SMIC & Samsung

Not to be left out of the semiconductor industry’s rush to add capacity that we have been witnessing for the last 6 months, China’s largest foundry SMIC (688981.CH) has signed a Cooperation Framework with the government of Shanghai to build a 12” foundry line that will operate at 28nm and larger nodes. The project is expected to cost $8.87b US with SMIC contributing at least 51% of the capital and the Shanghai government no more than 25%. The balance will be raised from 3rd party investors. There is no start date on the project as this is just a framework rather than a completed agreement, but we assume that the Shanghai government has made inquiries about potential 3rd party investors and is confident that they will be able to raise the additional capital necessary.

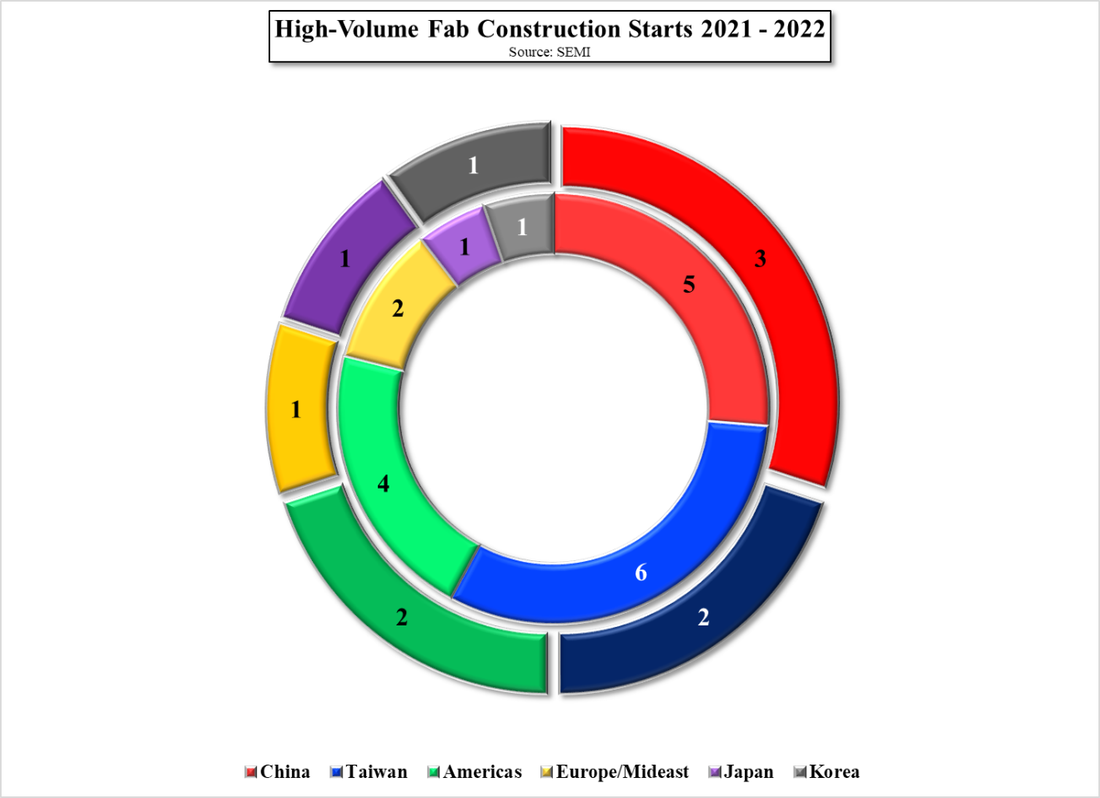

At the end of June, according to SEMI, 19 high volume fabs will have started new construction before the end of the year and another 10 in 2022. 15 of the 29 fabs (excluding SMIC) will be foundries, with the largest producing ~220,000 wpm (200mm equivalents). 22 of the 29 fabs will be 300mm lines, with the rest between 100mm and 200mm. The combined output of the 29 fabs is expected to be ~2.6m wafers/month[1] and spending for 300mm fabs in 2022 is expected to reach $17b, an all-time high, but will outpace 300mm wafer production if no additional wafer capacity is announced this year. Hopefully new chip production capacity will not outpace demand in 2023 – 2024, but if wafer capacity expansion does not match capacity, it will be a moot point.

[1] 200mm equivalents

At the end of June, according to SEMI, 19 high volume fabs will have started new construction before the end of the year and another 10 in 2022. 15 of the 29 fabs (excluding SMIC) will be foundries, with the largest producing ~220,000 wpm (200mm equivalents). 22 of the 29 fabs will be 300mm lines, with the rest between 100mm and 200mm. The combined output of the 29 fabs is expected to be ~2.6m wafers/month[1] and spending for 300mm fabs in 2022 is expected to reach $17b, an all-time high, but will outpace 300mm wafer production if no additional wafer capacity is announced this year. Hopefully new chip production capacity will not outpace demand in 2023 – 2024, but if wafer capacity expansion does not match capacity, it will be a moot point.

[1] 200mm equivalents

And while we are on the subject, documents have revealed that the city of Taylor, Texas, about 25 miles from where Samsung Electronics (005930.KS) has its only semiconductor production fab in the US, has offered the company some very attractive tax breaks to establish its new $17b fab in their quaint town. Taylor, a town of almost 16,300 residents, has been the site of a number of famous and infamous movies and TV shows including Varsity Blues, Friday Night Lights, and The Texas Chain Saw Massacre, and such notables as Tex Avery, animator and creator of Daffy Duck and Droopy, and actor Rip Torn, and while the town does have a crime rate a bit above the US average, one of the town’s biggest problems is the annual migration of the Cattle Egret, a heron that is noisy can damage vegetation.

Cattle Egret - Source: All About Birds

Competing with Austin, the state capital and city of just under 1m, can be daunting but with Taylor offering Samsung a grant of 92.5% of assessed property tax for 10 years, 90% for the next 10, and 85% for the last 10, and that same 92.5% waiver on any new property built on the site, along with the repayment of any development review costs, and a 1,188 acre site (the existing Samsung site in Austin is 250 acres plus 350 that Samsung recently purchased). If Taylor were to win the Samsung semiconductor fab bake-off, which also includes sites in Arizona and New York, it would create ~1,800 new jobs with construction starting in 1Q 2022 and production in 2024.

RSS Feed

RSS Feed