Fun with Data – iPad Procurement

Chinese panel producer BOE (200725.CH) has been on a roller coaster ride with Apple (AAPL), with Apple rejecting the company’s displays for entry into the iPhone supply chain a number of times in 2020 and 2021, but the company persevered and was accepted into the exclusive fold typically dominated by Samsung Display (pvt) and LG Display (LPL). Just when things seemed to be going well, stories began to circulate earlier this year that BOE had changed driver circuitry on a display it was supplying to Apple without permission, and they were suspended from iPhone production for a period of time. Since then there have been various projections as to how much participation BOE will have in the iPhone 14 series, which should begin this month.

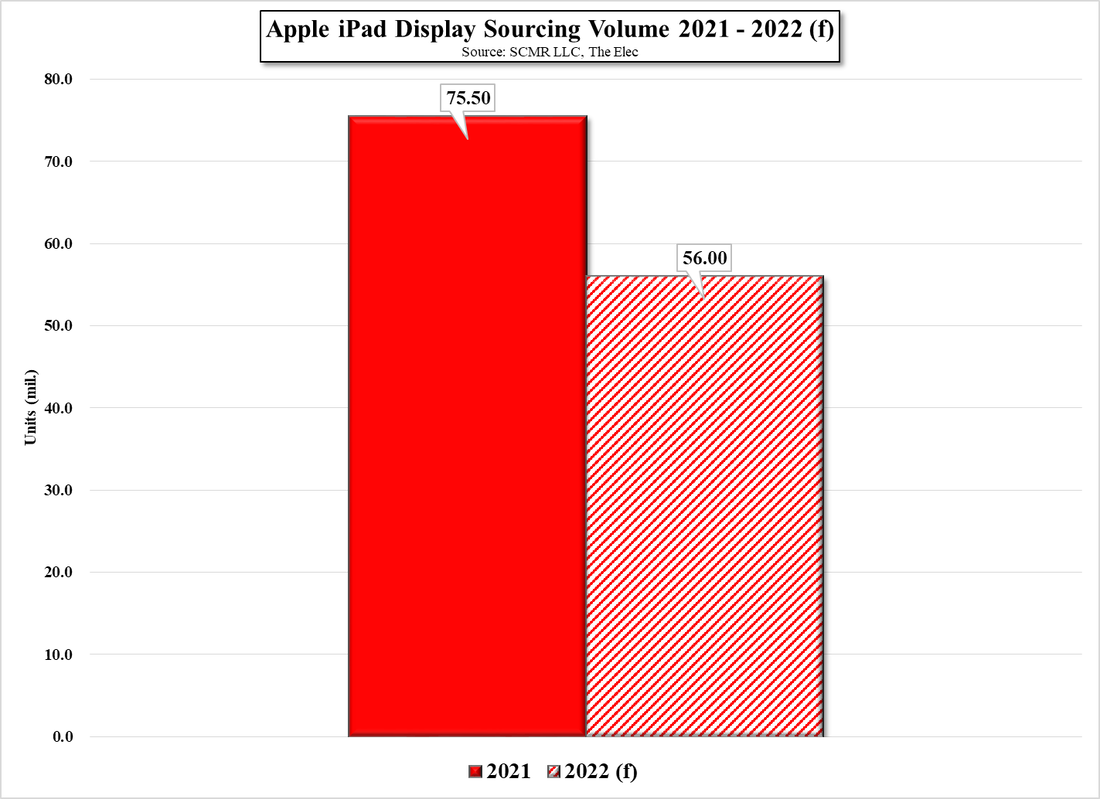

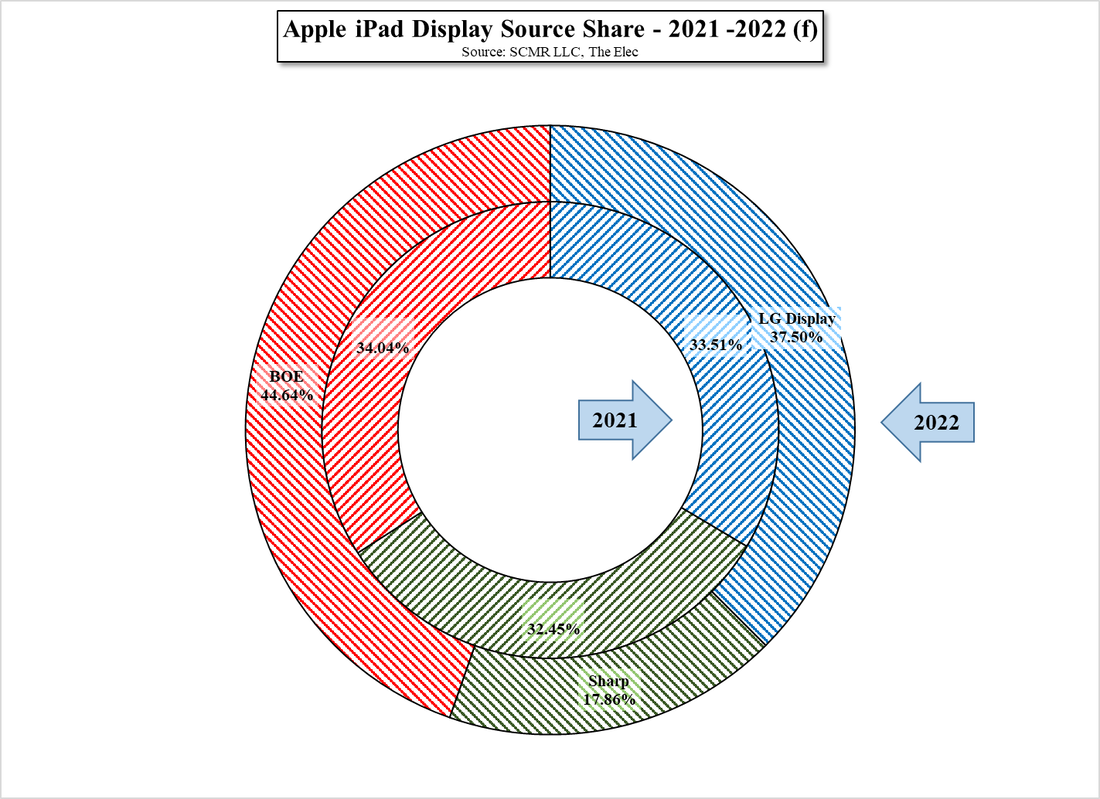

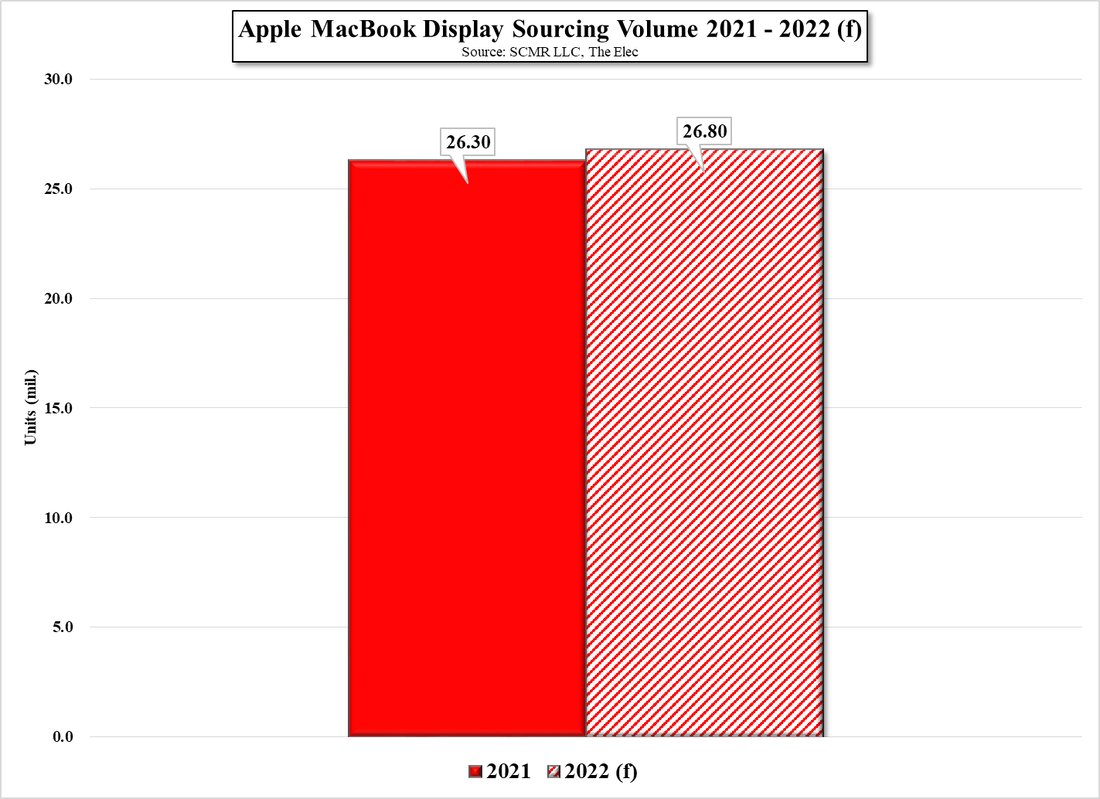

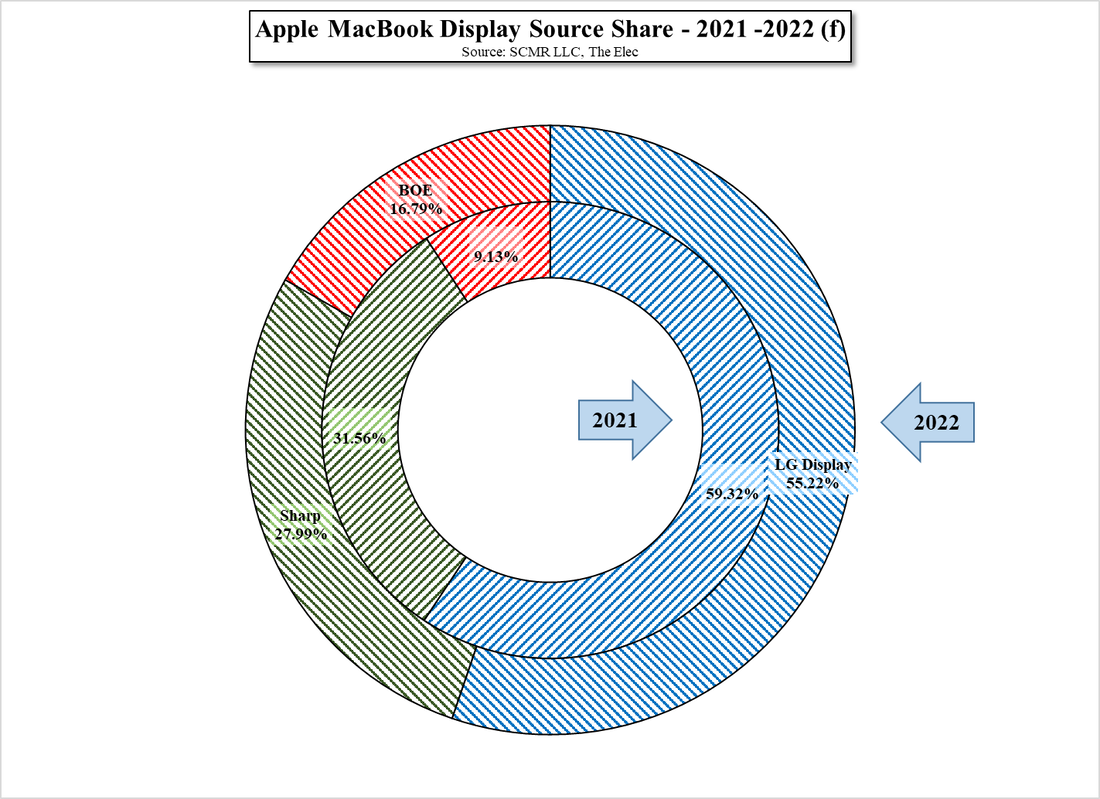

Much has been made in the Chinese trade press as to how BOE is now challenging South Korean dominance in Apple’s display supply chain, with considerable and mostly well-deserved nationalistic pride, but while the press champions BOE’s success with the iPhone, they miss the fact that BOE was the primary supplier of LCD displays to Apple’s iPad line in 2021 and is expected to remain so this year, despite reductions in Apple’s display procurement for the product., which is expected to decline by 25.8%. In fact, if estimates for LCD iPad display procurement are correct, BOE will see only a small drop in y/y units shipped (-2.7%), while LG Display will see a 17.0% reduction in units and Sharp (6753.JP) will see a 59.2% y/y unit reduction this year. MacBook shipments are expected to see a 1.9% increase this year, and while BOE will not have the dominant share, it will be the only supplier to see an increase in units (+87.5%), with both LG Display (-5.1%) and Sharp (-9.6%) seeing decreases, which points to the fact that BOE, while still facing some challenges in the OLED space, is seeing considerable success with Apple in the LCD display space.

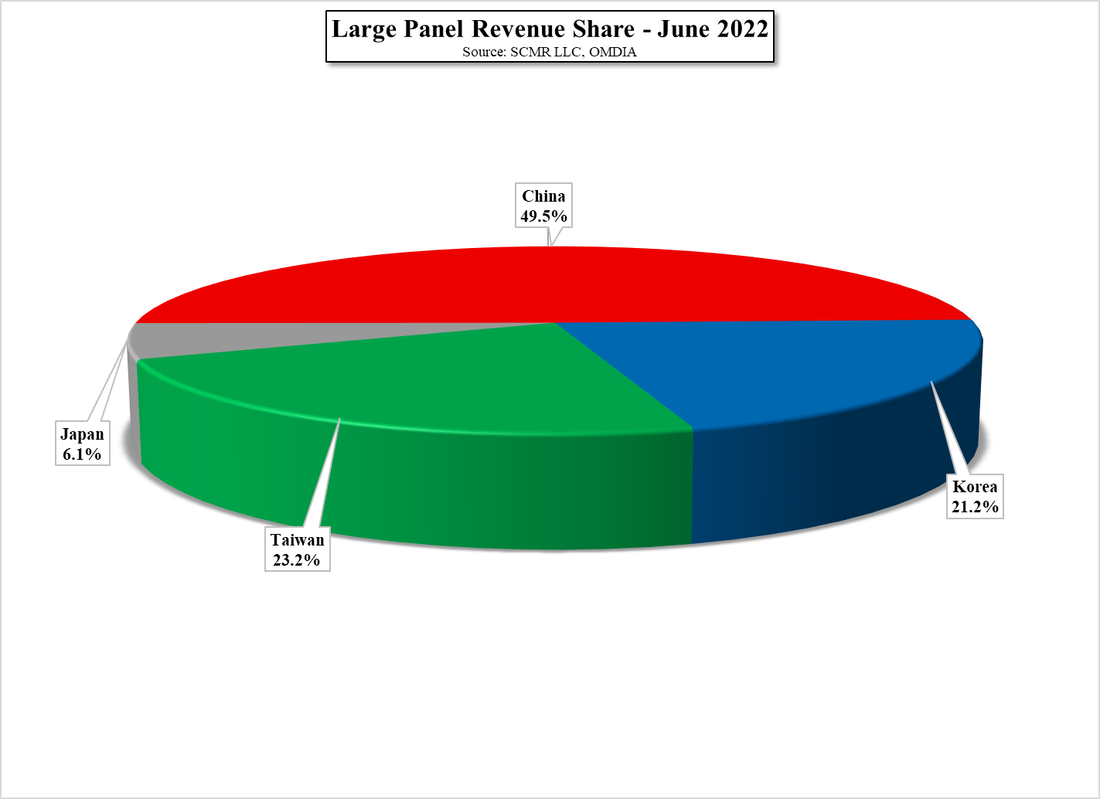

While OLED displays, particularly flexible OLED displays tend to be the focus for number crunching and press releases, there is still a vast LCD display world that gets little recognition unless it has ‘quantum dot’ or ‘mini-LED’ attached, but that world is still a very large one with ~891.2m large panel LCD units shipped last year, generating over $85b in revenue and one that Chinese display producers dominate. While the Chinese press glorifies any statistics that show Chinese supremacy in the display space, credit is due to BOE, Chinastar (pvt) and other Chinese LCD display producers, who hold the top share in the large pane LCD space. One can question whether that will be as valuable a position 5 years from now, but currently they certainly have accomplished their goal of becoming the leading source of large panel LCD displays.

Much has been made in the Chinese trade press as to how BOE is now challenging South Korean dominance in Apple’s display supply chain, with considerable and mostly well-deserved nationalistic pride, but while the press champions BOE’s success with the iPhone, they miss the fact that BOE was the primary supplier of LCD displays to Apple’s iPad line in 2021 and is expected to remain so this year, despite reductions in Apple’s display procurement for the product., which is expected to decline by 25.8%. In fact, if estimates for LCD iPad display procurement are correct, BOE will see only a small drop in y/y units shipped (-2.7%), while LG Display will see a 17.0% reduction in units and Sharp (6753.JP) will see a 59.2% y/y unit reduction this year. MacBook shipments are expected to see a 1.9% increase this year, and while BOE will not have the dominant share, it will be the only supplier to see an increase in units (+87.5%), with both LG Display (-5.1%) and Sharp (-9.6%) seeing decreases, which points to the fact that BOE, while still facing some challenges in the OLED space, is seeing considerable success with Apple in the LCD display space.

While OLED displays, particularly flexible OLED displays tend to be the focus for number crunching and press releases, there is still a vast LCD display world that gets little recognition unless it has ‘quantum dot’ or ‘mini-LED’ attached, but that world is still a very large one with ~891.2m large panel LCD units shipped last year, generating over $85b in revenue and one that Chinese display producers dominate. While the Chinese press glorifies any statistics that show Chinese supremacy in the display space, credit is due to BOE, Chinastar (pvt) and other Chinese LCD display producers, who hold the top share in the large pane LCD space. One can question whether that will be as valuable a position 5 years from now, but currently they certainly have accomplished their goal of becoming the leading source of large panel LCD displays.

Apple iPad Display Sourcing Volume - 2021 - 2022 (f) - Source: SCMR LLC, The Elec

Apple iPad Display Source Share - 2021 - 2022 (f) - Source: SCMR LLC, The Elec

Apple MacBook Display Sourcing Volume - 2021 - 2022(f) - Source: SCMR LLC, The Elec

Apple MacBook Display Source Share - 2021 - 2022(f) - Source: SCMR LLC, The Elec

Large Panel Revenue Share - June 2022 - Source: SCMR LLC, OMDiA

RSS Feed

RSS Feed