Folds

There has been much said this year about foldable smartphones, particularly recently as Samsung is expected to announce at least two new foldables at an event next month, and at lower prices than the previous models (see our note from yesterday. While Samsung is certainly the leader with the largest number of foldable devices, there are expected to be a number of new players entering the foldable smartphone market this year, although dates are still tentative for most and we expect at least one to fall into 2022.

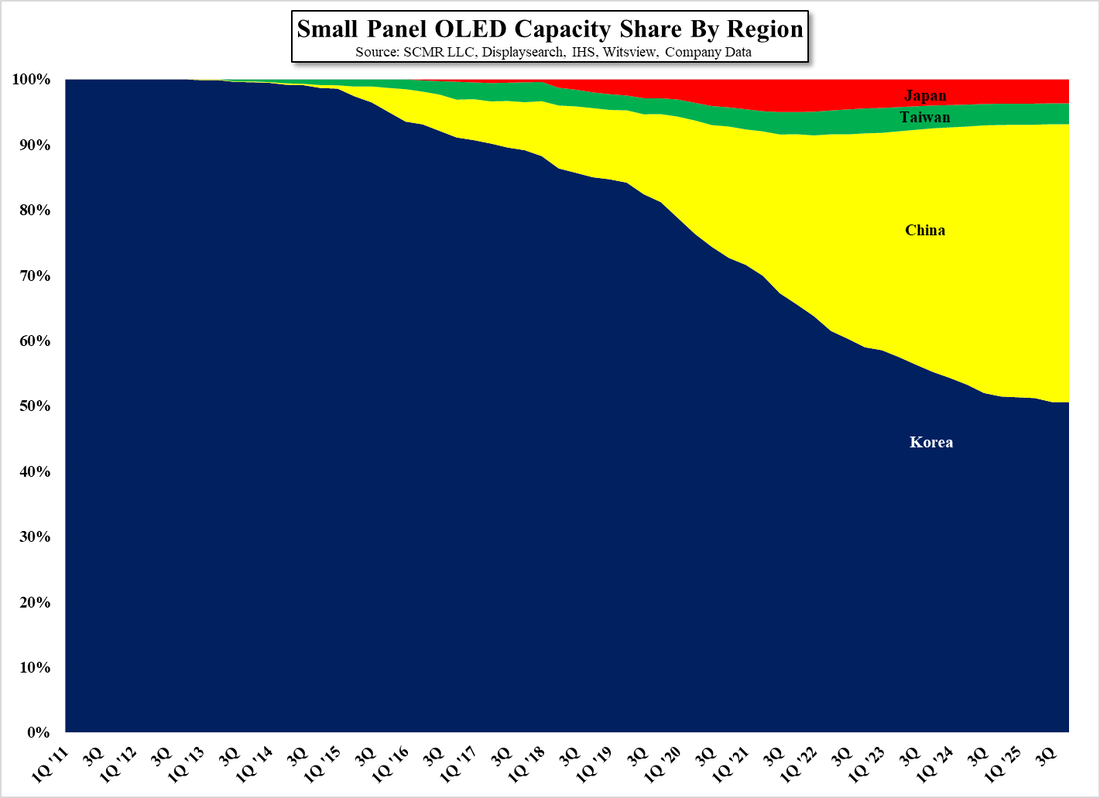

While the supply chain for foldables is similar to that of flexible or rigid display smartphones, it is still developing, with OLED display suppliers vying for representation, hinge suppliers developing new systems to help reduce folding stress, and cover material suppliers looking for better display protection without sacrificing bendability. Samsung Display is the leader in foldable display production, supplying parent Samsung Electronics with all of its foldable displays, but China’s BOE (200725.CH) and Chinastar (pvt) continue to challenge SDC’s domination of the foldable display space.

That said, each new model opens a new round of competition between the players and there is no guarantee that the same display supplier will maintain its place as new models appear. Further, the challenges facing other component suppliers, particularly cover materials, also continues, with a growing desire to move from polyimide film to glass. Glass for foldables needs to be extremely thin, below 60um (0.00236”, 0.001mm, or the thickness of very thin magazine paper) in order to bend without breaking, and must be shatter-resistant at the least, as polyimide film has lower bend radius limitations but is not 100% optically clear and can crease if bent too many times.

Chinese foldable smartphone brands have been using polyimide as had Samsung until recently when it switched from polyimide, supplied by Sumitomo Chemical (4005.JP) to UTG (Ultra-thin glass) produced by Schott (AFX.GR) and thinned by Dowoo Insys (pvt) a small firm in Korea. Samsung has also been working with long-time cover glass supplier Corning (GLW) to develop UTG and is expected to use Corning’s UTG on the upcoming Galaxy Z Fold3 to be announced next month. What complicates this situation is that the new Galaxy Z Fold 3 is expected to have pen capabilities which both increases the thickness of the display and increases the need to protect the display from pen pressure. With Corning’s UTG at 50um and Schott’s at 30um the thinner UTG represents a way for Samsung to keep display thickness under control but provides less protection from the stylus pressure, which is likely to give Corning the edge for the Galaxy Fold3, while Schott will continue to provide UTG for the Galaxy Flip 3. That said, Corning is said to be working with its own Korean glass processor, eCONY (pvt) in terms of cutting while Samsung is said to be looking for a local processor to thin Corning’s UTG further.

As Chinese brands roll out additional or first-time foldables later this year, they are expected to also make the shift to UTG, but it is unclear who they will choose as a cover glass supplier. Corning is the exclusive supplier of large panel substrate glass to BOE so they have a solid relationship already existing, giving them a strong negotiating position, but the necessity for a thicker UTG is not an issue for most other foldable brand, so there will be a model by model battle for each of the new devices between current suppliers. The table below shows existing and new models expected for this year.

While the supply chain for foldables is similar to that of flexible or rigid display smartphones, it is still developing, with OLED display suppliers vying for representation, hinge suppliers developing new systems to help reduce folding stress, and cover material suppliers looking for better display protection without sacrificing bendability. Samsung Display is the leader in foldable display production, supplying parent Samsung Electronics with all of its foldable displays, but China’s BOE (200725.CH) and Chinastar (pvt) continue to challenge SDC’s domination of the foldable display space.

That said, each new model opens a new round of competition between the players and there is no guarantee that the same display supplier will maintain its place as new models appear. Further, the challenges facing other component suppliers, particularly cover materials, also continues, with a growing desire to move from polyimide film to glass. Glass for foldables needs to be extremely thin, below 60um (0.00236”, 0.001mm, or the thickness of very thin magazine paper) in order to bend without breaking, and must be shatter-resistant at the least, as polyimide film has lower bend radius limitations but is not 100% optically clear and can crease if bent too many times.

Chinese foldable smartphone brands have been using polyimide as had Samsung until recently when it switched from polyimide, supplied by Sumitomo Chemical (4005.JP) to UTG (Ultra-thin glass) produced by Schott (AFX.GR) and thinned by Dowoo Insys (pvt) a small firm in Korea. Samsung has also been working with long-time cover glass supplier Corning (GLW) to develop UTG and is expected to use Corning’s UTG on the upcoming Galaxy Z Fold3 to be announced next month. What complicates this situation is that the new Galaxy Z Fold 3 is expected to have pen capabilities which both increases the thickness of the display and increases the need to protect the display from pen pressure. With Corning’s UTG at 50um and Schott’s at 30um the thinner UTG represents a way for Samsung to keep display thickness under control but provides less protection from the stylus pressure, which is likely to give Corning the edge for the Galaxy Fold3, while Schott will continue to provide UTG for the Galaxy Flip 3. That said, Corning is said to be working with its own Korean glass processor, eCONY (pvt) in terms of cutting while Samsung is said to be looking for a local processor to thin Corning’s UTG further.

As Chinese brands roll out additional or first-time foldables later this year, they are expected to also make the shift to UTG, but it is unclear who they will choose as a cover glass supplier. Corning is the exclusive supplier of large panel substrate glass to BOE so they have a solid relationship already existing, giving them a strong negotiating position, but the necessity for a thicker UTG is not an issue for most other foldable brand, so there will be a model by model battle for each of the new devices between current suppliers. The table below shows existing and new models expected for this year.

RSS Feed

RSS Feed