads, TV brands, who are for the most part are setting higher shipment goals for 2017 than in the previous year, despite lackluster TV growth, or Chinese smartphone vendors, who expect to see sales from inventory during the 1st quarter? We always go with pricing, which is why we track it on a monthly basis, but when all of the signs are pointing in different directions we become suspicious, as we are currently. At a gut level if feels like everyone is saying what they hope rather than what they expect, which usually leads to a disappointment. Maybe our gut is wrong, but the stars do not seem to align in this situation, at least for the time being.

Figure 3 - TV panel pricing - through January 2017 - Source: SCMR LLC, Displaysearch, Witsview

RSS Feed

RSS Feed