2026 TV Market Price Reveal: Strategic Divergence Explored

The Timing of the "Price Reveal"

New TV models from major brands are typically announced at the Consumer Electronics Show in early January, but pricing is not usually revealed until March or April, right around when they become available for pre-order. There are a number of reasons why TV set brands hesitate to reveal prices early in the new year, some of which are fiscal and some psychological.

The “Price Reveal” pulls the curtain away from the hype that surrounds the new models early in the year and adds a sense of reality that allows the consumer to make a judgement as to whether the propaganda is worth the money. In fact, almost all brands have revealed 2026 TV set prices, with only Samsung Electronics (005930.KS) the holdout at this point in the year. That said, LG Electronics (066570.KS), who revealed the pricing for much of their flagship and mid-tier TV sets recently, is holding back the pricing on their budget tier sets, likely until they get an understanding of Samsung’s pricing.

LG’s Premium Strategy: Holding the Line on OLED

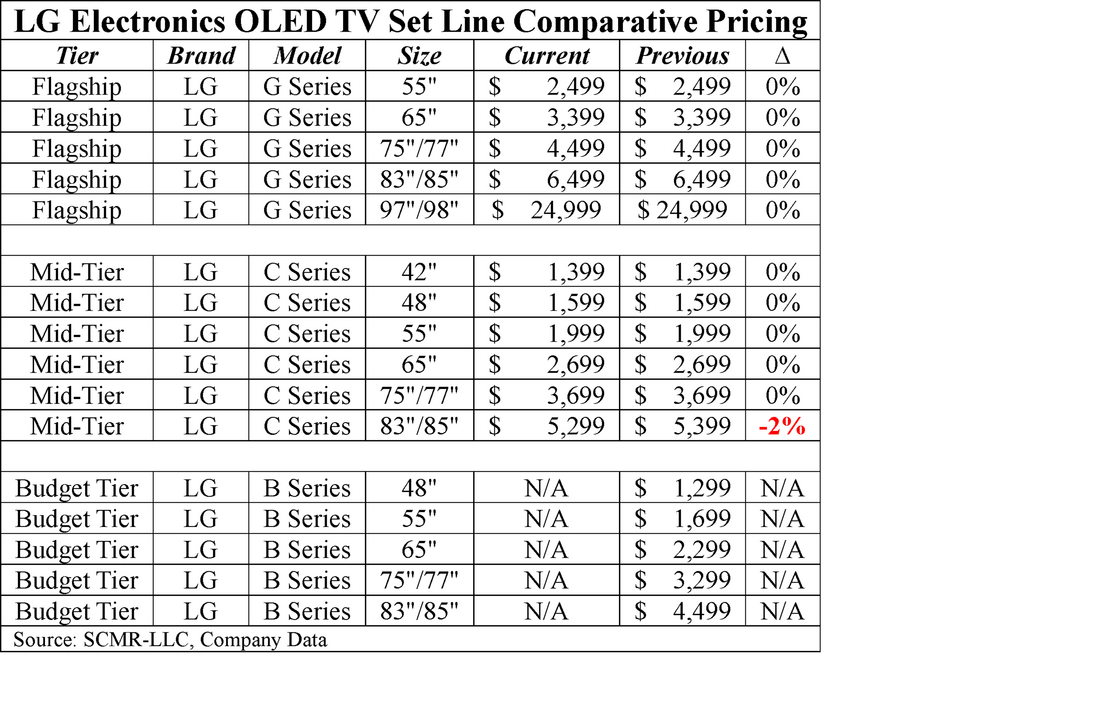

The most important point relating to LG’s TV set lineup is the pricing itself, which many expected to increase as the cost of memory and other components continues to rise into the new year. In fact, LG has kept initial TV set prices almost entirely in-line with last year’s initial set pricing, with only one model size different than last year, and that price is actually lower than last year.

New TV models from major brands are typically announced at the Consumer Electronics Show in early January, but pricing is not usually revealed until March or April, right around when they become available for pre-order. There are a number of reasons why TV set brands hesitate to reveal prices early in the new year, some of which are fiscal and some psychological.

The “Price Reveal” pulls the curtain away from the hype that surrounds the new models early in the year and adds a sense of reality that allows the consumer to make a judgement as to whether the propaganda is worth the money. In fact, almost all brands have revealed 2026 TV set prices, with only Samsung Electronics (005930.KS) the holdout at this point in the year. That said, LG Electronics (066570.KS), who revealed the pricing for much of their flagship and mid-tier TV sets recently, is holding back the pricing on their budget tier sets, likely until they get an understanding of Samsung’s pricing.

LG’s Premium Strategy: Holding the Line on OLED

The most important point relating to LG’s TV set lineup is the pricing itself, which many expected to increase as the cost of memory and other components continues to rise into the new year. In fact, LG has kept initial TV set prices almost entirely in-line with last year’s initial set pricing, with only one model size different than last year, and that price is actually lower than last year.

The LCD Defensive: Aggressive Cuts in Non-Premium Tiers

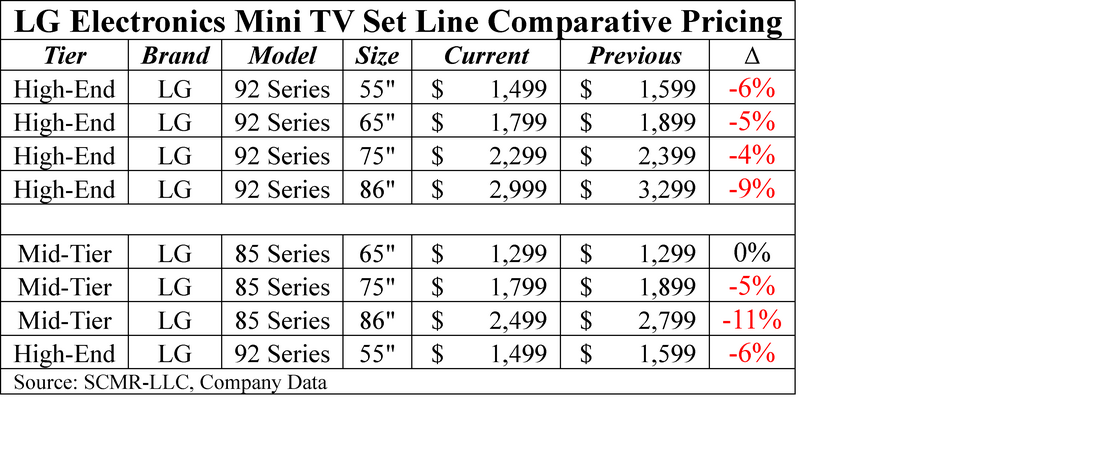

However, LG’s TV set lines are more than just OLED. The company also offers Mini-LED TV sets, Quantum dot enhanced LCD TVs, and generic LCD TVs, and the pricing on these “Non-Premium” lines is even more different from expectations. With only one exception (Flat), all of LG’s Mini-LED TV sets, both this year’s high and low price tiers), are priced below the initial price these sets were offered at last year, antithetical to conventional wisdom.

However, LG’s TV set lines are more than just OLED. The company also offers Mini-LED TV sets, Quantum dot enhanced LCD TVs, and generic LCD TVs, and the pricing on these “Non-Premium” lines is even more different from expectations. With only one exception (Flat), all of LG’s Mini-LED TV sets, both this year’s high and low price tiers), are priced below the initial price these sets were offered at last year, antithetical to conventional wisdom.

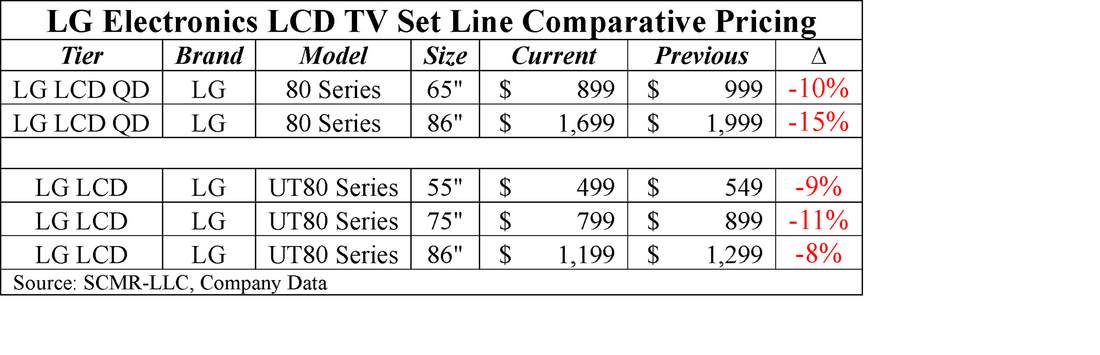

Taking this unusual circumstance further, when looking at LG’s more generic LCD TV line, both with quantum dots and without, the discounts to last year’s pricing are even greater, averaging almost 11%. We do expect the pricing for the budget tier of LG’s OLED line to remain flat, at the least, but depending on Samsung’s competitive positioning, it could fall below last year’s initial prices.

Industry-Wide Trends: BOM Pressure vs. Brand Identity

As noted, as the largest TV set brand globally, the TV set pricing data from Samsung is quite important for the industry. Samsung is quite aware of this fact and holds out its reveal as long as possible to keep competitors guessing, but even without Samsung we can poll other large brands and see if they follow LG’s lead or if the trend is in other directions.

We note that the data for each brand is tempered by BOM pressure as noted, but also by brand strategy, which can have a significant effect on new year TV set pricing, along with trying to manage 2025 remaining inventory. Higher initial prices will drive consumers to last year’s models, while lower prices will bring them to the new line of sets 2026 is already shaping up to be a year of ‘influences’ with even more factors pushing brands in one direction or the other. Tariff issues and transportation headaches have already begun to complecate an already complicated CE space. That said, we collected data similar to LG’s data for four other brands which we summarize below.

Competitor Breakdown: Five Different Paths to 2026

The 2026 "Price Reveal" has effectively unmasked a deeply bifurcated industry strategy. While the narrative early in the year focused on BOM (Bill of Materials) pressure and rising component costs, the actual pricing data suggests that brand strategy is currently outweighing fiscal necessity. We are seeing a market split into two distinct camps: those prioritizing brand elevation and margin preservation, and those engaged in an aggressive pursuit of market share.

Sony and HiSense represent the "margin first" contingent. Sony is leaning heavily into its heritage as a premium Tier-1 brand, betting that consumers will pay a nearly 20% premium for flagship processing. HiSense is perhaps making an even bolder move; by aggressively up-tiering their mainstream pricing by over 8%, they are signaling an end to their "budget brand" identity, attempting to move into the vacuum left by brands that have historically held the mid-to-high ground.

Conversely, Vizio, TCL, and LG are playing a defensive volume game, though with different tools. Vizio’s double-digit collapse in year-over-year pricing is a clear "shock and awe" campaign intended to re-establish the brand's footprint under its new ownership. TCL continues to leverage its vertical integration to commoditize the 65” to 75” market while keeping a premium "tax" on the ultra-large sets they alone can manufacture at scale. LG, meanwhile, is effectively using a "shield and sword" strategy—using stable OLED pricing as the shield to protect their premium image, while using their LCD line as the sword to slash into the mass-market share of their Chinese competitors.

The Samsung Pivot: Waiting for the Final Piece

The final piece of the 2026 puzzle remains Samsung. As the lone holdout, Samsung’s eventual pricing will act as the ultimate pivot point for the year. If they follow Sony’s lead toward margin expansion, it will provide a much-needed "pricing umbrella" for the rest of the industry. However, if they choose to follow LG and Vizio into a price war to protect their #1 global position, 2026 will quickly transform from a year of "strategic influences" into a race to the bottom that will test the fiscal endurance of every brand on this list. We will know in about a month.

As noted, as the largest TV set brand globally, the TV set pricing data from Samsung is quite important for the industry. Samsung is quite aware of this fact and holds out its reveal as long as possible to keep competitors guessing, but even without Samsung we can poll other large brands and see if they follow LG’s lead or if the trend is in other directions.

We note that the data for each brand is tempered by BOM pressure as noted, but also by brand strategy, which can have a significant effect on new year TV set pricing, along with trying to manage 2025 remaining inventory. Higher initial prices will drive consumers to last year’s models, while lower prices will bring them to the new line of sets 2026 is already shaping up to be a year of ‘influences’ with even more factors pushing brands in one direction or the other. Tariff issues and transportation headaches have already begun to complecate an already complicated CE space. That said, we collected data similar to LG’s data for four other brands which we summarize below.

Competitor Breakdown: Five Different Paths to 2026

- LG - Defensive Stability & OLED Protection

- Total Weighted change - ↓2.13%

- LG is focused on protecting its premium OLED market share. They kept Flagship (G-Series) and Mid-Tier (C-Series) pricing nearly identical to last year (0% to -2%). However, they are aggressively cutting prices in their LCD and QNED (QD) lines (-9% to -13%). LG is signaling that OLED is a premium and stable investment while using their lower-end LCD sets to fight off the aggressive price-cutting from TCL and HiSense in the mass market.

- Sony (SNE) - Premium Aspirations & Margin Preservation

- Total Weighted Change: +2.97%

- Sony remains relatively stable overall. While their Flagship models saw nearly a 20% jump, their "Elite" and "Performance" tiers stayed flat at 0%, which balanced out the total brand impact. Sony is betting on superior processing and brand equity to justify higher entry prices for their newest tech. By keeping other tiers flat rather than cutting them, they are prioritizing profit margins over raw volume, refusing to join the "race to the bottom" that can typify TV set pricing.

- HiSense (600060.CH) - Aggressive Up-Tiering

- Total Weighted Change: +8.55%

- Despite some price cuts in their "Value" tier, HiSense has the highest overall increase. This is driven by significant double-digit price hikes in their high-volume "Performance" and "Mainstream" categories. HiSense is attempting to shift its brand image from "budget" to "premium performance”. It seems they are using their low-end sets to attract customers but expect to upsell to models that carry higher margins.

- TCL (000100.CH) - "Big Screen" Pivot

- Total Weighted Change: -1.87%

- TCL is showing a slight downward trend for the brand. Their huge price increases in the "Ultra-High" (98"+) segment were almost entirely offset by aggressive price drops across their Budget, Entry-Mini, and Performance lines. TCL is banking on the "Bigger is Better" trend. By making 65" and 75" sets much cheaper, they drive volume; by raising prices on the 98" and 115" sets, they capitalize on their unique manufacturing advantage in giant panels where there is less competition.

- Vizio (WMT): Market Share Recovery

- Total Weighted Change: -16.40%

- Vizio is the only brand in the set with a double-digit decrease across the entire brand. They are cutting prices across every tier that had year-over-year data, signaling a very aggressive value-focused strategy for 2026. Vizio is in full "disruption mode" to claw back market share lost to TCL and HiSense. They are aiming to be the default choice for the price-conscious consumer at big-box retail, likely prioritizing unit volume and platform growth (SmartCast) over hardware margins. While likely a necessary early strategy to identify the brand with its new owner, the longer-term prospects for that strategy are less robust..

The 2026 "Price Reveal" has effectively unmasked a deeply bifurcated industry strategy. While the narrative early in the year focused on BOM (Bill of Materials) pressure and rising component costs, the actual pricing data suggests that brand strategy is currently outweighing fiscal necessity. We are seeing a market split into two distinct camps: those prioritizing brand elevation and margin preservation, and those engaged in an aggressive pursuit of market share.

Sony and HiSense represent the "margin first" contingent. Sony is leaning heavily into its heritage as a premium Tier-1 brand, betting that consumers will pay a nearly 20% premium for flagship processing. HiSense is perhaps making an even bolder move; by aggressively up-tiering their mainstream pricing by over 8%, they are signaling an end to their "budget brand" identity, attempting to move into the vacuum left by brands that have historically held the mid-to-high ground.

Conversely, Vizio, TCL, and LG are playing a defensive volume game, though with different tools. Vizio’s double-digit collapse in year-over-year pricing is a clear "shock and awe" campaign intended to re-establish the brand's footprint under its new ownership. TCL continues to leverage its vertical integration to commoditize the 65” to 75” market while keeping a premium "tax" on the ultra-large sets they alone can manufacture at scale. LG, meanwhile, is effectively using a "shield and sword" strategy—using stable OLED pricing as the shield to protect their premium image, while using their LCD line as the sword to slash into the mass-market share of their Chinese competitors.

The Samsung Pivot: Waiting for the Final Piece

The final piece of the 2026 puzzle remains Samsung. As the lone holdout, Samsung’s eventual pricing will act as the ultimate pivot point for the year. If they follow Sony’s lead toward margin expansion, it will provide a much-needed "pricing umbrella" for the rest of the industry. However, if they choose to follow LG and Vizio into a price war to protect their #1 global position, 2026 will quickly transform from a year of "strategic influences" into a race to the bottom that will test the fiscal endurance of every brand on this list. We will know in about a month.

RSS Feed

RSS Feed