Panel Prices – “Elevator Out of Service”

LCD panel prices, particularly TV panel prices, have been on the rise since last May. During June and July there were rumblings that demand was slowing a bit and perhaps 3Q would not see the rapid price increases that had been seen in previous months. Some of this ‘cautionary talk’ cited component shortages, double ordering, and COVID-19 outbreaks as the root cause, but as we said in our 08/06/21 note, the rest of the industry nodded quietly during such discussions but indicates that those factors have not affected their business and expectations remain unchanged.

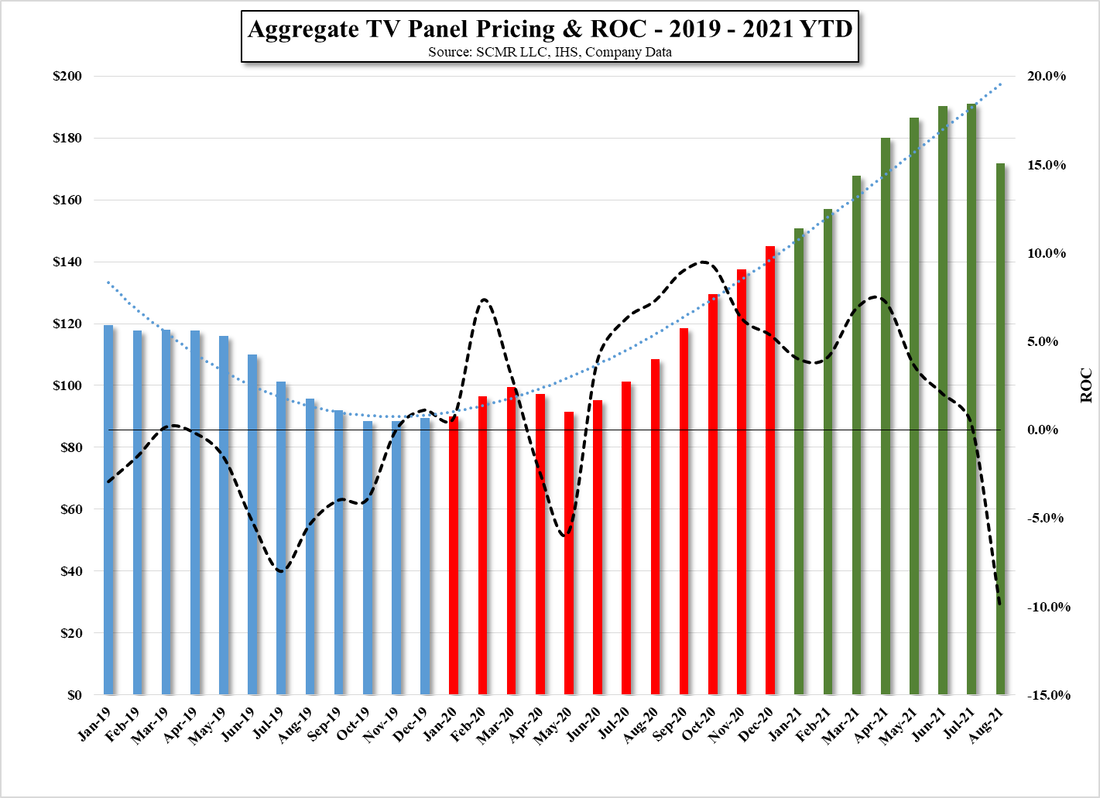

Our expectations for August were for relatively modest increases in IT product panel prices (Monitors & Notebooks), while TV panel prices were a bit more bifurcated, with the most price pressure on smaller TV panels, while demand for larger TV panels was a bit better and could see some increases, although the aggregate was down. We did note that panel producers have been shifting capacity away from TV panel production toward IT products, the leverage toward production of those panels has certainly been favorable for LCD panel producers, but at some point that leverage will work against panel producers should demand slow in that segment, more a matter of ‘when’ than ‘if’.

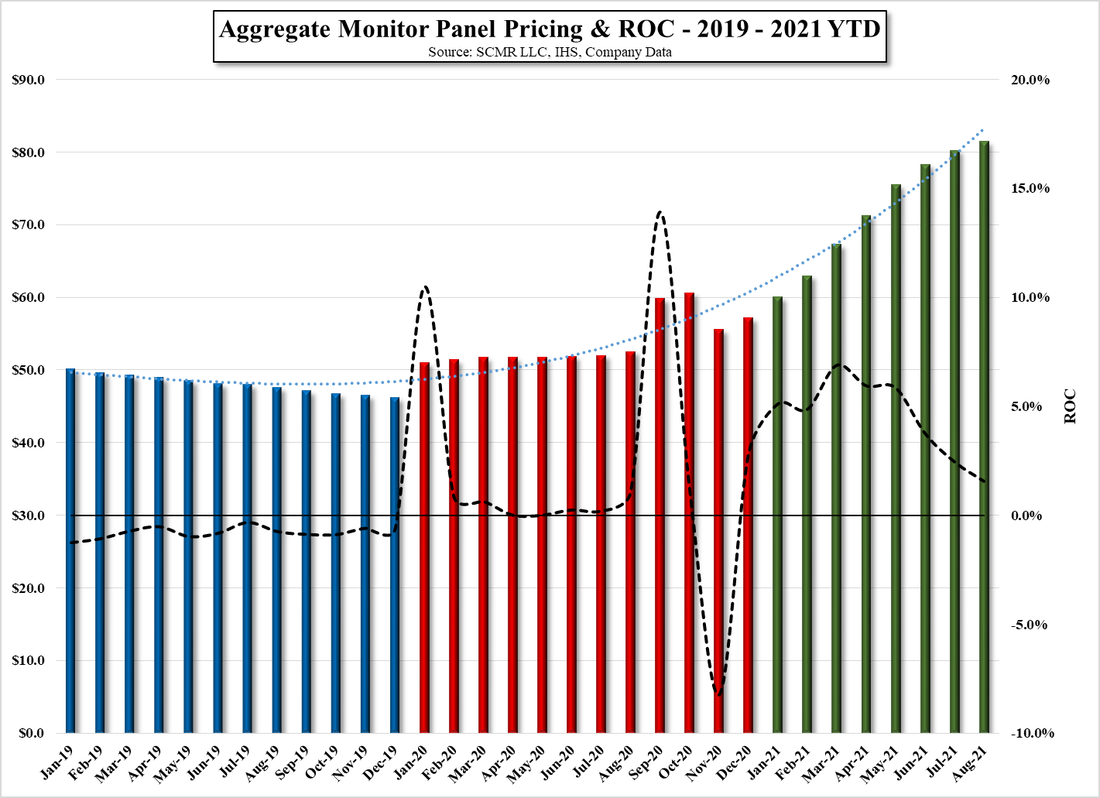

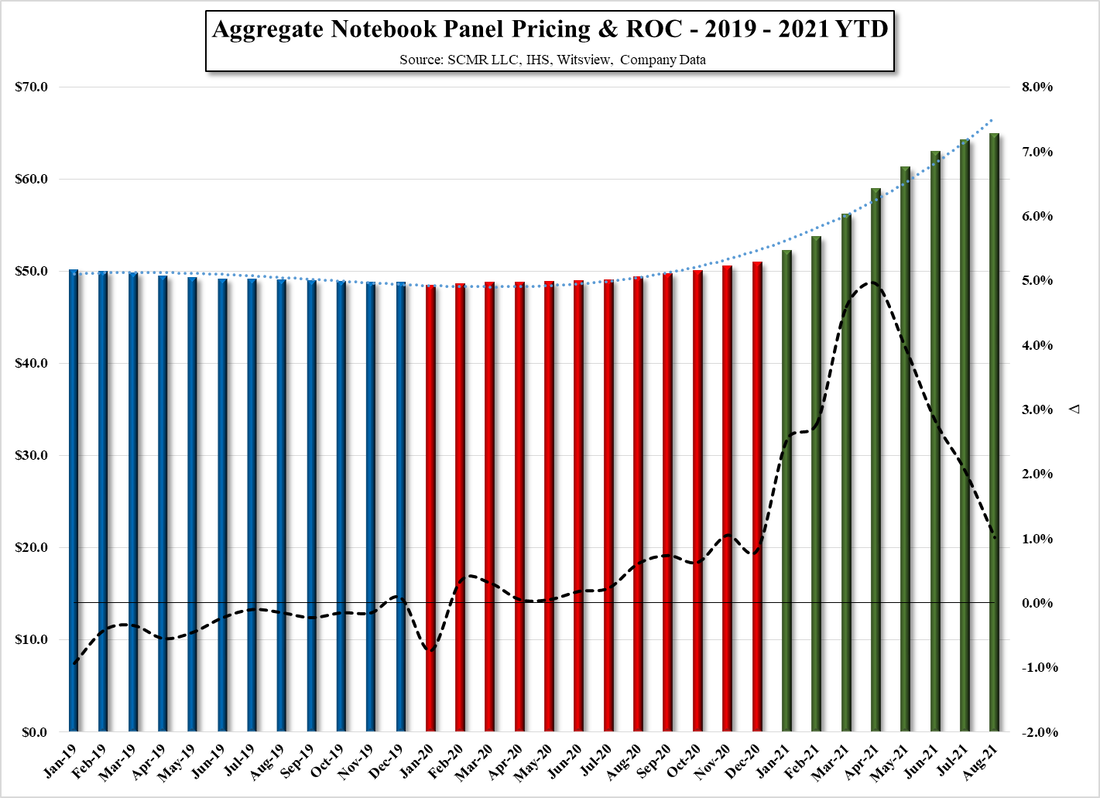

That was not the case in August for IT products, panel prices rose again, but it was the case for TV panels who saw the first aggregate TV panel price drop since May 2020, with prices down 10.1%. It is difficult to pinpoint which of the potential factors caused the greatest impact to TV panel prices, but we expect all of the contributing factors that we have mentioned in the past, including component shortages, higher logistics costs, and the realization that higher overall TV set prices would stifle consumer demand, finally became reality for TV set producers and their expectations for 3Q and the holiday season began to wither on the vine. In the case of TV panel prices, the withering was not just for smaller TV panel sizes but across the board and far greater than even our modestly pessimistic view had expected.

Our expectations for August were for relatively modest increases in IT product panel prices (Monitors & Notebooks), while TV panel prices were a bit more bifurcated, with the most price pressure on smaller TV panels, while demand for larger TV panels was a bit better and could see some increases, although the aggregate was down. We did note that panel producers have been shifting capacity away from TV panel production toward IT products, the leverage toward production of those panels has certainly been favorable for LCD panel producers, but at some point that leverage will work against panel producers should demand slow in that segment, more a matter of ‘when’ than ‘if’.

That was not the case in August for IT products, panel prices rose again, but it was the case for TV panels who saw the first aggregate TV panel price drop since May 2020, with prices down 10.1%. It is difficult to pinpoint which of the potential factors caused the greatest impact to TV panel prices, but we expect all of the contributing factors that we have mentioned in the past, including component shortages, higher logistics costs, and the realization that higher overall TV set prices would stifle consumer demand, finally became reality for TV set producers and their expectations for 3Q and the holiday season began to wither on the vine. In the case of TV panel prices, the withering was not just for smaller TV panel sizes but across the board and far greater than even our modestly pessimistic view had expected.

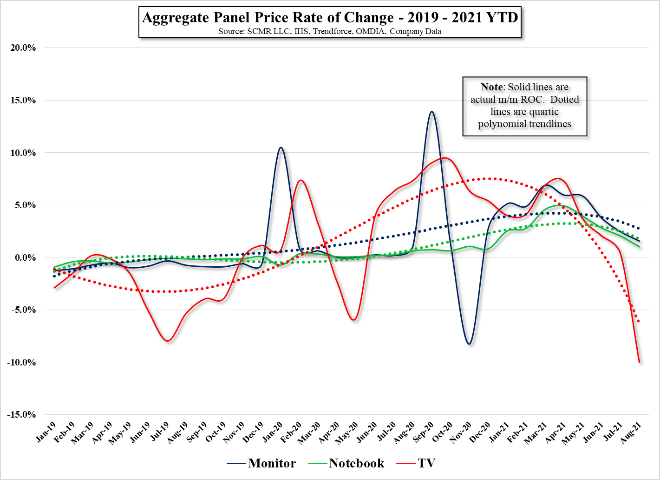

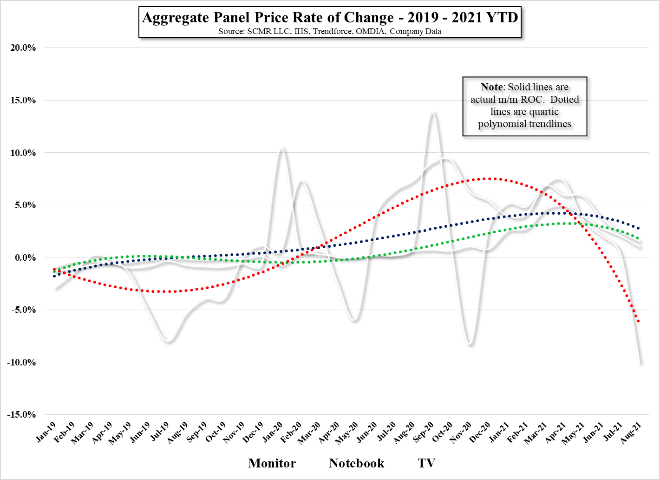

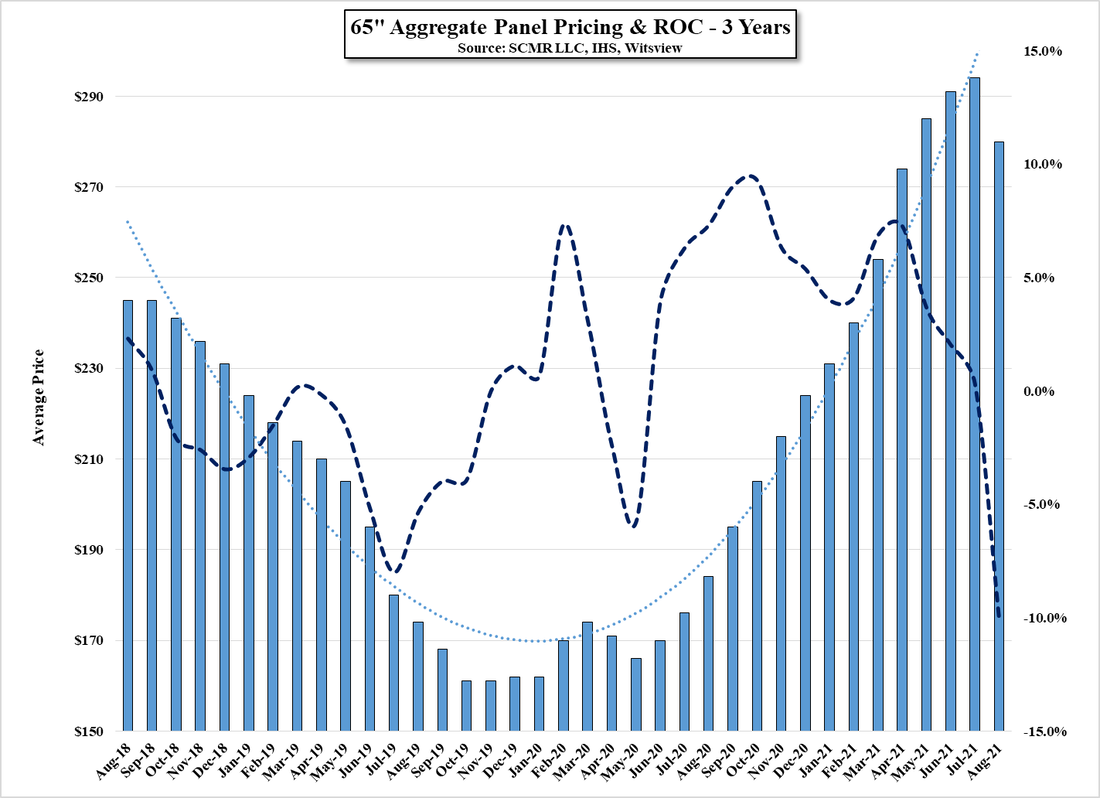

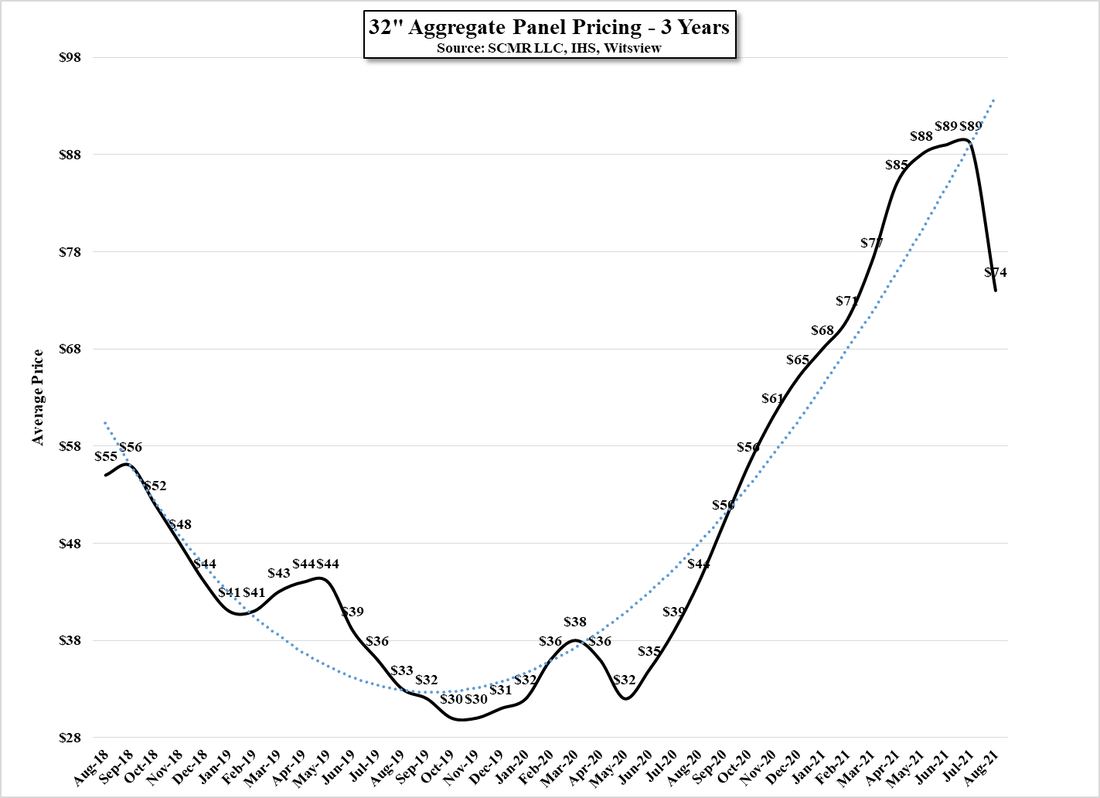

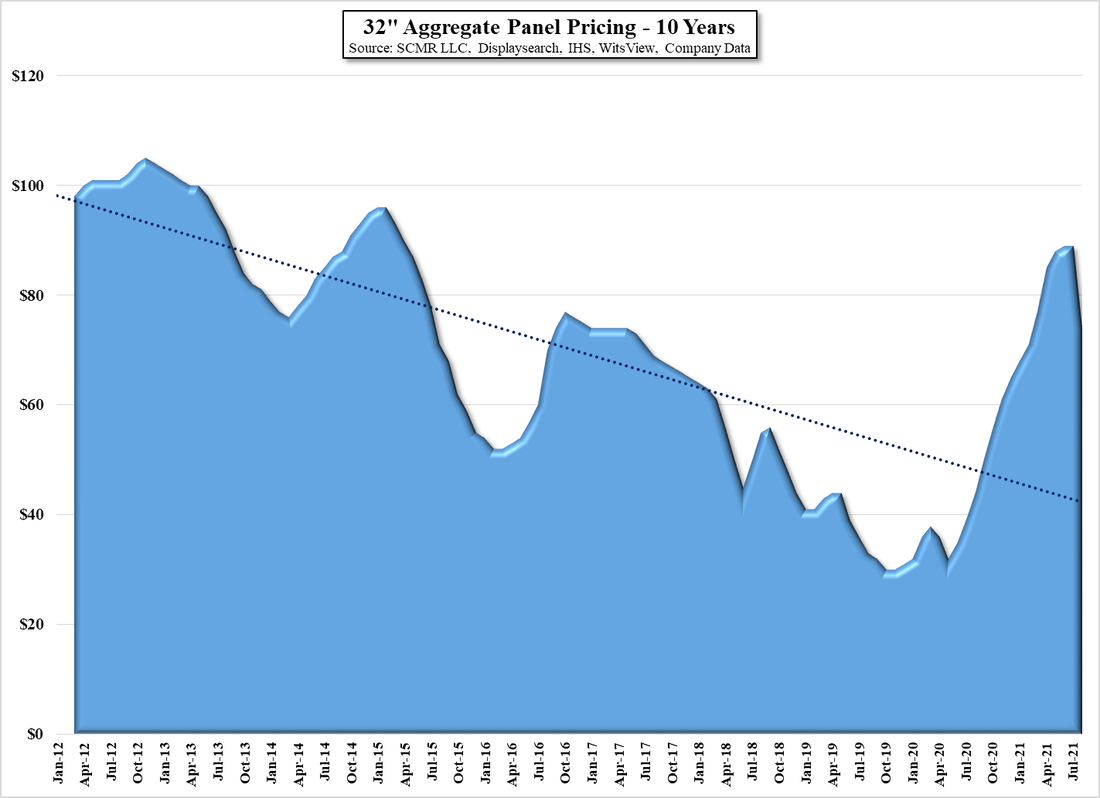

Figs. 1 – 3 show aggregate panel prices for the three major categories, while we show the ROC for those categories in Fig. 4 & 5, with the actual prices removed in Fig. 5, leaving only the trend lines. To better show how severe the price drop was for TV panels, we have included both Fig. 6 & Fig. 7, which show 65” (large) and 32” (small) TV panel pricing for additional clarity, but we also point out that even after the -10.1% drop in aggregate TV panel prices, they are still up 86.96% over the aggregate price in May 2020, the last month where TV panel prices saw declines, so while the drop in August was significant, Fig. 8 shows that over the long-term 32” (and most other) panel prices have been declining, which leaves a big opening as to where TV panel prices will bottom out and more importantly, the effect falling TV panel prices will have on panel producer profitability going forward. It’s a bit early to forecast September panel pricing, but we are keeping our expectations low for all categories and see little reason for anything more than a situation similar to August thus far.

Aggregate Monitor Panel Pricing & ROC - 2019 - 2021 YTD - Source: SCMR LLC, IHS, Company Data

Aggregate Notebook Panel Pricing & ROC - 2019 - 2021 YTD - Source: SCMR LLC, IHS, Witsview, Company Data

Aggregate TV Panel Pricing & ROC - 2019 - 2021 YTD - Source: SCMR LLC, IHS, Witsview, Company Data

Figure 4 & 5 - Aggregate Panel Price ROC - 2019 - 2021 YTD - Source: SCMR LLC, IHS, Trendforce, OMDIA, Company Data

65" Aggregate Panel Prices & ROC - 3 Years - Source: SCMR LLC, IHS, Witsview, Company Data

32" Aggregate Panel Pricing - 3 Years - Source: SCMR LLC, IHS, Witsview, Company Data

32" Aggregate Panel Pricing - 10 Years - Source: SCMR LLC, Displaysearch, IHS, Witsview, Company Data

RSS Feed

RSS Feed