Fun with Data – Semi Equipment

Semi.org is a global industry association that represents electronics manufacturing and design supply chain covering ~1.3m industry workers and more than 2,500 members. The organization tracks various aspects of semiconductor industry spending and publishes forecasts and data for its members and occasionally, the public. The organization just released expectations for semiconductor equipment spending for this year and next, estimating 14.5% growth this year and 2.8% growth in 2023. Based on their expectations for 2022 the implication would be for 2H sales of $66.39b, up 29.9% over the 1st half and up 22.5% y/y. At 56.5% of the full year estimate, the year is a bit weighted toward 2H as the typical 2H ratio of full year sales is 52.4%.

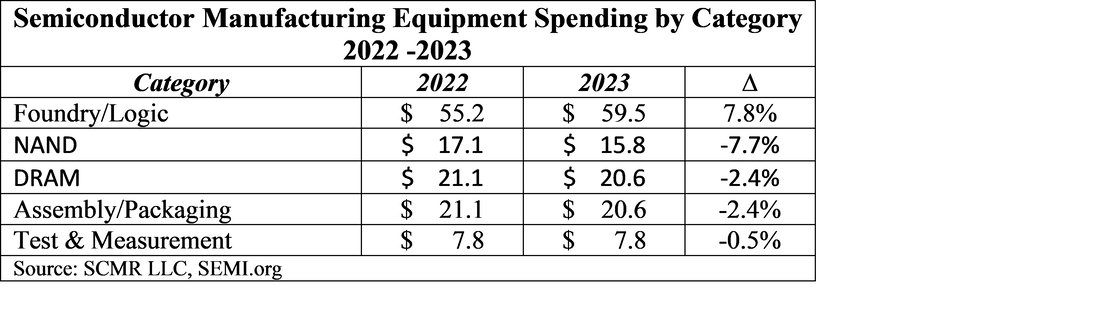

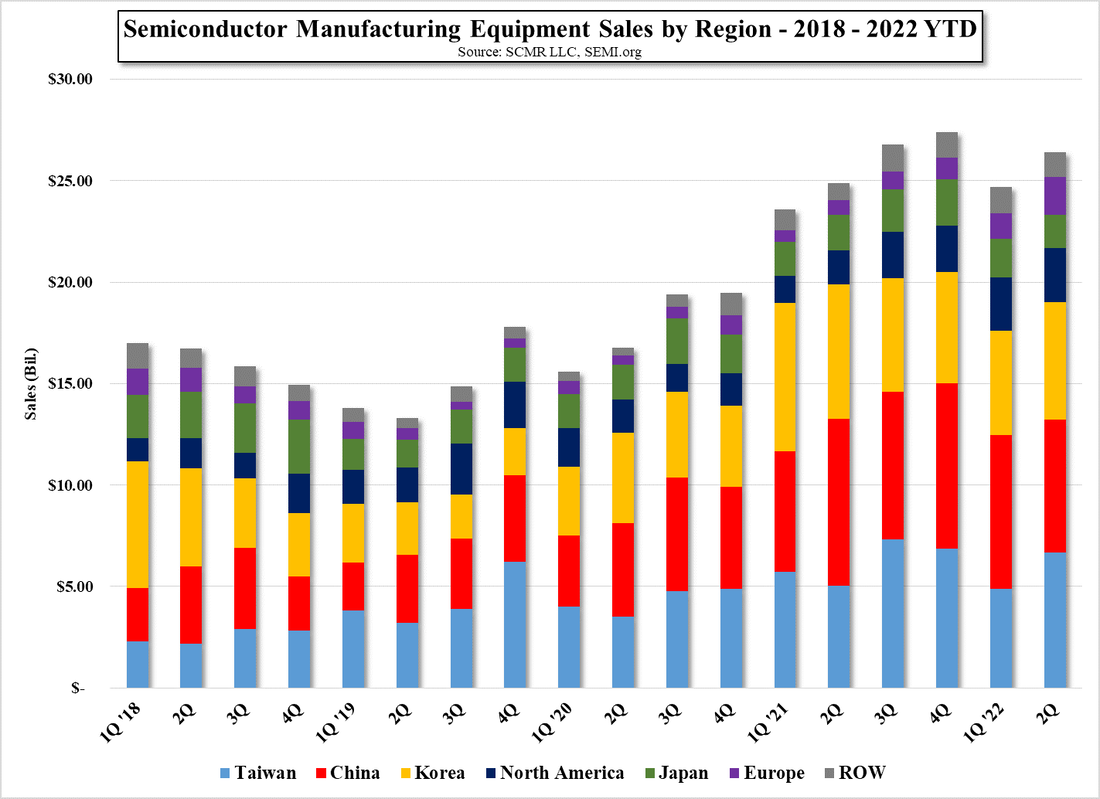

Almost all of the growth in 2023 will be from Foundry & Logic equipment, which is expected to grow from 55.2b to 59.5b, while memory/storage and Assembly & Packaging tool sales are expected to decline modestly from 7.8B to 7.7b, with Test & Measurement tool sales increasing slightly by 0.4%. On a regional basis, Taiwan regained 1st place over China in 2Q after falling behind Mainland equipment sales in 4Q of last year, although both regions had almost identical spending in 2Q. As we have previously noted, Chinese foundries have accelerated purchases of lithography equipment in anticipation of the US tightening restrictions on DUV tools following restrictions on more advanced node EUV tools. While China continues to expand its semiconductor foundry business at a rapid pace, we expect the value of foundry and locic equipment sales will see less growth as US trade restrictions further limit tool purchases to mature nodes, while Taiwan and Korea are able to purchase those higher priced but higher value tools without restriction.

Almost all of the growth in 2023 will be from Foundry & Logic equipment, which is expected to grow from 55.2b to 59.5b, while memory/storage and Assembly & Packaging tool sales are expected to decline modestly from 7.8B to 7.7b, with Test & Measurement tool sales increasing slightly by 0.4%. On a regional basis, Taiwan regained 1st place over China in 2Q after falling behind Mainland equipment sales in 4Q of last year, although both regions had almost identical spending in 2Q. As we have previously noted, Chinese foundries have accelerated purchases of lithography equipment in anticipation of the US tightening restrictions on DUV tools following restrictions on more advanced node EUV tools. While China continues to expand its semiconductor foundry business at a rapid pace, we expect the value of foundry and locic equipment sales will see less growth as US trade restrictions further limit tool purchases to mature nodes, while Taiwan and Korea are able to purchase those higher priced but higher value tools without restriction.

Semiconductor Manufacturing Equipment Sales - 2017 - 2023 - Source: SCMR LLC, SEMI.org

Semiconductor Manufacturing Equipment Sales by Region - 2Q 2022 - Source: SCMR LLC, SEMI.org

Semiconductor Manufacturing Equipment Sales by Region - 2018 - 2022 YTD - Source: SCMR LLC, SEMI.org

RSS Feed

RSS Feed