May Panel Pricing and April Panel Shipments

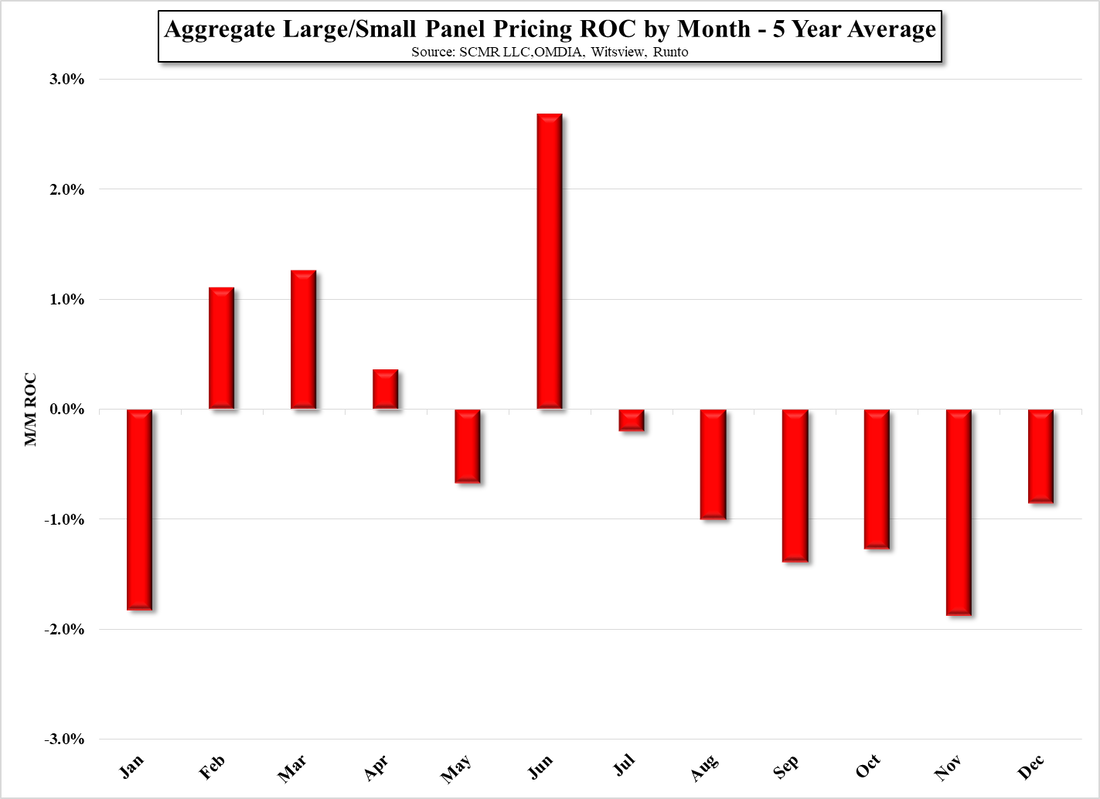

May display panel pricing was worse than expected, but more significant is the forecast for June, which is typically the strongest m/m gain for the year and potentially the beginning of the holiday build season. Given there are a number of unusual circumstances surrounding the CE space and the display industry, particularly the COVID lockdowns in China that have disrupted the supply chain and slowed Chinese CE demand, however as we noted last week, Chinese LCD panel producers have made relatively minor adjustments to their utilization rates and have therefore been pushed to keep lowering prices in order to attract customers. Inventories remain relatively high in the channel for most display products but it seems that industry expectations remain fixed on a demand recovery in 3Q. There will be some new device production increases in July as Apple (AAPL) and others prepare products for the holidays but initial orders generally are modest as brands have already lowered targets and China’s lockdown policy continues to pressure the production and assembly supply chain.

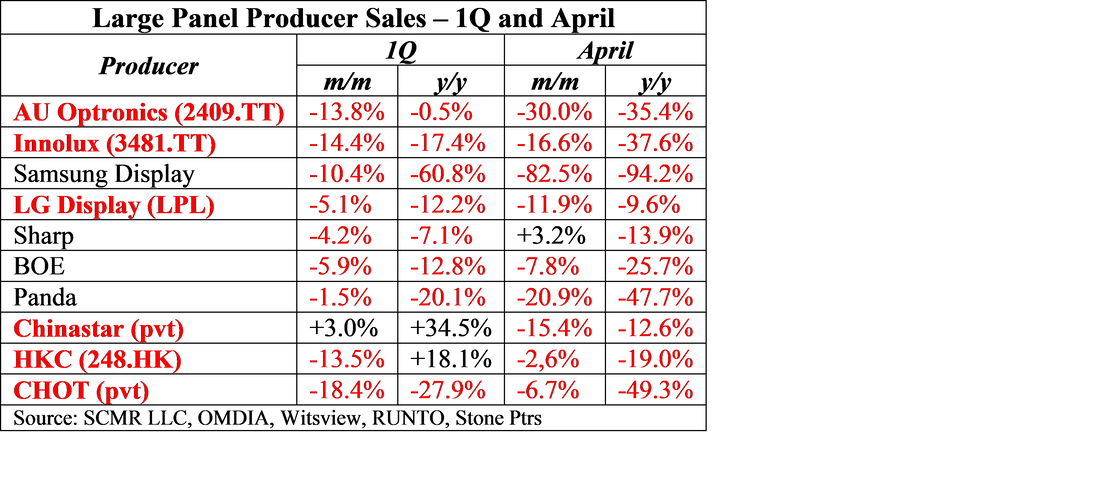

A can be seen in the tables below, TV panel prices fell far more than we expected, putting the aggregate TV panel price at the lowest point seen in the last 5 years and down 58.8% from the high reached in June of last year. Aggregate IT panel prices are now down 34.9% from the high reached in August 2021 and only 8.6% from the 5 year low seen in November 2017. April industry panel shipment data saw large panel revenue decline 13.6% m/m and is now down 25.9% y/y, with all categories showing lower shipments on y/y basis other than monitors which saw a severe shipment decline last year in 1Q and 2Q. While China’s share of overall large panel revenue increased to 51.8% in April, China’s large panel producers saw revenue decline 9.5% m/m and decline 24.1% y/y, while Japan (Sharp (6753.JP)) saw the only increase in large panel sales. We break out major large panel producers in Table 3, which shows the severity of the revenue decline in April. We note that Samsung Display (pvt) is in the process of closing its last large panel LCD fab, so the decline in that case is exaggerated and Panda (pvt) sold two of its fabs to BOE (200725.CH) last year, making the y/y comparison less relevant.

A can be seen in the tables below, TV panel prices fell far more than we expected, putting the aggregate TV panel price at the lowest point seen in the last 5 years and down 58.8% from the high reached in June of last year. Aggregate IT panel prices are now down 34.9% from the high reached in August 2021 and only 8.6% from the 5 year low seen in November 2017. April industry panel shipment data saw large panel revenue decline 13.6% m/m and is now down 25.9% y/y, with all categories showing lower shipments on y/y basis other than monitors which saw a severe shipment decline last year in 1Q and 2Q. While China’s share of overall large panel revenue increased to 51.8% in April, China’s large panel producers saw revenue decline 9.5% m/m and decline 24.1% y/y, while Japan (Sharp (6753.JP)) saw the only increase in large panel sales. We break out major large panel producers in Table 3, which shows the severity of the revenue decline in April. We note that Samsung Display (pvt) is in the process of closing its last large panel LCD fab, so the decline in that case is exaggerated and Panda (pvt) sold two of its fabs to BOE (200725.CH) last year, making the y/y comparison less relevant.

Aggregate Total Panel Pricing - 2021 - 2022 YTD - Source: SCMR LLC, OMDIA, Witsview, Stone Ptrs, Company Data

Aggregate LArge Panel Pricing & Share - 2021 - 2022 YTD - Source: SCMR LLC, OMDIA, Witsview, Stone Ptrs, Company Data

Large Panel Display Shipments - 2020 - 2022 YTD - Source: SCMR LLC, OMDIA, Witsview, RUNTO, Company Data

- Large Panel Display Revenue By Region - 2020 - 2022 YTD - Source: SCMR LLC, RUNTO, Witsview, OMDIA, Company Data

Aggregate Large/Small Panel Pricing ROC by Month - 5 Year Average - Source: SCMR LLC, OMDIA, Witsview, RUNTO

RSS Feed

RSS Feed