LCD Large Panel Shipments – July Final

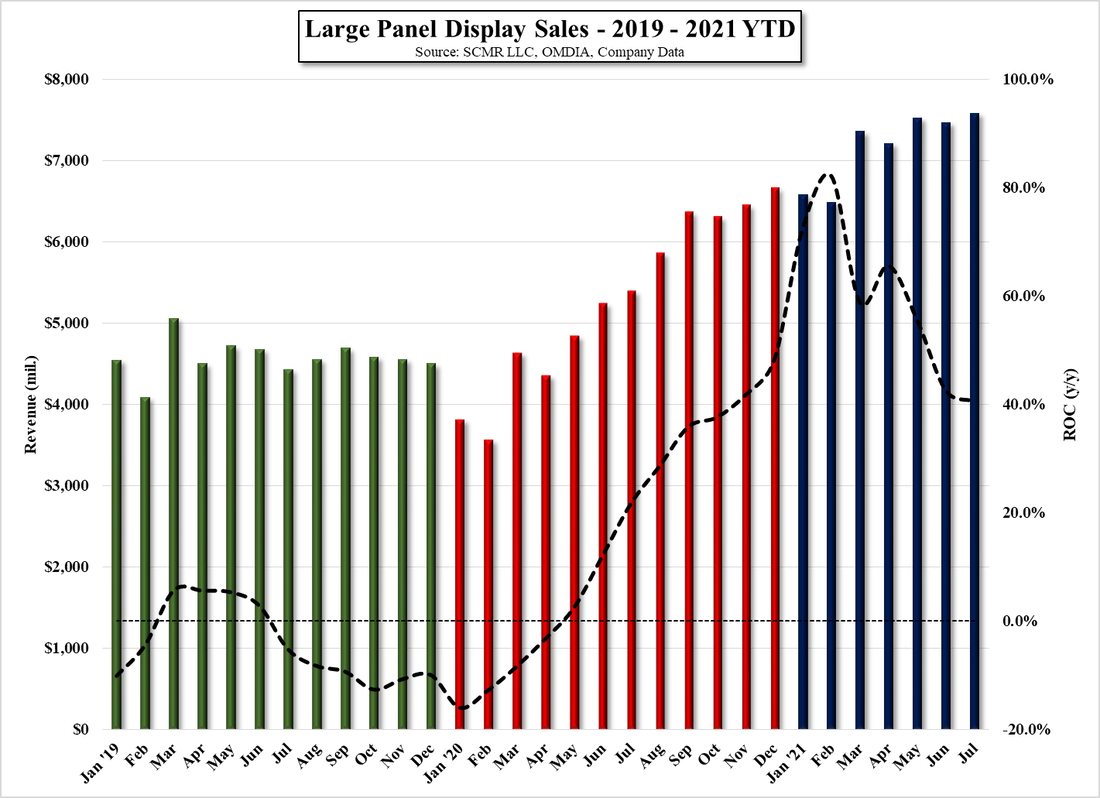

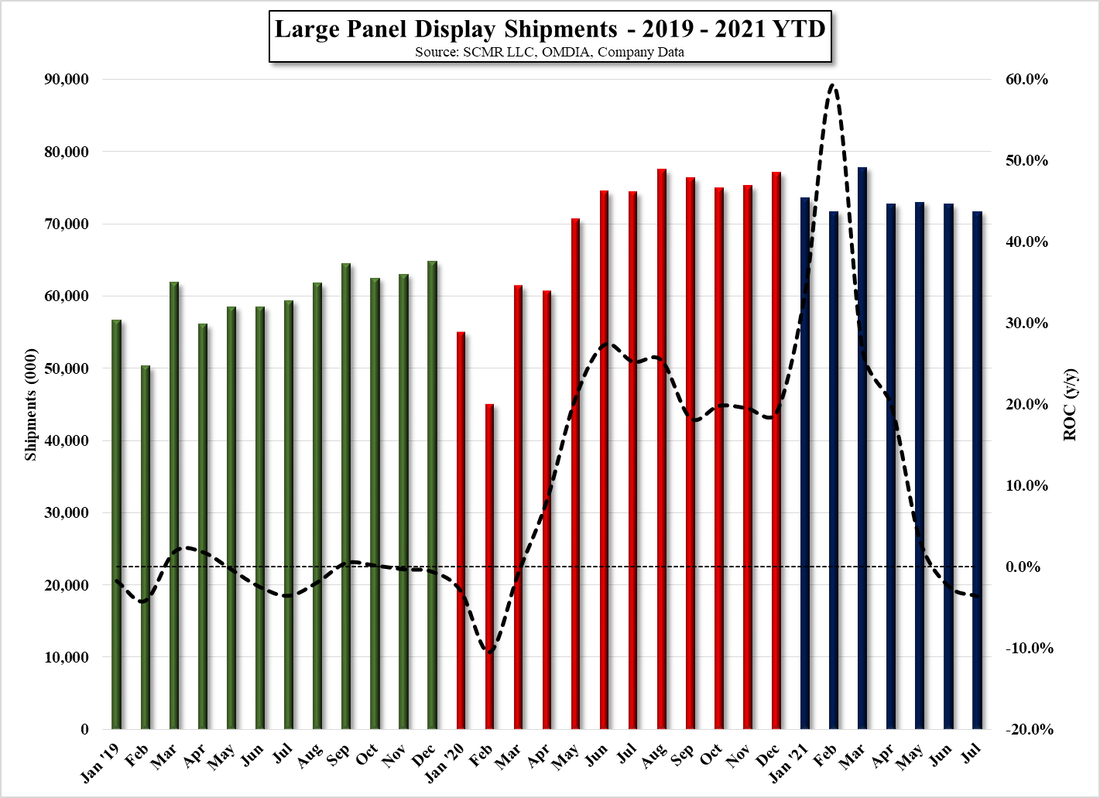

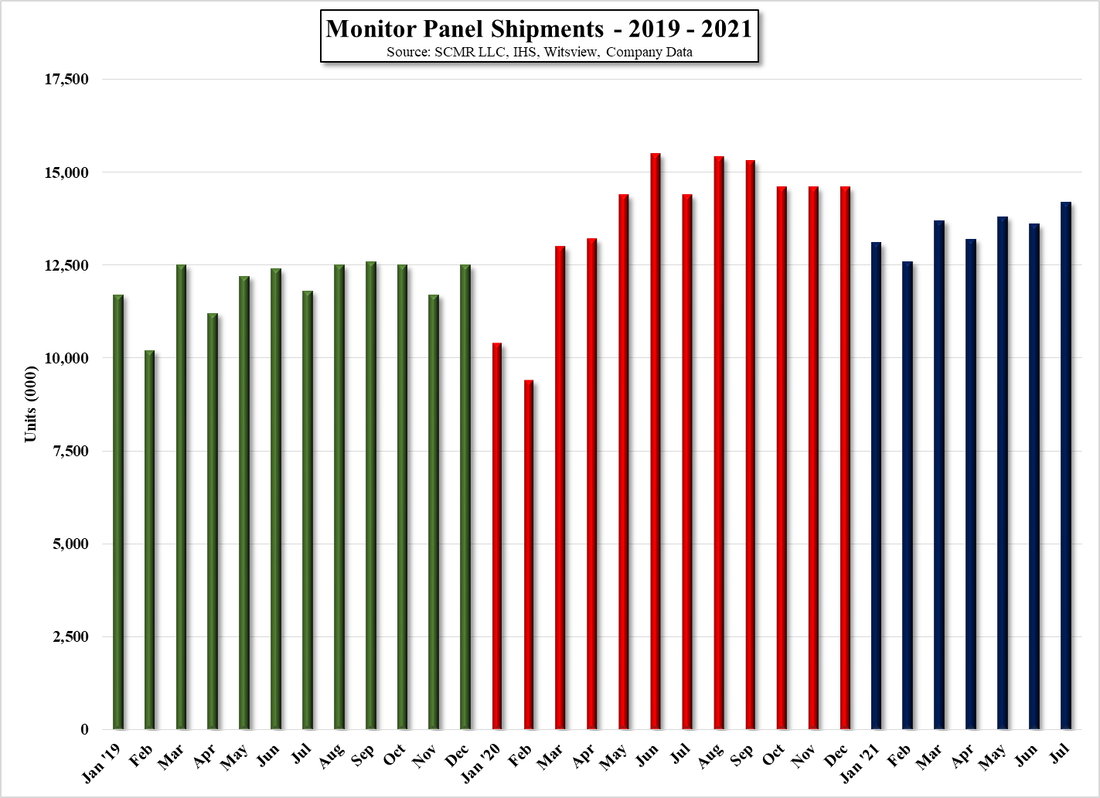

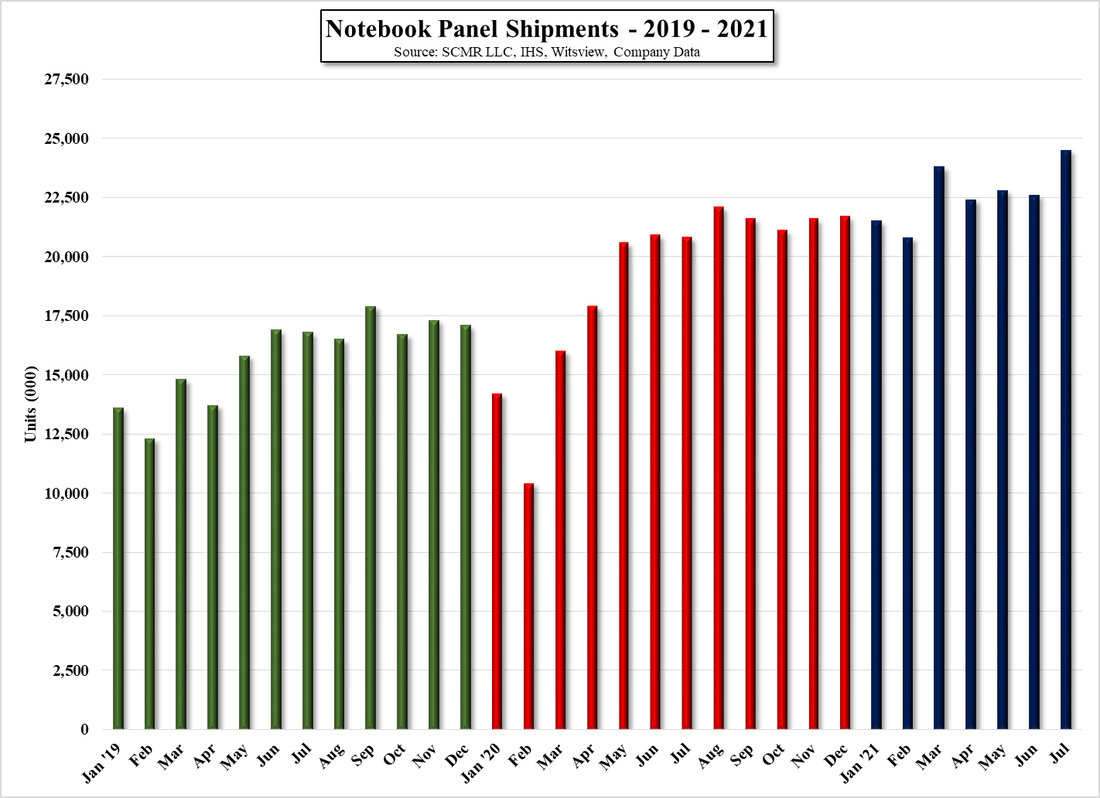

After seeing August results for panel prices above, the fact that large panel sales increased in July by 1.5% seems a bit unspectacular. While we would expect the impact of the August drop in large panel prices to be felt the greatest in China, as it has been averaging 48.7% of industry large panel sales, both Taiwan (26.5% avg.) and South Korea (19.7%) will also feel some of the effects, and any slowdown in shipments of panel prices for monitors and notebooks will exacerbate the impact. July saw overall large panel shipments down 1.4% m/m but was offset by a 2.9% increase in ASP (m/m) which is a bit off from typical July shipments, which average (5 year) +1.0%. August is typically a stronger month, averaging +4.8% in m/m shipments and a 5.6% increase in large panel sales, but the impact of the TV panel price drop will impact overall industry sales, regardless of shipments, unless there is some anomaly that pushes shipments out of normal range for August. As July is a ‘rear-view mirror’ month, given what we know about August, the charts below will tell the story.

Large Panel Display Sales - 2019 - 2021 YTYD - Source: SCMR LLC, OMDIA, Company Data

Large Panel Display Shipments - 2019 - 2021 YTD - Source: SCMR LLC, OMDIA, Company Data

Monitor Panel Shipments - 2019 - 2021 YTD - Source: SCMR LLC, IHS, Witsview, Company Data

Notebook Panel Shipments - 2019 - 2021 YTD - Source: SCMR LLC, IHS, Witsview, Company Data

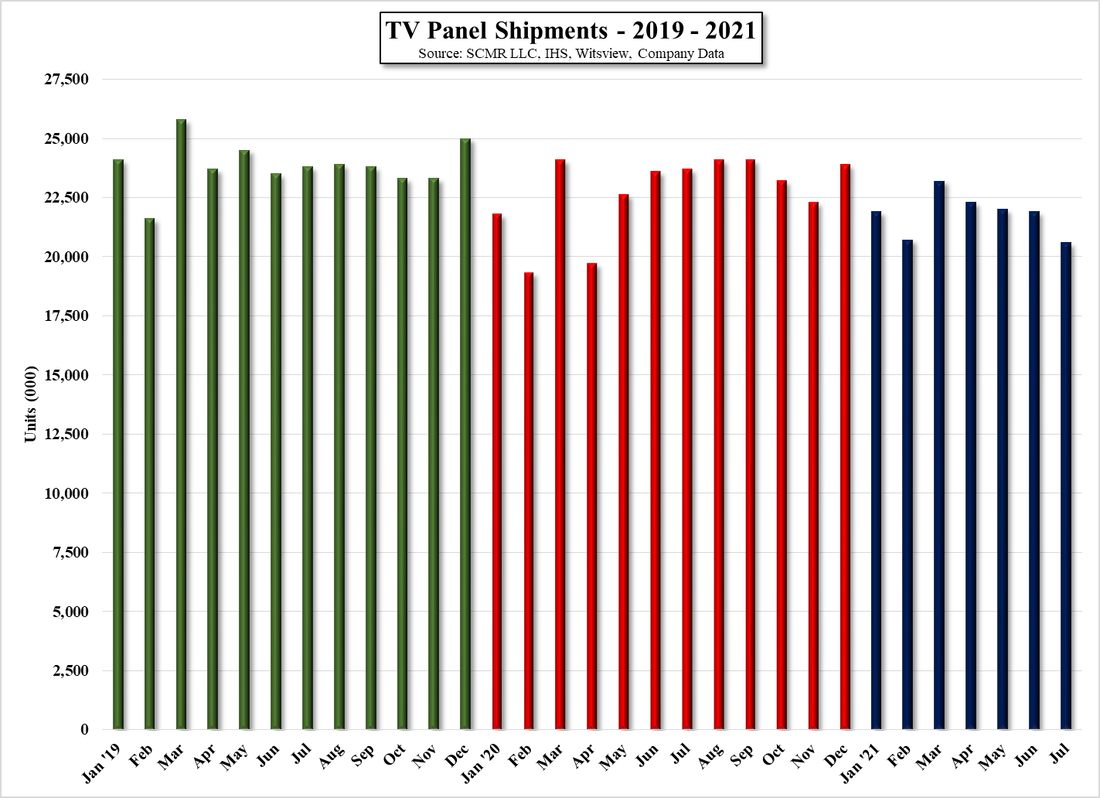

TV Panel Shipments - 2019 - 2021 YTD - Source: SCMR LLC, IHS, Witsview, Company Data

RSS Feed

RSS Feed