Fun with Data – 5G in 1Q – Digging Deeper

While 5G data is relatively easy to come by in China, likely because China is the 5G leader and wants the world to know, it is much more difficult to derive such data for the rest of the world. Much comes from the fact that 5G deployments vary considerably from country to country which means there is almost no 5G subscriber data for many areas and little 5G smartphone shipment data from those regions. That said, 5G smartphone shipments do not always link to subscriber growth as some customers upgrading or replacing a 4G/3G smartphone might move to 5G in anticipation of deployment in their area or country. Under that premise, we are just beginning to see data that helps to understand why smartphone brands are so interested in selling the idea of 5G to customers, aside from the fact that the smartphone market is saturated smartphone market in many developed regions.

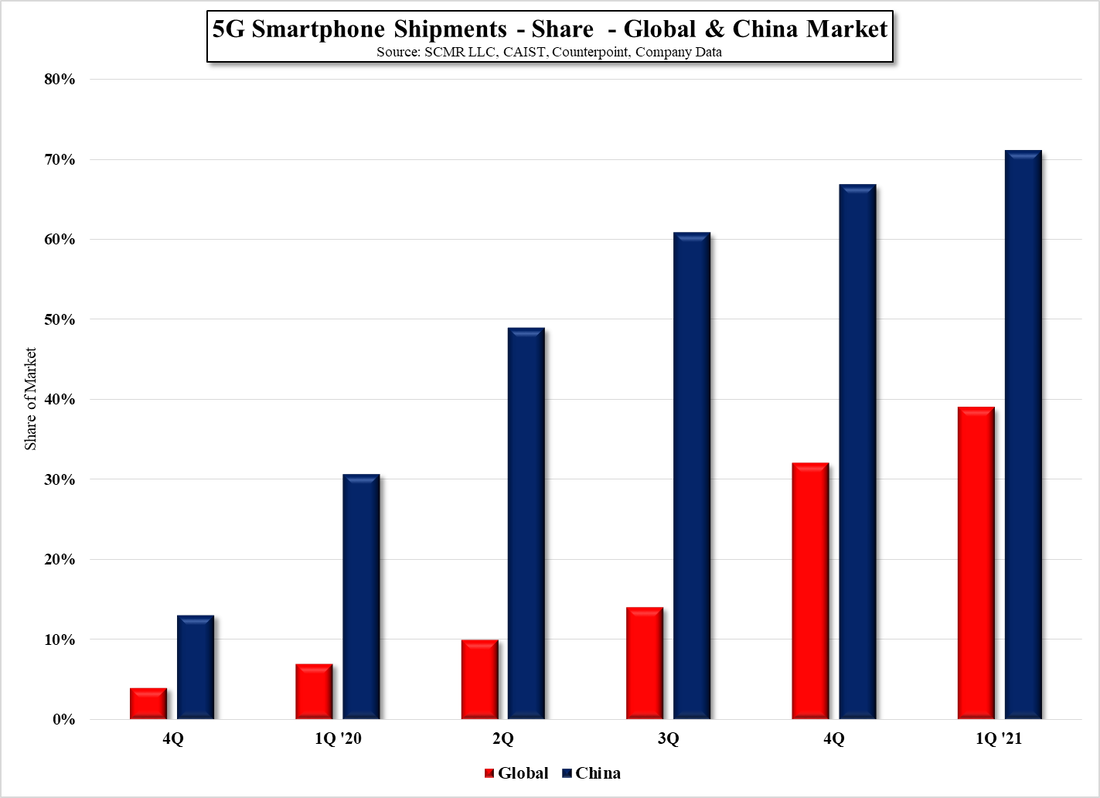

Early data for 2021 suggests that global 5G smartphone shipments represented 39% of total smartphone shipments in 1Q of this year, or ~138m units, and before we go further we note that based on our China shipment data, that 39% is far below the 71% share that 5G represents of China’s total smartphone shipments. That has been the case since the data became meaningful in 4Q 2019. Chinese consumers have embraced 5G far more aggressively that global consumers, likely because China has made a concerted effort to deploy large numbers of 5G base stations across the country, or at least in populated areas, and continues to deploy at a rapid rate. According to the Vice Minister of the Ministry of Industry & Information Technology, China has installed over 910,000 base stations across the country, accounting for ~70% of the global total.

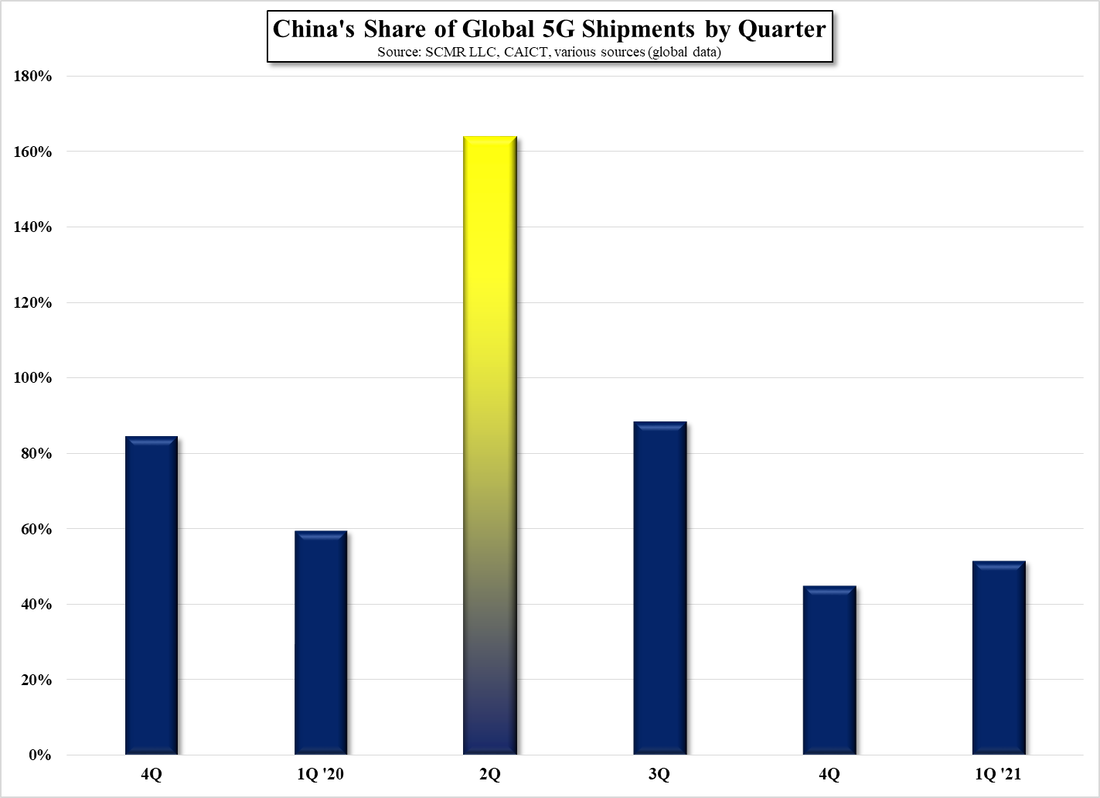

Unfortunately, as we parse the historic data there are some glaring inconsistencies. If we look at 5G shipment data for 2Q 2020, the global general consensus seems to be ~29m units, or roughly 11% of the total smartphones shipped that quarter. However data from China says that in the 2nd quarter of 2020 China shipped 49.5m 5G smartphones, or ~164% of the global total, which implies that either the global totals are incorrect, or the Chinese data is inflated. Almost all of the data on the Chinese smartphone industry comes from CAICT, the China Academy of Information & Communication Technology, which, in its own words, is a scientific research institute directly under the Ministry of Industry and Information Technology, which is an agency of the State Council, also known as the Central People’s Government, which presides over all of the countries provincial governments., alongside the Chinese Communist Party, and the People’s Liberation Army.

This makes CAICT a direct organ of the state government and likely has its releases and data carefully scrutinized by various state and party officials. While the data is at least consistent month to month in most cases, we would expect if there were any discrepancies, they would have been during the 1st half of last year when COVID-19 was at its peak in China, yet it seems that Chinese citizens, at least according to the data, were flocking to stores or on-line to purchase 5G smartphones. As specifics as to how the Chinese data is collected and what it contains, we might assume that the Chinese data includes every 5G smartphone ‘produced’ in China, whether it was sold on the Mainland or not, but data from other periods is more consistent with global numbers, so we can only accept the data as it stands but take it with a large grain of salt.

Early data for 2021 suggests that global 5G smartphone shipments represented 39% of total smartphone shipments in 1Q of this year, or ~138m units, and before we go further we note that based on our China shipment data, that 39% is far below the 71% share that 5G represents of China’s total smartphone shipments. That has been the case since the data became meaningful in 4Q 2019. Chinese consumers have embraced 5G far more aggressively that global consumers, likely because China has made a concerted effort to deploy large numbers of 5G base stations across the country, or at least in populated areas, and continues to deploy at a rapid rate. According to the Vice Minister of the Ministry of Industry & Information Technology, China has installed over 910,000 base stations across the country, accounting for ~70% of the global total.

Unfortunately, as we parse the historic data there are some glaring inconsistencies. If we look at 5G shipment data for 2Q 2020, the global general consensus seems to be ~29m units, or roughly 11% of the total smartphones shipped that quarter. However data from China says that in the 2nd quarter of 2020 China shipped 49.5m 5G smartphones, or ~164% of the global total, which implies that either the global totals are incorrect, or the Chinese data is inflated. Almost all of the data on the Chinese smartphone industry comes from CAICT, the China Academy of Information & Communication Technology, which, in its own words, is a scientific research institute directly under the Ministry of Industry and Information Technology, which is an agency of the State Council, also known as the Central People’s Government, which presides over all of the countries provincial governments., alongside the Chinese Communist Party, and the People’s Liberation Army.

This makes CAICT a direct organ of the state government and likely has its releases and data carefully scrutinized by various state and party officials. While the data is at least consistent month to month in most cases, we would expect if there were any discrepancies, they would have been during the 1st half of last year when COVID-19 was at its peak in China, yet it seems that Chinese citizens, at least according to the data, were flocking to stores or on-line to purchase 5G smartphones. As specifics as to how the Chinese data is collected and what it contains, we might assume that the Chinese data includes every 5G smartphone ‘produced’ in China, whether it was sold on the Mainland or not, but data from other periods is more consistent with global numbers, so we can only accept the data as it stands but take it with a large grain of salt.

5G Smartphone Shipments - Share - Global & China Markets - Source: SCMR LLC, CAIST, Counterpoint, Company Data

China's Share of Global 5G Shipments by Quarter - Source: SCMR LLC, CAICT, various

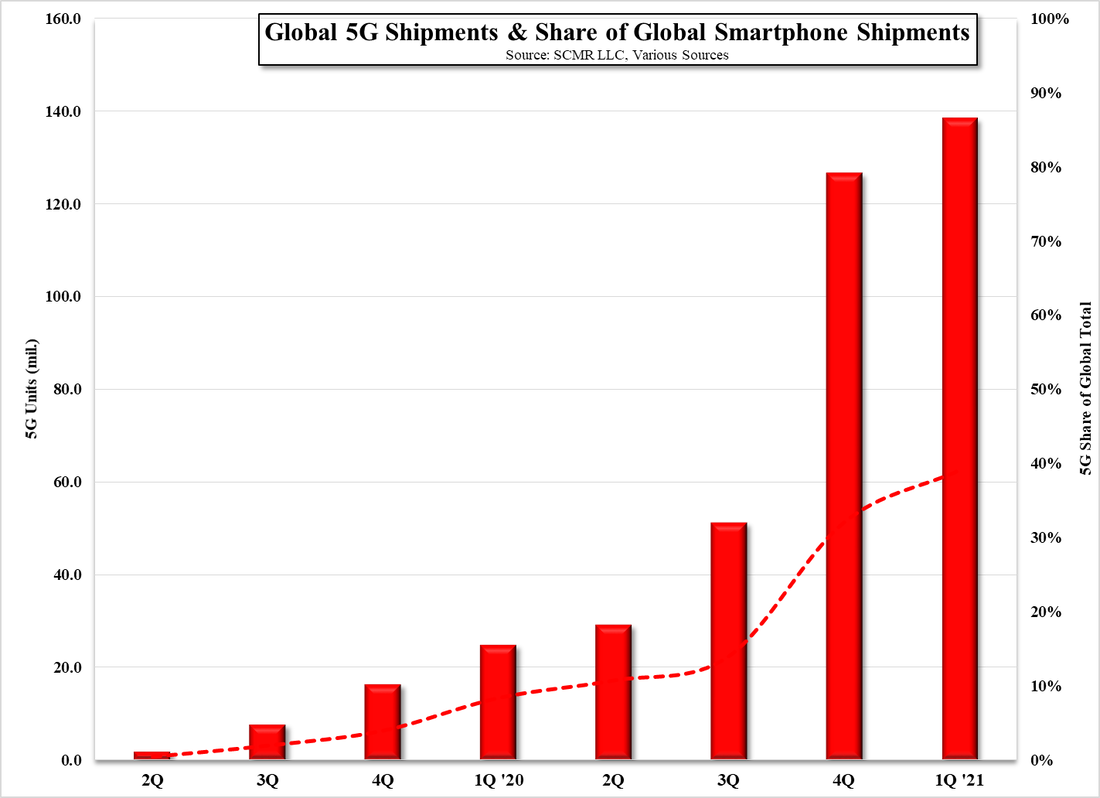

Looking at just the global data, which we derive from a number of sources, 5G smartphone shipments, both from a sales standpoint and a share of the smartphone market, have been improving, with a noticeable jump in 4Q of last year when Apple (AAPL) released the iPhone 12 series, all of which were 5G enabled. While the iPhone 12 series had a large impact on 5G smartphone shipments, it also had an unusual impact on the share of revenue generated from 5G sales, which had been tracking roughly 8% to 13% higher than the shipment share until the iPhone 12 release. As can be seen in Fig. 3, the share of revenue from 5G sales, as a percentage of total smartphone sales, jumped from 28% in 3Q 2020 to 62% in 4Q and continued to climb in 1Q of this year.

Global 5G Shipments & Share of Global Smartphone Shipments - Source: SCMR LLC, Various Sources

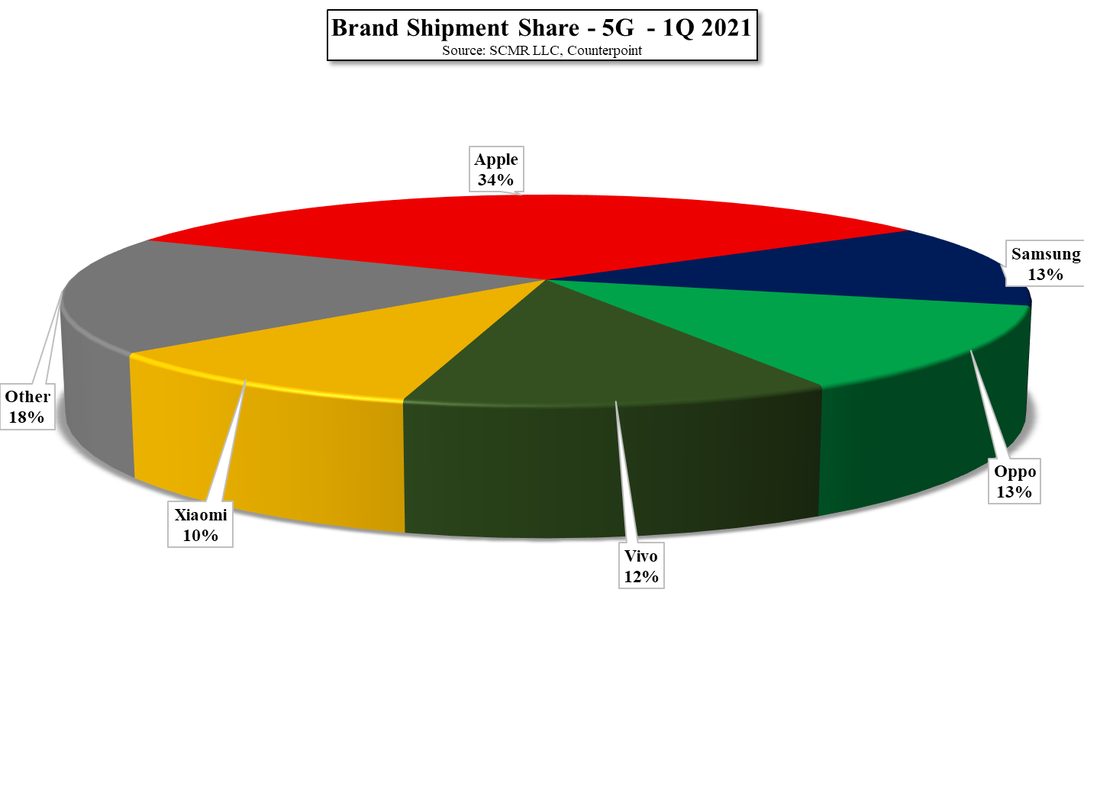

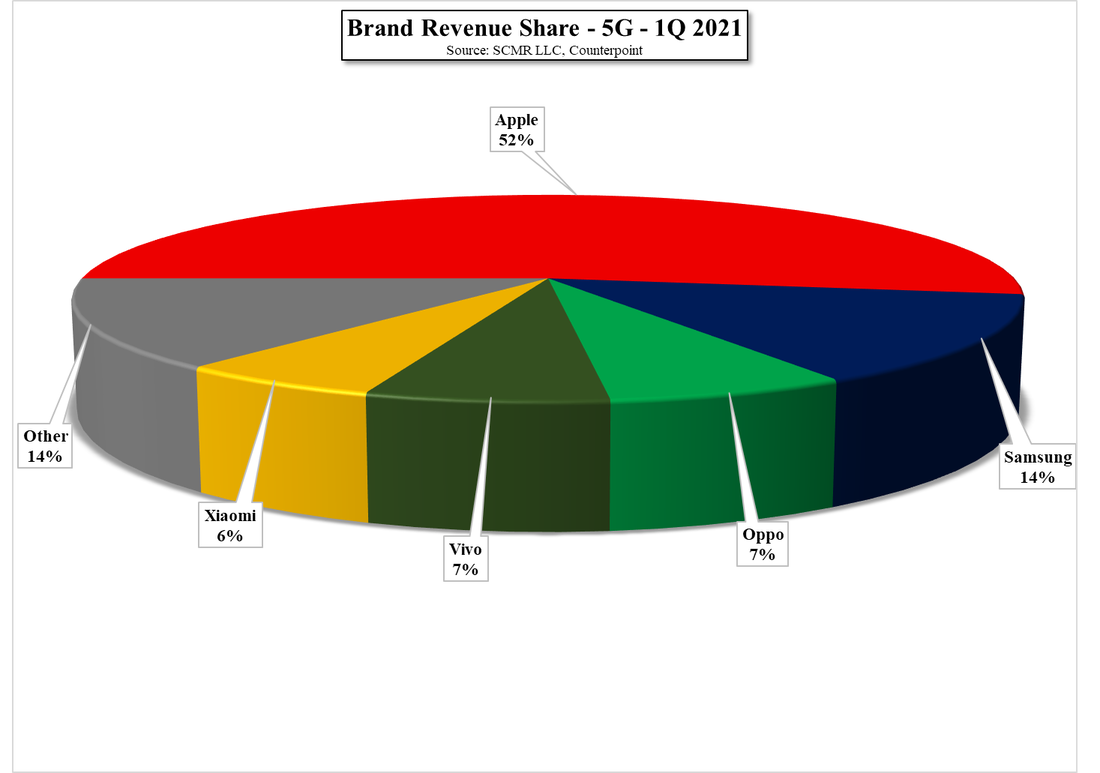

Some of that increase also came from increasing shipment share of 5G smartphone from other vendors, with the 4Q holiday season as a stimulus, but the continued share of revenue expansion into 1Q seems to indicate that Apple was much of the source. If we look more specifically at the main 5G smartphone brands, it becomes even more obvious that the release of the iPhone 12 series was the impactful event that boosted 5G revenue share across the industry, but when comparing 5G shipment share and revenue share in 1Q ’21 only Apple and Samsung (005930.KS) saw share of revenue higher than share of shipments, and Samsung by only a small amount. Apple stood out in 1Q as owning 53% of 5G revenue with only a 34% share of shipments. The data contained in Fig. 4 & Fig. 5 is summarized in the table below.

We would expect 2Q data to be similar, but while Apple could maintain a revenue share over 50% in 2Q, as new models from other brands are released, Apple’s shipment share will decrease until the iPhone 13 is released in October. We expect the revenue impact to be a bit more muted this year as some Apple users migrated to 5G last year, but we expect the release will still be impactful. If Apple pulls in the release date a bit to compete with Samsung’s potential updated foldable line, the 3Q boost could be closer to what was seen last year, with the understanding that last year was both an anomaly from the standpoint of the growth limitations that COVID-19 put on 5G growth, and as the first full year of meaningful 5G smartphone shipments and sales. While this year will still see the impact of COVID-19 on the smartphone market, perhaps more through component shortages than physical limitations, and 5G smartphone offerings have proliferated considerably from last year, 5G smartphone shipments and sales will see more subdued q/q growth and less of an impact from individual brands.

We would expect 2Q data to be similar, but while Apple could maintain a revenue share over 50% in 2Q, as new models from other brands are released, Apple’s shipment share will decrease until the iPhone 13 is released in October. We expect the revenue impact to be a bit more muted this year as some Apple users migrated to 5G last year, but we expect the release will still be impactful. If Apple pulls in the release date a bit to compete with Samsung’s potential updated foldable line, the 3Q boost could be closer to what was seen last year, with the understanding that last year was both an anomaly from the standpoint of the growth limitations that COVID-19 put on 5G growth, and as the first full year of meaningful 5G smartphone shipments and sales. While this year will still see the impact of COVID-19 on the smartphone market, perhaps more through component shortages than physical limitations, and 5G smartphone offerings have proliferated considerably from last year, 5G smartphone shipments and sales will see more subdued q/q growth and less of an impact from individual brands.

Brand Shipment Share - 5G - 1Q 2021 - Source: SCMR LLC, Counterpoint

Brand Revenue Share - 5G - 1Q - 2021 - Source: SCMR LLC, Counterpoint

RSS Feed

RSS Feed