Did TV panel price increases hurt holiday sales in China?

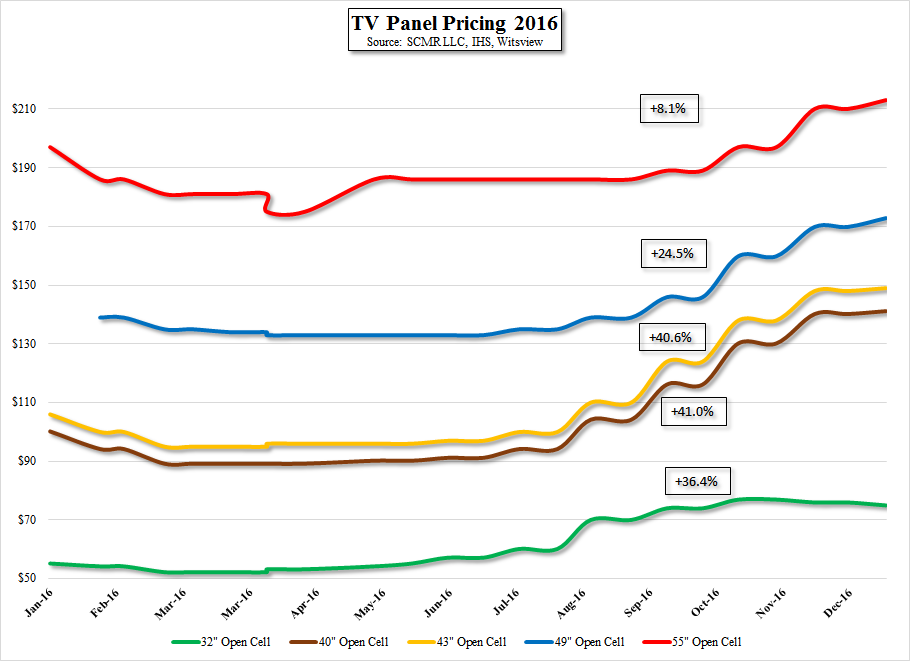

TV panel prices rose significantly in 2016, and while panel producers benefitted, TV brands suffered as the higher panel price eroded their gross margins and gave them less flexibility to discount during holiday periods. China, which has been the driver for TV growth during the last few years, saw TV unit volumes grow only 7.9% to ~51m units, despite relatively strong sales early in the year, but the impact of higher panel prices on TV set pricing was felt during the Chinese holiday season, which saw an 11.4% decline in unit volumes y/y during the Chinese New Year and Spring Festival in late January and early February. The cause of the decline is considered to be the lack of discounting and overall higher TV pricing.

Expectations for the Chinese TV market this year (2017) are for a decline of ~2.8% in units (1.7m units) making the sensitivity toward TV panel prices extremely high. A continuation of price increases could further damage the growth of the Chinese TV market, and while brands and panel producers all focus on large screen sizes and 4K/HDR premium oriented sets to maintain margins and dollar volume, the industry, particularly China is facing negative growth as a result of the TV panel price increases.

Would we expect panel producers to altruistically lower prices to help brands generate profitability? Not really, especially as they were on the other side of the ‘seller’s market’ for quite some time, but as TV set producers struggle to burn through inventory and lower expectations for quarterly and yearly shipments, a lack of buyer enthusiasm might spark a little price competition among panel producers, who need to keep fabs at near 100% utilization or see rapid declines in margins. Should that occur, and we believe it is a possibility for those TV panel sizes that have not seen increases from artificial supply issues, TV brands might have a chance to see profitability improvements later this year, with the tradeoff being lower margins at panel producers. There is potential for a balance, with panel producers still seeing profits, albeit not peak level, and brands seeing margin improvement, but it is a fine line that is rarely walked in the display space.

Expectations for the Chinese TV market this year (2017) are for a decline of ~2.8% in units (1.7m units) making the sensitivity toward TV panel prices extremely high. A continuation of price increases could further damage the growth of the Chinese TV market, and while brands and panel producers all focus on large screen sizes and 4K/HDR premium oriented sets to maintain margins and dollar volume, the industry, particularly China is facing negative growth as a result of the TV panel price increases.

Would we expect panel producers to altruistically lower prices to help brands generate profitability? Not really, especially as they were on the other side of the ‘seller’s market’ for quite some time, but as TV set producers struggle to burn through inventory and lower expectations for quarterly and yearly shipments, a lack of buyer enthusiasm might spark a little price competition among panel producers, who need to keep fabs at near 100% utilization or see rapid declines in margins. Should that occur, and we believe it is a possibility for those TV panel sizes that have not seen increases from artificial supply issues, TV brands might have a chance to see profitability improvements later this year, with the tradeoff being lower margins at panel producers. There is potential for a balance, with panel producers still seeing profits, albeit not peak level, and brands seeing margin improvement, but it is a fine line that is rarely walked in the display space.

TV Panel Pricing in 2016 - Source: SCMR LLC, IHS, Witsview

RSS Feed

RSS Feed