Fun with Data – Small Panel OLED Demand & Apple

Last week we noted that demand for small panel (primarily smartphone applications) rigid OLED displays in 2Q was considerably below expectations (missed by 25.9%), coming in down 19.5% q/q and down 33.2% y/y. Much of the small panel OLED demand shortfall came from Samsung Electronics (005930.KS) and Xiaomi (1810.HK), and has led to expectations for 3Q small panel OLED rigid demand to decline by 25.9% q/q and by 46.5% y/y. While these are certainly concerning data points, we also noted that small panel rigid OLED displays are an increasingly smaller part of overall small panel OLED displays, falling to 38.6% in 2Q and averaging 40.1% in 1H after 2021’s average of 44.0%, which puts the focus more specifically on small panel flexible OLED displays for a better understanding of demand for the smartphone OLED display market.

Now that we have full demand data for small panel flexible OLED displays, we note that the results for flexible OLED displays in 2Q was only off by 1.9% putting 2Q composite small panel OLED demand 12.85% below expectations, not a great number but certainly better than the rigid miss. As can be seen in the table below, while both Apple (AAPL) and Vivo (pvt) came in above small panel flexible OLED expectations, Apple represented 49.6% of actual small panel flexible OLED demand in 2Q and was the only brand that saw better than expected results in the composite, with the composite itself being down 13.6% q/q and down 3.4% y/y.

Now that we have full demand data for small panel flexible OLED displays, we note that the results for flexible OLED displays in 2Q was only off by 1.9% putting 2Q composite small panel OLED demand 12.85% below expectations, not a great number but certainly better than the rigid miss. As can be seen in the table below, while both Apple (AAPL) and Vivo (pvt) came in above small panel flexible OLED expectations, Apple represented 49.6% of actual small panel flexible OLED demand in 2Q and was the only brand that saw better than expected results in the composite, with the composite itself being down 13.6% q/q and down 3.4% y/y.

The weak results in 2Q and the ongoing macro challenges facing the smartphone market have brought down expectations for small panel OLED demand in 3Q although there is hope for a relatively small amount of q/q growth (3.4%), as shown in the table below. While these expectations translate to a decline of 20.3% (composite) on a y/y basis Apple, Honor (pvt) and Huawei (pvt) are expected to see q/q increases, with only Huawei seeing a y/y increase, a result of the extremely poor results Huawei saw in 2021 due to US trade restrictions.

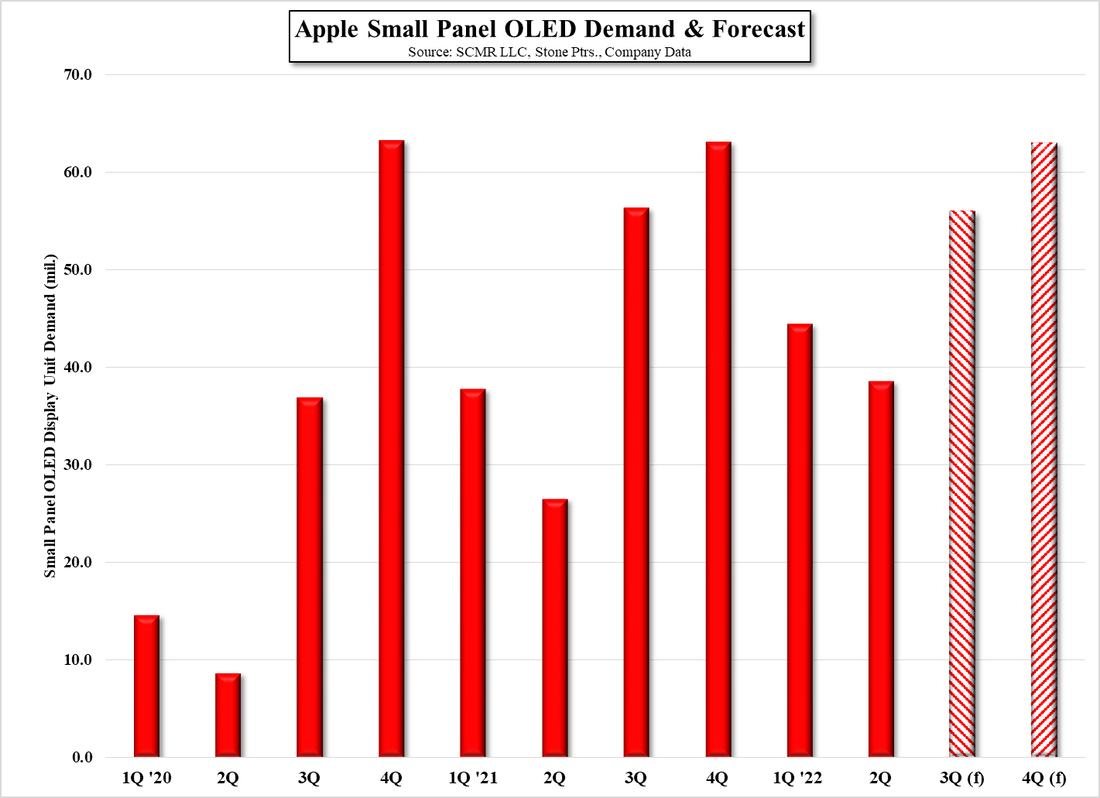

All in, another weak quarter for smartphones continues to put a damper on small panel OLED growth, despite an increasing share of the overall smartphone market, with Apple the only substantial standout. As the iPhone 14 series was announced on September 7, much of the 3Q actual results will rest on the new iPhone line’s popularity during the last 15 days of the month, and based on those results, Apple will determine it order rate for 4Q. In 2020 and 2021 Apple increased orders q/q in 4Q (11.9% and 71.5% respectively) while the y/y increase was less than 1%. While we expect Apple is optimistic about customer demand for the iPhone 14 series, we assume they will temper that enthusiasm a bit as the macro-economic situation continues to weigh on consumer spending, which would lead us to expect Apple’s full year small panel OLED demand to be ~200m units, up 9.8% y/y. Given that almost all of Apple’s iPhone models (old and new) are OLED, this gives a good approximation of Apple’s 2022 display demand, which should translate into shipments, less build and transport timing and existing inventory.

All in, another weak quarter for smartphones continues to put a damper on small panel OLED growth, despite an increasing share of the overall smartphone market, with Apple the only substantial standout. As the iPhone 14 series was announced on September 7, much of the 3Q actual results will rest on the new iPhone line’s popularity during the last 15 days of the month, and based on those results, Apple will determine it order rate for 4Q. In 2020 and 2021 Apple increased orders q/q in 4Q (11.9% and 71.5% respectively) while the y/y increase was less than 1%. While we expect Apple is optimistic about customer demand for the iPhone 14 series, we assume they will temper that enthusiasm a bit as the macro-economic situation continues to weigh on consumer spending, which would lead us to expect Apple’s full year small panel OLED demand to be ~200m units, up 9.8% y/y. Given that almost all of Apple’s iPhone models (old and new) are OLED, this gives a good approximation of Apple’s 2022 display demand, which should translate into shipments, less build and transport timing and existing inventory.

Apple Small Panel OLED Demand & Forecast - Source: SCMR LLC, Stone Ptrs, Company Data

RSS Feed

RSS Feed