Supply/Demand

As we noted yesterday there are a number of demand scenarios that could occur this year with COVID-19 the driving force that will determine the outcome. The supply side in 2021 however is a 2nd order function as capacity additions and subtractions will be based on demand, which is based on COVID-19 outcomes. While this complicates things a bit, in reality the large panel capacity outlook this year is determined by producers in two regions, South Korea and China, given their combined share of the large panel display market (area) was 79.1% last year.

Before COVID-19 became global large panel prices had been in decline, and both Samsung Display (pvt) and LG Display (LPL) the two large panel producers in South Korea, had been making plans to reduce or completely end large panel LCD production. Not only was this a function of large panel pricing which put many panel producers in loss mode, but was also a function of the increasing competition from Chinese Large Panel LCD producers, who had been adding capacity for a number of years and through construction and operating subsidies, were able to produce commodity LCD panels competitively.

As the COVID-19 pandemic both reduced worker availability and increased demand for certain large panel products, the large panel market tightened and panel producers began to see profitability. This changed their outlook, and Chinese capacity expansion plans that had been put on hold began again. At the same time, both Samsung and LG reevaluated their plans for reducing their large panel LCD capacity, given a more profitable outlook, and most of those plans, which would have been implemented at or near the end of last year have been postponed.

Postponed might not be the proper word here, as we suspect both Samsung and LG will reinstitute those large panel LCD capacity reduction plans at the first sign of a change in large panel price direction, given that the competition from China remains the same or has increased, so while speculation that such plans by Korean large panel LCD producers have been extended through 2021, we believe those plans could change in a heartbeat. At this poi9nt in the year we have little choice but to make certain capacity assumptions for all producers based on current circumstances, but as we did on the demand side, there are a number of possible scenarios for capacity, based on the global COVID-19 pandemic and how it has and could continue to change our lifestyle. Rather than do what would be some very complex calculations, we have chosen to lock in a capacity scenario at this time in order to plot the industry outcome against the scenarios we created previously. Hopefully we will be able to set up an ‘if…then’ set for all 16 possible supply/demand scenarios at a later date, but for now we use the capacity data indicated below.

Before COVID-19 became global large panel prices had been in decline, and both Samsung Display (pvt) and LG Display (LPL) the two large panel producers in South Korea, had been making plans to reduce or completely end large panel LCD production. Not only was this a function of large panel pricing which put many panel producers in loss mode, but was also a function of the increasing competition from Chinese Large Panel LCD producers, who had been adding capacity for a number of years and through construction and operating subsidies, were able to produce commodity LCD panels competitively.

As the COVID-19 pandemic both reduced worker availability and increased demand for certain large panel products, the large panel market tightened and panel producers began to see profitability. This changed their outlook, and Chinese capacity expansion plans that had been put on hold began again. At the same time, both Samsung and LG reevaluated their plans for reducing their large panel LCD capacity, given a more profitable outlook, and most of those plans, which would have been implemented at or near the end of last year have been postponed.

Postponed might not be the proper word here, as we suspect both Samsung and LG will reinstitute those large panel LCD capacity reduction plans at the first sign of a change in large panel price direction, given that the competition from China remains the same or has increased, so while speculation that such plans by Korean large panel LCD producers have been extended through 2021, we believe those plans could change in a heartbeat. At this poi9nt in the year we have little choice but to make certain capacity assumptions for all producers based on current circumstances, but as we did on the demand side, there are a number of possible scenarios for capacity, based on the global COVID-19 pandemic and how it has and could continue to change our lifestyle. Rather than do what would be some very complex calculations, we have chosen to lock in a capacity scenario at this time in order to plot the industry outcome against the scenarios we created previously. Hopefully we will be able to set up an ‘if…then’ set for all 16 possible supply/demand scenarios at a later date, but for now we use the capacity data indicated below.

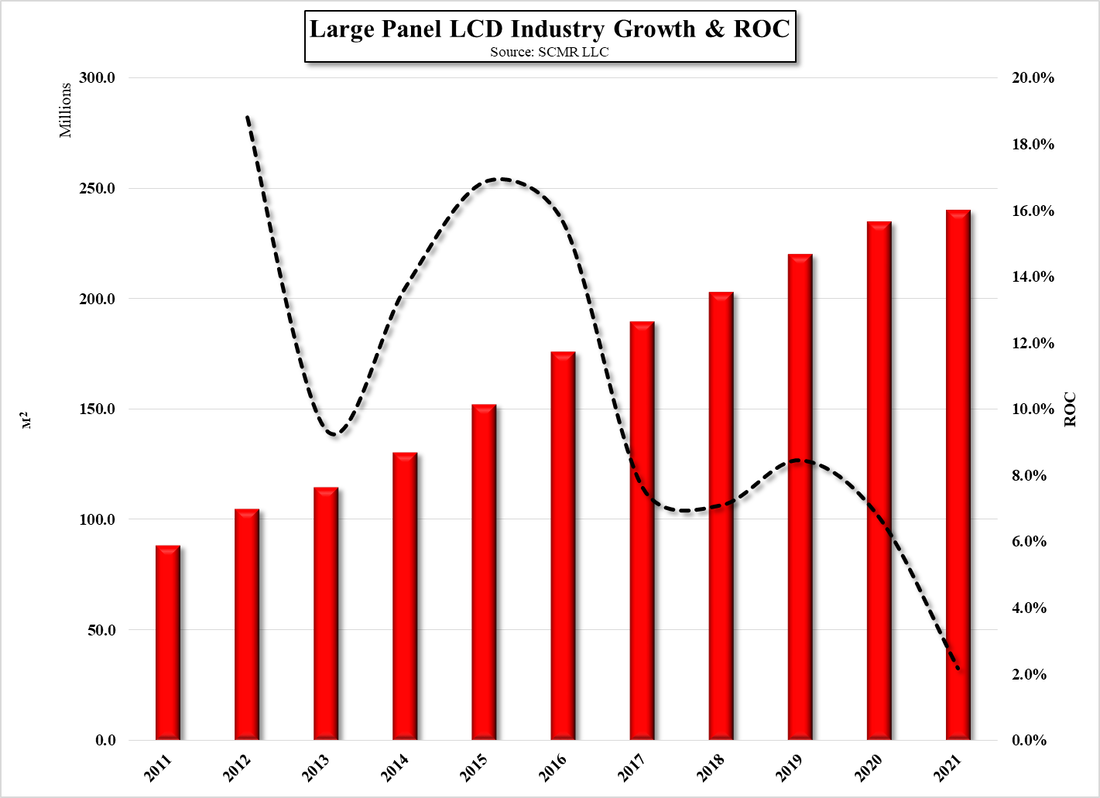

Large Panel Industry Growth & ROC - Source: SCMR LLC

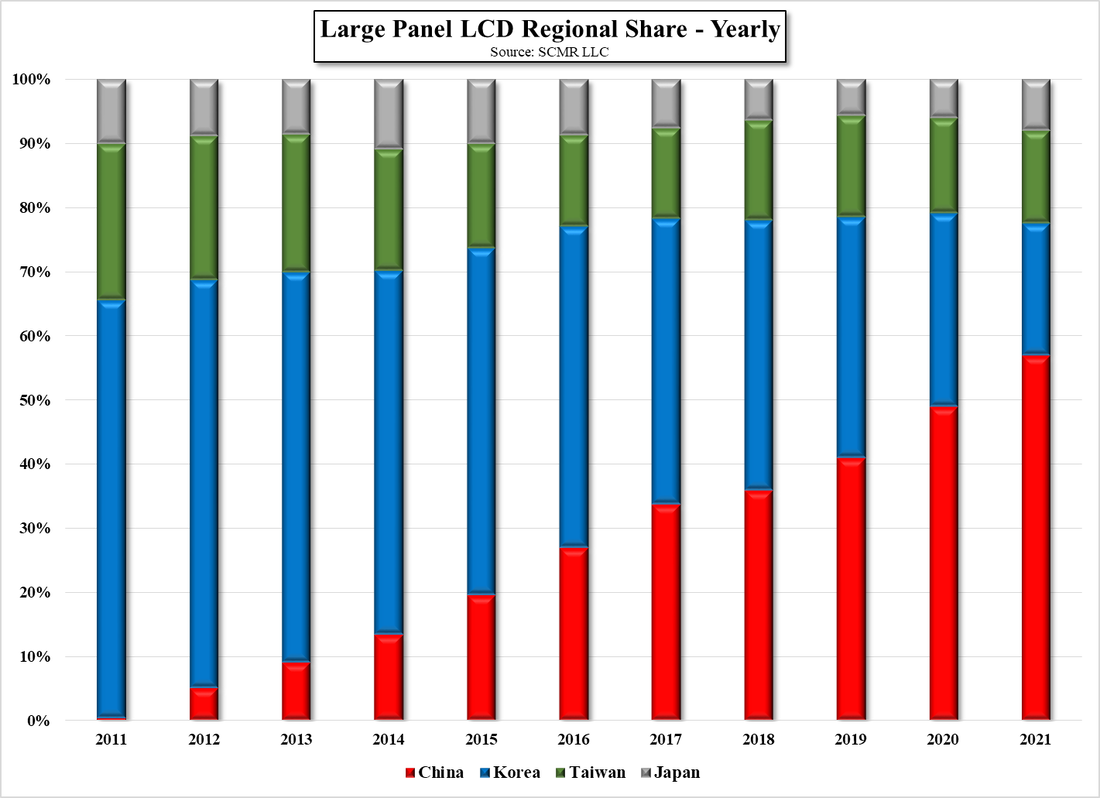

Large Panel LCD Regional Share - Yearly - Source: SCMR LLC

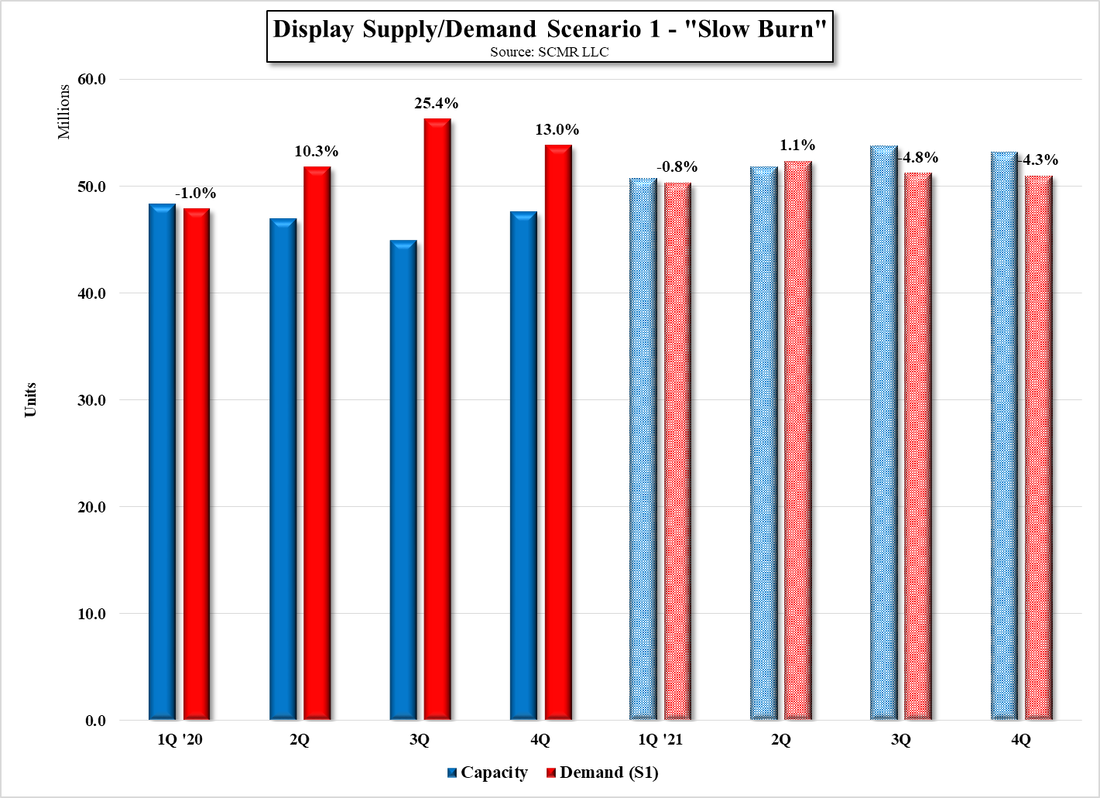

For each of the demand scenarios we mapped out yesterday, we show how that demand will match up with large panel LCD capacity this year, along with the static results from 2020 for comparison.

In the “Slow Burn” scenario, after a year (2020) where demand outstripped supply in three of four quarters, oversupply levels off and at its worst sees ~4.3% of yielded overcapacity, which would likely see panel prices stable or declining. Again we note that each of these demand is plotted against t same supply model.

In the “Slow Burn” scenario, after a year (2020) where demand outstripped supply in three of four quarters, oversupply levels off and at its worst sees ~4.3% of yielded overcapacity, which would likely see panel prices stable or declining. Again we note that each of these demand is plotted against t same supply model.

Display Supply/Demand Scenario 1 - "Slow Burn" - Source: SCMR LLC

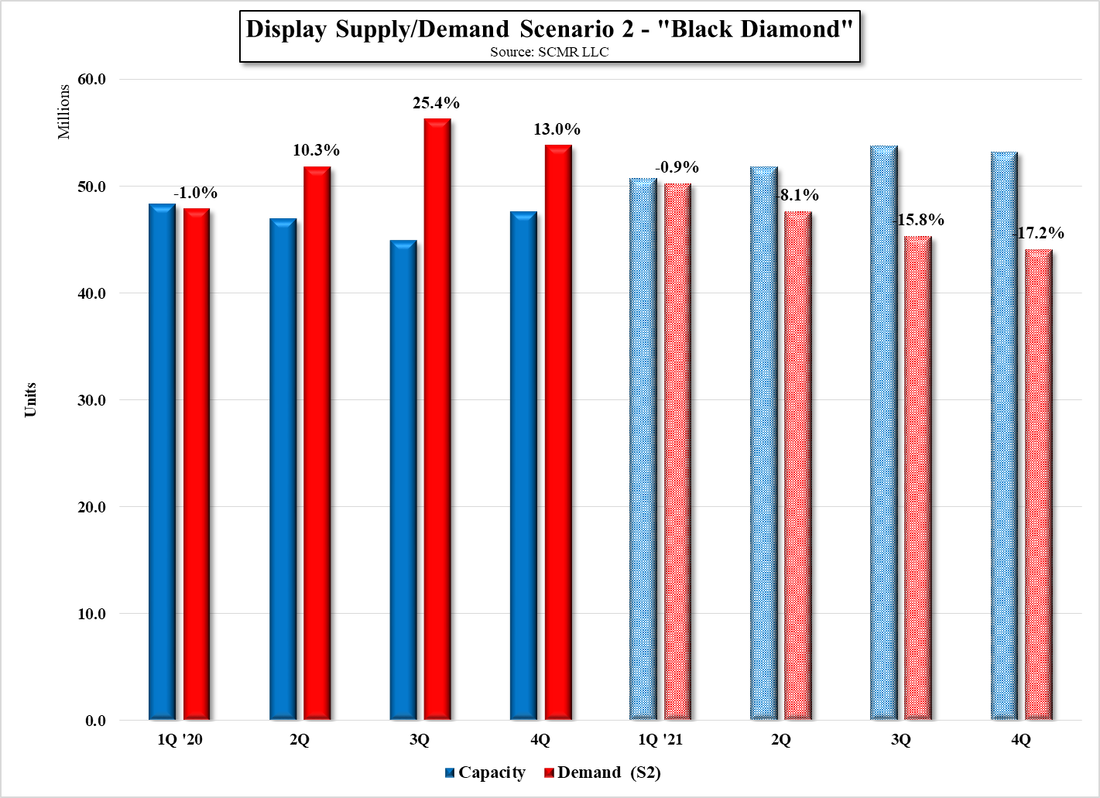

In the more draconian “Black Diamond” scenario, the oversupply worsens as the year progresses, leading to what would likely be a rapid decline in large panel prices in 2H ’21. We note however that our assumptions on yield are also static in each scenario, which would mean that even in an overcapacity situation, panel producers continue to run at high utilization rates, which while it might happen for a short period of time, would likely not continue to be the case if panel prices began to fall rapidly. That said, there could still be room for panel producer profitability as panel prices decline, given the steep rise they have taken over the last few months, but we expect if the “Black Diamond” scenario were to take place panel producers would begin to reduce utilization at the end of 2Q.

Display Supply/Demand Scenario 2 - "Black Diamond" - Source: SCMR LLC

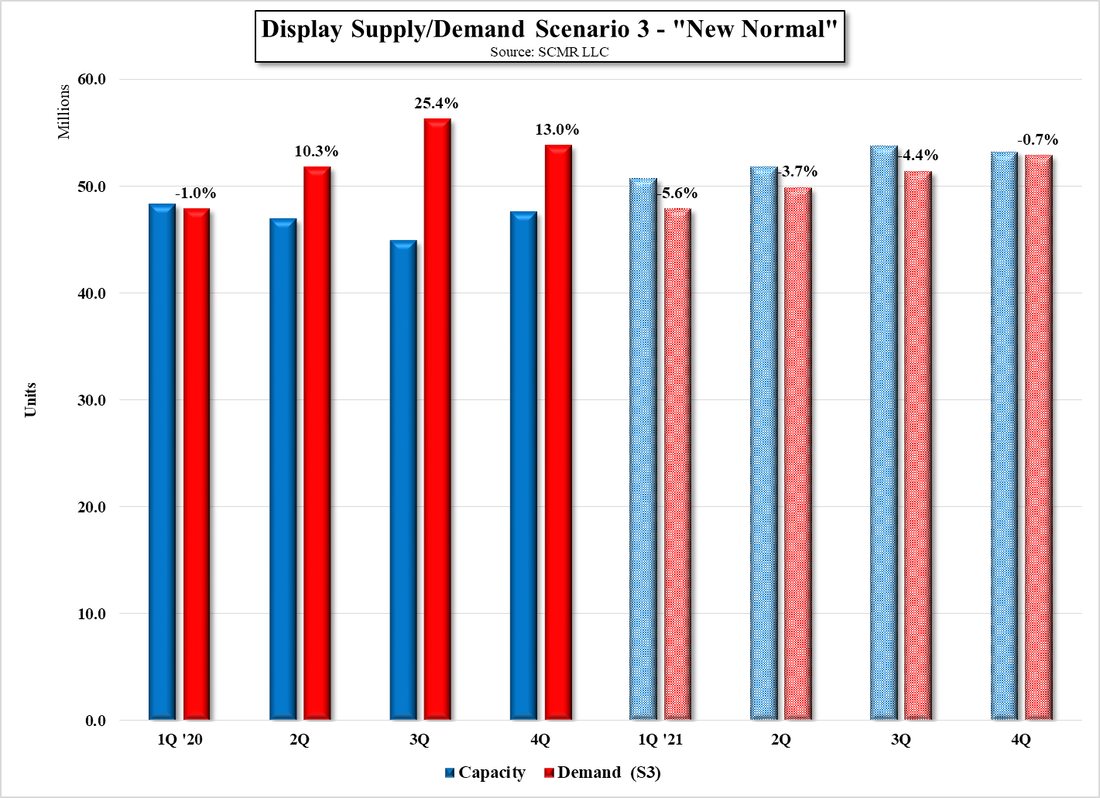

In the “New Normal” scenario, as we noted yesterday, demand increases and along with that panel producer optimism toward capacity expansion plans also increases. While there is a slight bit of yielded overcapacity even in this scenario, much will depend on plans at Samsung and LG toward their large panel LCD capacity, given they would likely continue to produce at current levels for the year. If either makes the more long-term decision to wind down capacity further, even this small amount of large panel LCD overcapacity could evaporate quickly and tighten the market, raising panel prices further.

Display Supply/Demand Scenario 3 - "New Normal" - Source: SCMR LLC

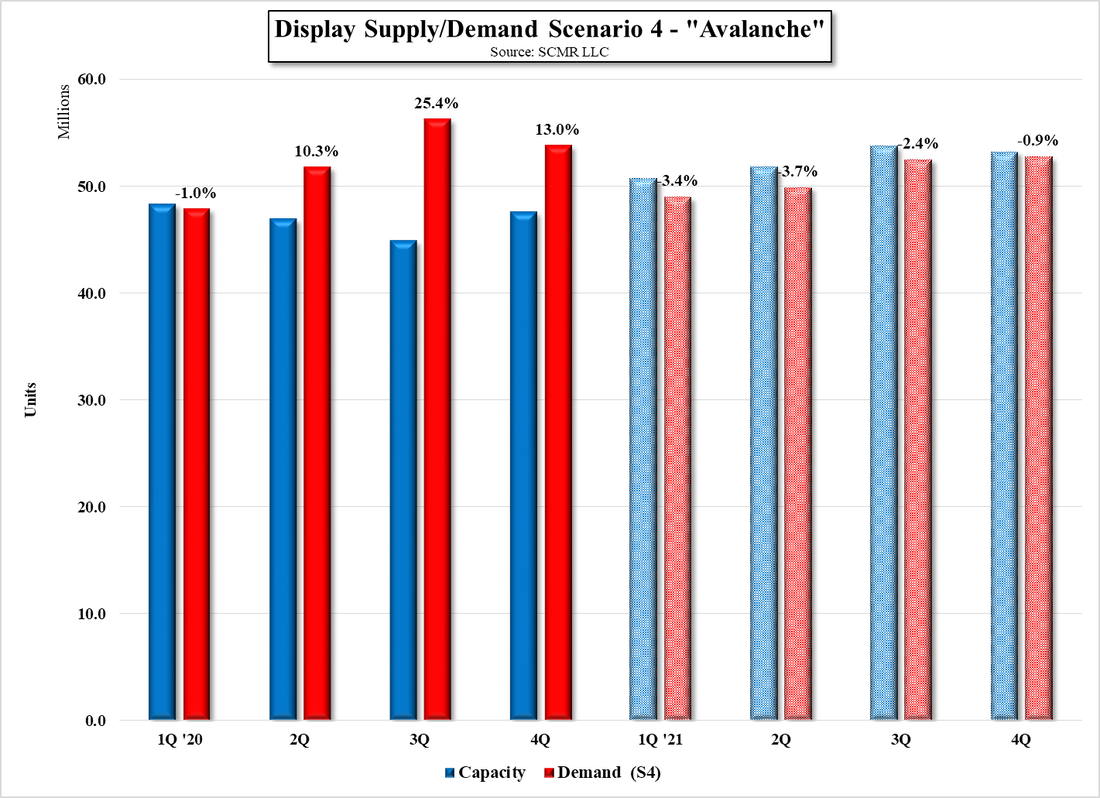

In the “Avalanche” scenario, even with the quick drop off in demand seen in yesterday’s charts, producers continue their optimistic view toward capacity expansion and modest yielded oversupply continues, keeping panel prices relatively stable throughout the year.

Display Supply/Demand Scenario 4 - "Avalanche" - Source: SCMR LLC

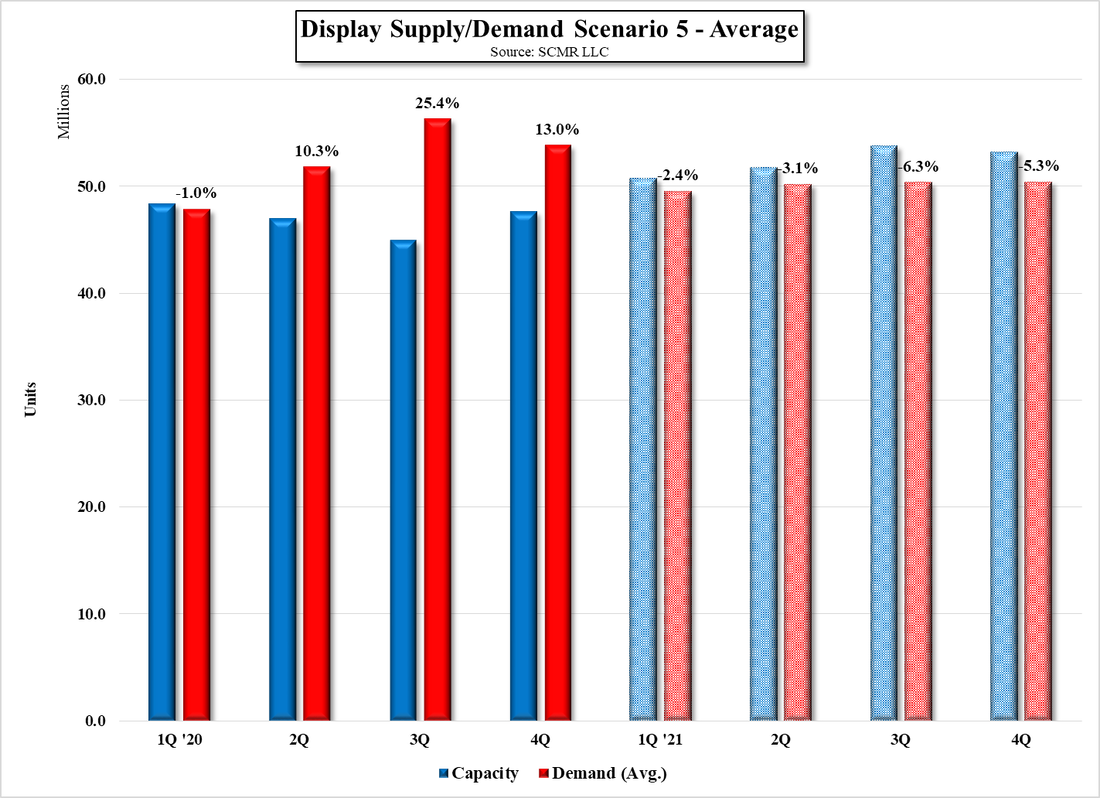

Lastly we look at the “Average” of all the scenarios, where there is moderate overcapacity for the 2nd half of the year. While we do not count the average as a scenario, it does smooth the variations in the more specific demand scenarios and represents a middle ground for those that do not see the extremes this year.

Display Supply/Demand Scenario 5 - Average - Source: SCMR LLC

All in, we note that there is one factor that could change both sides of the large panel LCD supply/demand equation and that is the consumer and device elasticity. We have seen some consumer level price increases as panel prices have increased, but as lower cost panel inventory is depleted overall device prices will continue to rise. There is certainly a lag between when panel prices rise and consumer device prices rise as brands are willing to work against lower margins until they reach a pain point. We expect that in some of the scenarios, particularly where yielded capacity remains tight, continuing price increases will begin to have a more onerous effect in 2H, particularly in the TV set space, but it is only one factor along with a host of others that could affect panel and device prices this year. Each month we will update both supply and demand models with actual data to see which of the scenarios are closest to reality.

RSS Feed

RSS Feed