Taiwan Panel Sales & Shipments

As we have noted in the past, while Taiwan represents ~27.4% (Fe. ‘22) of large panel display industry revenue, the three Taiwanese panel producers are required to report monthly sales figures while panel producers in other regions and countries typically report those figures quarterly. This gives a bit of granularity to shorter-term trends in the display space and justifies tracking those results. As February is an unusual month for the display space given that it is a short month and also contains the Chinese New Year holiday, March tends to even the quarter out, making it a bit more comparable to other years. Such is the case this year, although the total quarterly result is a bit less positive than last year.

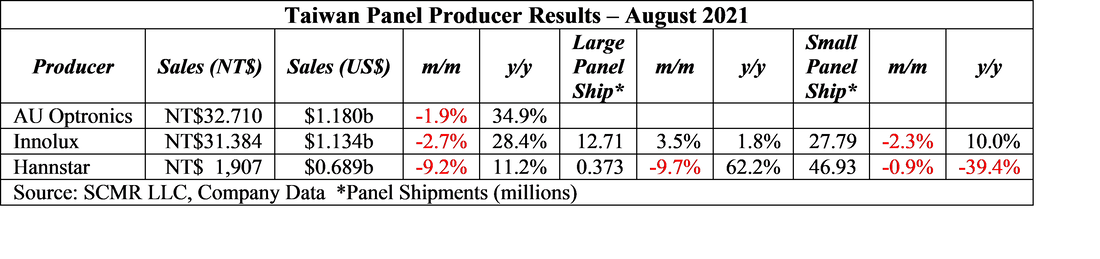

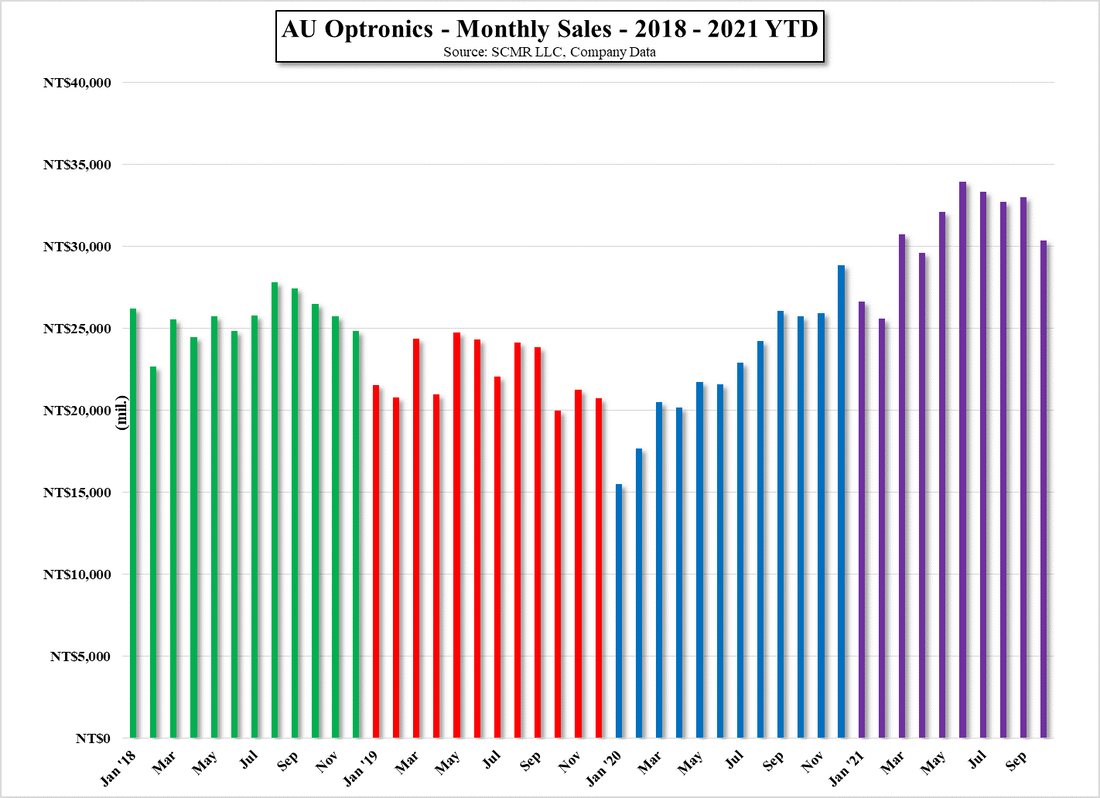

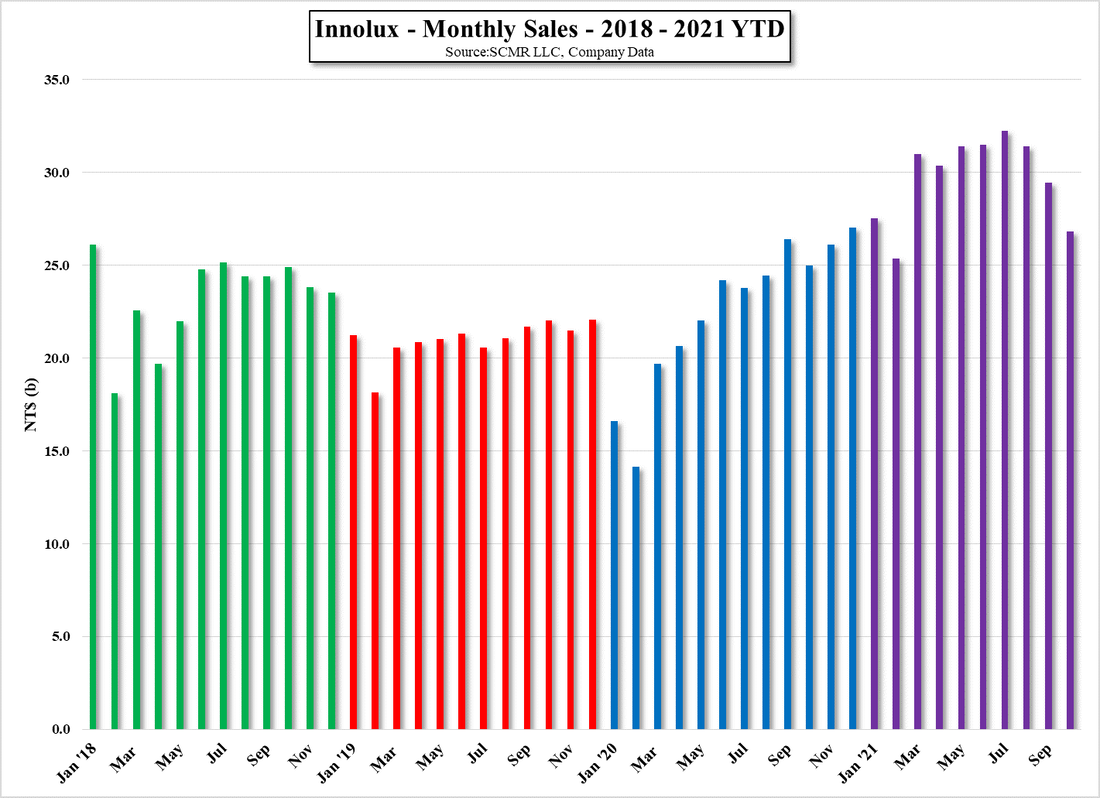

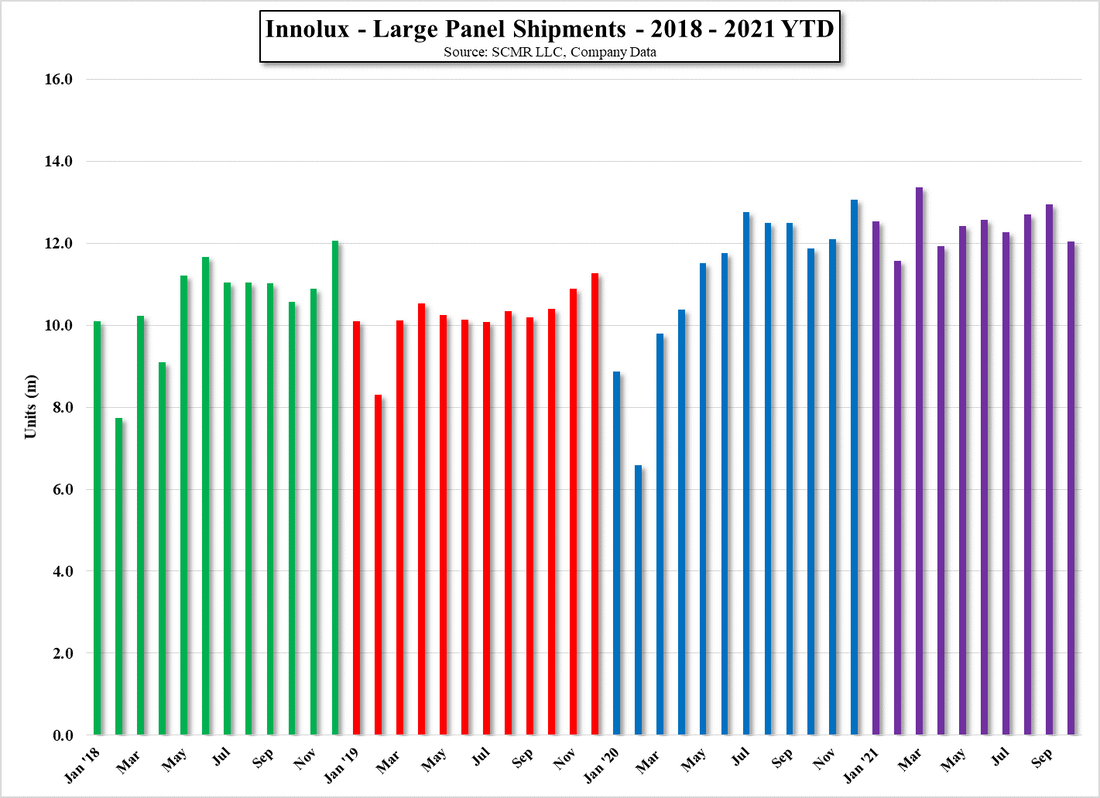

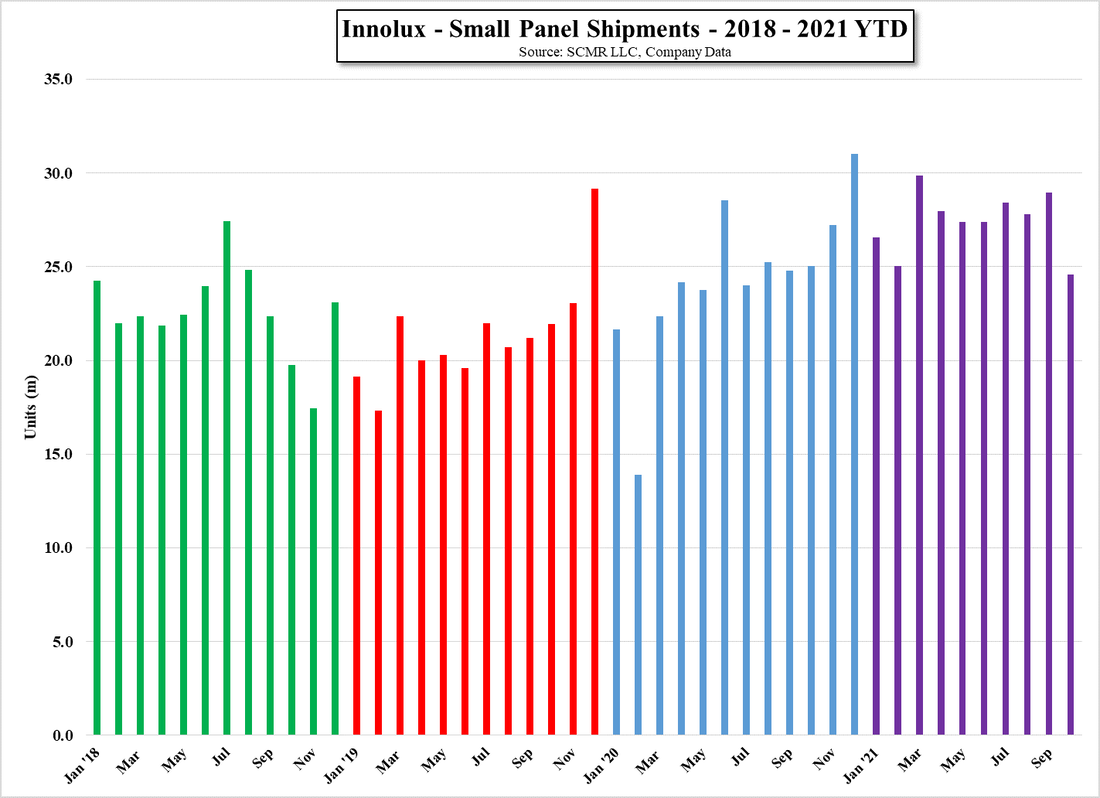

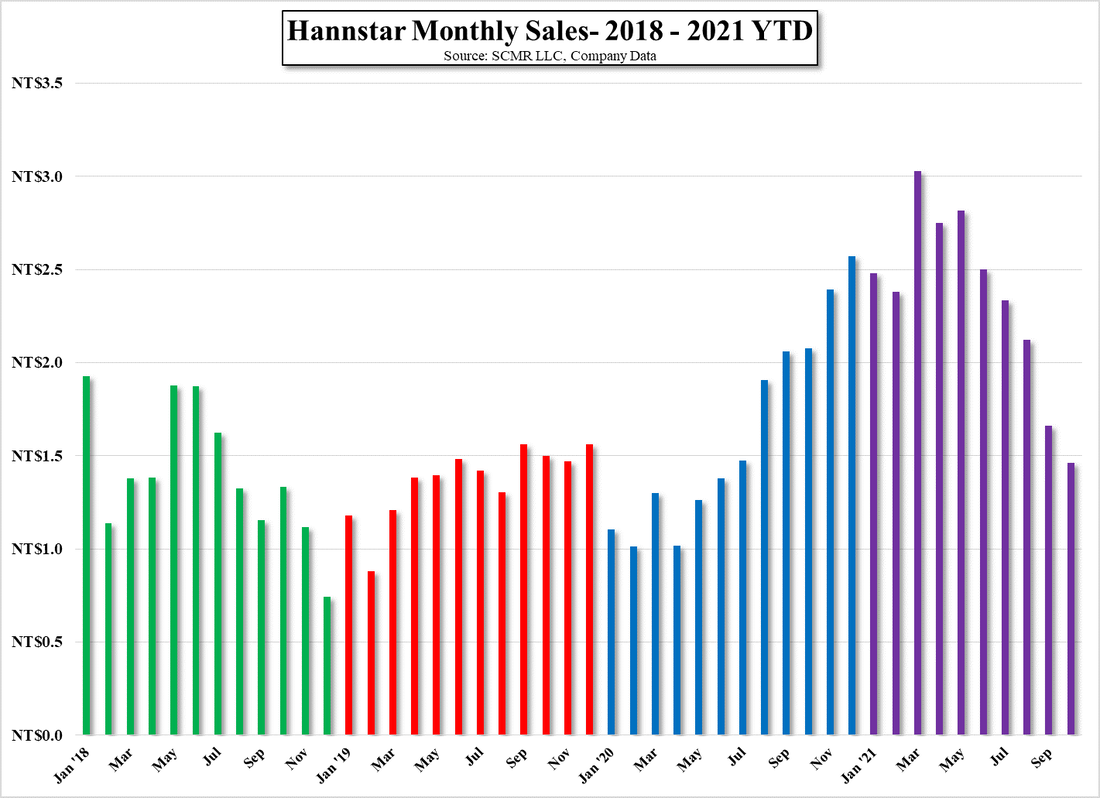

AU Optronics (2409.TT) reported March sales of NT$28043 ($829m US), up 9.3% m/m but down 8.7% y/y, while Innolux (3481.TT) posted sales of NT$23.92b ($825.74m US), up 9.0% m/m but down 22.8% y/y, while Hannstar (61116.TT) generated sales of NT$1.74b ($59.57m US), up17.4% m/m but down 42.6% y/y. While the m/m performance looks strong, as we noted, March tends to be a recovery month for panel producers after a slow January and February, however, in the table below, we also show the 5 year averages for March m/m and y/y, which indicate that the gains seen this March are below the averages, particularly when comparing y/y metrics.

Preliminary quarterly sales results, as shown in Table 2, paint a similar picture, although not quite as negative, with the 1Q results being a bit closer to 5 year q/q averages, while 1Q y/y results are a bit further from the averages. The charts below show that 2022 is starting out more similar to 2018 – 2019, which makes sense given 2020 was certainly not a typical year, nor was 2021, but based on the sales data thus far for the three Taiwan based panel producers, it looks like 2022 will be a more typical year than the last two, but at a higher sales level than 2018 – 2019. This would be a good indicator of full year panel producer results, however we expect TV panel pricing to remain relatively flat for 2Q and IT panel prices to decline further, which would pull down full year sales and make the 2022 full year chart look a bit less typical than it does thus far.

All in, the best case in our view would be a typically seasonal 2022 for panel sales, at a higher level than 2018 – 2019, but a lower one than the ‘COVID-19 years’ of 2020 and 2021. The worst case would be a rapid decline in IT panel prices with no increase in TV (large) panel prices, which would set up potential q/q declines during what should be sequentially better quarters. Y/y results will likely be down in 2Q and possibly 3Q as last year’s large panel price decline began late in the year. While not a disastrous year for panel producers 2022 is shaping up to be far more difficult than last year and we expect valuations to continue to remain constrained for most generic panel producers.

AU Optronics (2409.TT) reported March sales of NT$28043 ($829m US), up 9.3% m/m but down 8.7% y/y, while Innolux (3481.TT) posted sales of NT$23.92b ($825.74m US), up 9.0% m/m but down 22.8% y/y, while Hannstar (61116.TT) generated sales of NT$1.74b ($59.57m US), up17.4% m/m but down 42.6% y/y. While the m/m performance looks strong, as we noted, March tends to be a recovery month for panel producers after a slow January and February, however, in the table below, we also show the 5 year averages for March m/m and y/y, which indicate that the gains seen this March are below the averages, particularly when comparing y/y metrics.

Preliminary quarterly sales results, as shown in Table 2, paint a similar picture, although not quite as negative, with the 1Q results being a bit closer to 5 year q/q averages, while 1Q y/y results are a bit further from the averages. The charts below show that 2022 is starting out more similar to 2018 – 2019, which makes sense given 2020 was certainly not a typical year, nor was 2021, but based on the sales data thus far for the three Taiwan based panel producers, it looks like 2022 will be a more typical year than the last two, but at a higher sales level than 2018 – 2019. This would be a good indicator of full year panel producer results, however we expect TV panel pricing to remain relatively flat for 2Q and IT panel prices to decline further, which would pull down full year sales and make the 2022 full year chart look a bit less typical than it does thus far.

All in, the best case in our view would be a typically seasonal 2022 for panel sales, at a higher level than 2018 – 2019, but a lower one than the ‘COVID-19 years’ of 2020 and 2021. The worst case would be a rapid decline in IT panel prices with no increase in TV (large) panel prices, which would set up potential q/q declines during what should be sequentially better quarters. Y/y results will likely be down in 2Q and possibly 3Q as last year’s large panel price decline began late in the year. While not a disastrous year for panel producers 2022 is shaping up to be far more difficult than last year and we expect valuations to continue to remain constrained for most generic panel producers.

Au Optronics - Monthly Sales - 2018 - 2022 YTD - Source: SCMR LLC, Company Data

- Innolux - Monthly Sales - 2018 - 2022 YTD - Source: SCMR LLC, Company Data

- Innolux - Large & Small Panel Shipments - 2018 - 2022 YTD - Source: SCMR LLC, Company Data

Hannstar Monthly Sales - 2018 - 2022 YTD - Source: SCMR LLC, Company Data

Hannstar Monthly Large & Small Panel Shipments - 2018 - 2022 YTD - Source: SCMR LLC, Company Data

RSS Feed

RSS Feed