…and the Survey Says…

Typically surveys are conducted by humans that ask carefully crafted questions to (hopefully) a cross-section of industry personnel that have relevant experience in the survey genre. The questions are key and even slight changes to question language can have a significant impact on the answers (Sidebar). Lucidworks (pvt), a software company that specializes in search applications, performed three yearly surveys to see how AI has evolved, essentially how many participants have moved to deployment, are still watching from the sidelines, or are stuck in a pilot phase loop.

As we note that the questions themselves can add bias to the survey, Lucidworks has endeavored to remove another possible source of bias by both removing the potential subjectivity of those that tally the answers, and, even more importantly, the inherent biases in the answers themselves. They do this by not asking questions and listening to the participants promote their own view of the AI world, but by using their own agentic AI to collect hard implementation data from the respondents. In theory, this should remove much of the bias and noise from the results, but we have to take Lucidworks’ word for that. Here is the participant data:

A portion of the survey data is categorical in that it puts respondents into one of four categories in terms of their approach to agentic AI. The obvious favorite for Lucidworks itself is Achievers, those who have “…mastered the foundations while successfully implementing cutting-edge AI; operate with comprehensive AI governance frameworks; demonstrate clear ROI measurement”, and use a “balanced implementation of proven and emerging technologies to create compelling customer experiences.” This category represented 35% of the respondents, with examples being Amazon (AMZN), Costco (COST), Tesla (TSLA), and Ford (F).

Builders are the next group, representing 14% of respondents. They are defined as “Strong in essential capabilities but limited agentic implementation; excellent at foundation but measured about emerging technologies; solid governance and data quality; focused on perfecting core experiences.” Examples are Jeep (STLA), Paccar (PCAR), Neiman Marcus (pvt), and Bealls (pvt).

Category three, Climbers, represented 10% of respondents, described as “Advanced in agentic capabilities but missing opportunities in essential foundations; early adopters of cutting-edge tech; implementing innovative but sometimes isolated AI initiatives; may prioritize novel experiences over fundamentals.” Examples would be Macys (M), Marshalls (TJX), Winnebago (WGO), and Thor (THO).

Spectators are the final category and also the largest at 41%. Spectators are “Developing implementation across both dimensions; measured approach to AI adoption; common focus areas include building organizational readiness, addressing talent gaps, or refining strategy; learning from market experiences.” Examples would be Dollar Tree (DLTR), Kenworth (PCAR), Wabash (WNC), and Ross (ROST).

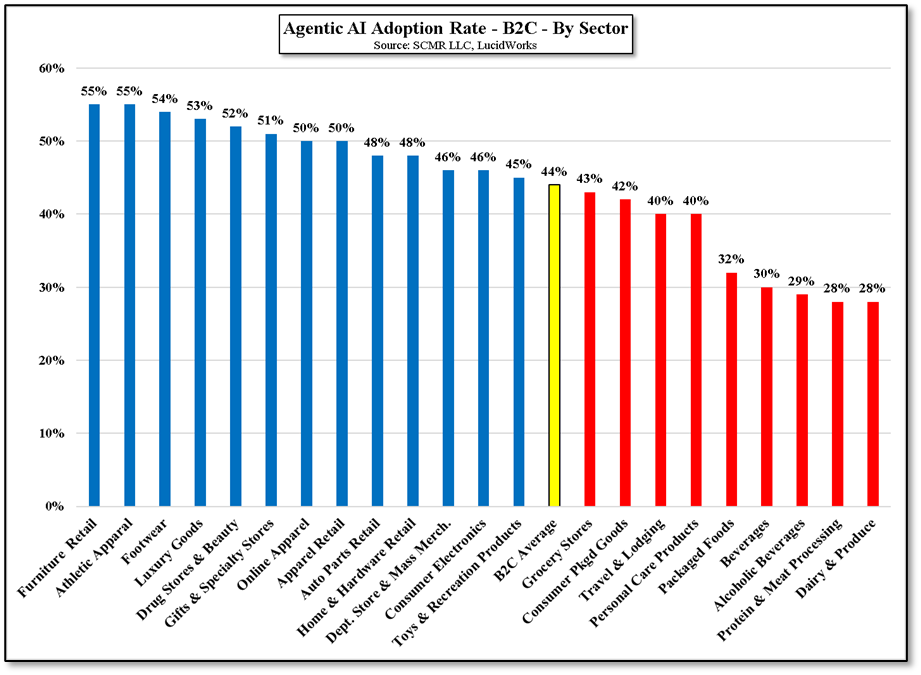

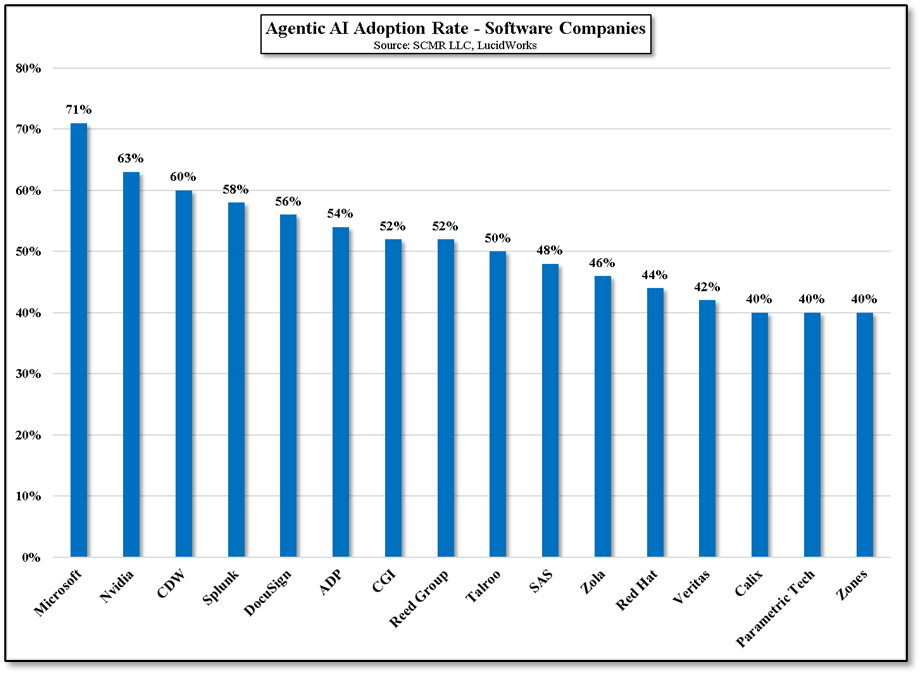

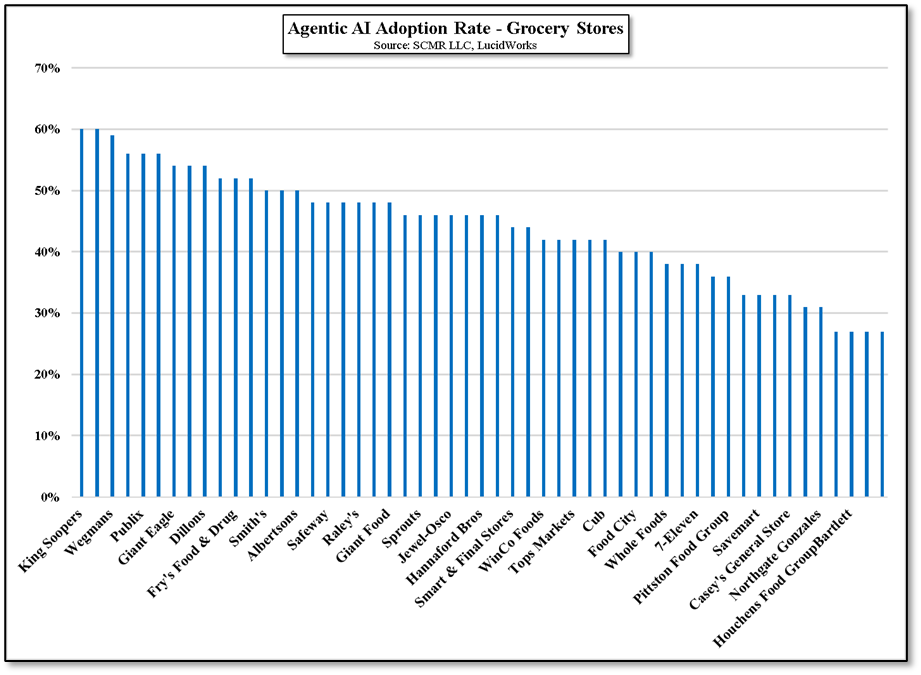

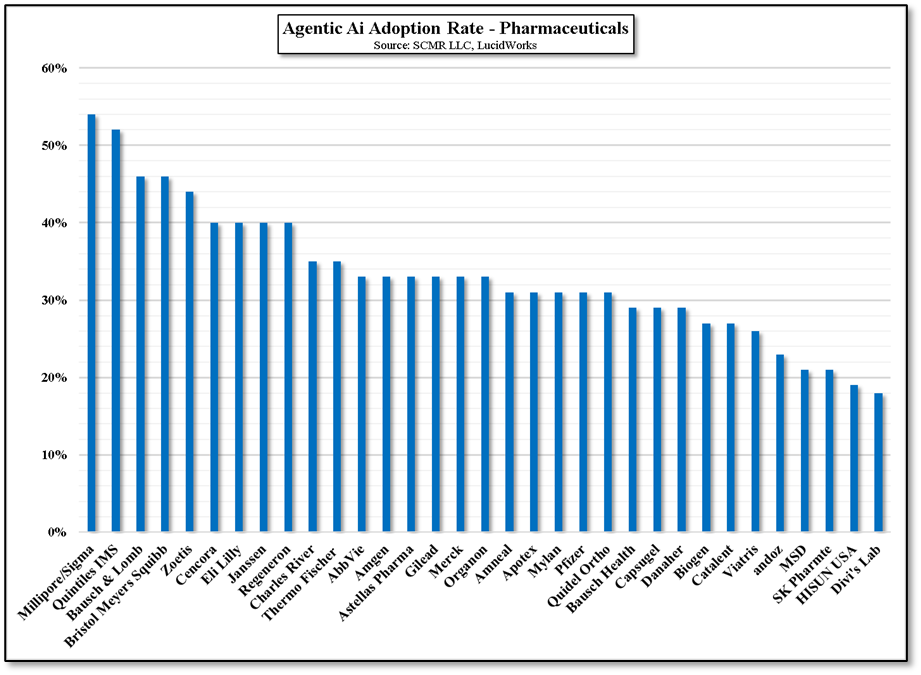

The data on implementation breaks down into broad industry segments in Figure 1, with Furniture Retail the leading category (55%) and Dairy & Produce the laggard (28%) with an average at ~44% across all industry segment, but the data goes further, with details by sector and company, a few of which we show below; Two tech sectors and two very non-tech. The data is even more granular than we show in Figure 1, with each company broken down into four AI application type categories; Ecommerce essentials, Classic AI/ML, AI Enriched, and Agentic AI, typically with the highest share of each total being ecommerce and classic AI/ML. Based on the average for each category we show, software ranked the highest at 51% with semiconductors close behind at 50%, while grocery stores came in at an average of 44% and most surprisingly pharmaceuticals with the lowest average of 33%. All of that said, only 30% of all the companies in the survey have implemented more than half of the four essential AI capabilities (in bold above), and only 5% have fully implemented all essential capabilities.

As noted, the data above was collected and analyzed by LucidWork’s own agentive AI, so it is also necessary to try to see how that data matches with the ‘verbal’ data that participants submitted to LucidWorks, which follows.

Based on data from the 2023, where 93% of companies indicated that they were planning to increase their AI spending, 2024’s 63% seemed a bit cool, but this year that same metric was 62% only a bit smaller than last year, so it does not seem like we are close to a spending reduction inflection point quite yet. That said, 83% of AI leaders indicated major or extreme concern regarding generative AI, including its cost and effectiveness., an 8% increase from 2024. Of the five biggest concerns indicated (see below), the biggest change from 2023 was concern over deployment costs, which increased by 18x from 2023 (share of concern, not actual costs), but at the same time the portion of companies that said they realized significant benefits from AI increased by 15% y/y to 34% this year, and we note that 43% of those in the healthcare industry indicated those same AI benefits, the highest of all industries.

Two other interesting points from the survey were that 21% of the respondents used open source models exclusively, 49% used only commercial products, while 30% used both, and 42% of respondents used a single model type, 31% used two models, 16% used three, 8% used 4 and 3% used five or more models.

What we come away with after reviewing the surveys is that while generative and agentic AI remains high on both B2B and B2C implementation lists, the headlong rush of 2023 and early 2024 seems to have passed the “In at any cost” level and is now more focused on gaining real-world benefits from AI at a reasonable cost. We are nowhere near a major pullback at the corporate level, but it is important to note that the idea of balancing cost against benefit is now as important as making sure everyone knows our company has AI. Quantifying those potential and real-world benefits will be the next major step.

As we note that the questions themselves can add bias to the survey, Lucidworks has endeavored to remove another possible source of bias by both removing the potential subjectivity of those that tally the answers, and, even more importantly, the inherent biases in the answers themselves. They do this by not asking questions and listening to the participants promote their own view of the AI world, but by using their own agentic AI to collect hard implementation data from the respondents. In theory, this should remove much of the bias and noise from the results, but we have to take Lucidworks’ word for that. Here is the participant data:

- 1600+ AI practitioners

- 28% Executives

- 42% Managers

- 30% Technical Decision Makers

- 15 Industries/8 Countries

- 53% North America

- 32% EMEA

- 15% APAC

A portion of the survey data is categorical in that it puts respondents into one of four categories in terms of their approach to agentic AI. The obvious favorite for Lucidworks itself is Achievers, those who have “…mastered the foundations while successfully implementing cutting-edge AI; operate with comprehensive AI governance frameworks; demonstrate clear ROI measurement”, and use a “balanced implementation of proven and emerging technologies to create compelling customer experiences.” This category represented 35% of the respondents, with examples being Amazon (AMZN), Costco (COST), Tesla (TSLA), and Ford (F).

Builders are the next group, representing 14% of respondents. They are defined as “Strong in essential capabilities but limited agentic implementation; excellent at foundation but measured about emerging technologies; solid governance and data quality; focused on perfecting core experiences.” Examples are Jeep (STLA), Paccar (PCAR), Neiman Marcus (pvt), and Bealls (pvt).

Category three, Climbers, represented 10% of respondents, described as “Advanced in agentic capabilities but missing opportunities in essential foundations; early adopters of cutting-edge tech; implementing innovative but sometimes isolated AI initiatives; may prioritize novel experiences over fundamentals.” Examples would be Macys (M), Marshalls (TJX), Winnebago (WGO), and Thor (THO).

Spectators are the final category and also the largest at 41%. Spectators are “Developing implementation across both dimensions; measured approach to AI adoption; common focus areas include building organizational readiness, addressing talent gaps, or refining strategy; learning from market experiences.” Examples would be Dollar Tree (DLTR), Kenworth (PCAR), Wabash (WNC), and Ross (ROST).

The data on implementation breaks down into broad industry segments in Figure 1, with Furniture Retail the leading category (55%) and Dairy & Produce the laggard (28%) with an average at ~44% across all industry segment, but the data goes further, with details by sector and company, a few of which we show below; Two tech sectors and two very non-tech. The data is even more granular than we show in Figure 1, with each company broken down into four AI application type categories; Ecommerce essentials, Classic AI/ML, AI Enriched, and Agentic AI, typically with the highest share of each total being ecommerce and classic AI/ML. Based on the average for each category we show, software ranked the highest at 51% with semiconductors close behind at 50%, while grocery stores came in at an average of 44% and most surprisingly pharmaceuticals with the lowest average of 33%. All of that said, only 30% of all the companies in the survey have implemented more than half of the four essential AI capabilities (in bold above), and only 5% have fully implemented all essential capabilities.

As noted, the data above was collected and analyzed by LucidWork’s own agentive AI, so it is also necessary to try to see how that data matches with the ‘verbal’ data that participants submitted to LucidWorks, which follows.

Based on data from the 2023, where 93% of companies indicated that they were planning to increase their AI spending, 2024’s 63% seemed a bit cool, but this year that same metric was 62% only a bit smaller than last year, so it does not seem like we are close to a spending reduction inflection point quite yet. That said, 83% of AI leaders indicated major or extreme concern regarding generative AI, including its cost and effectiveness., an 8% increase from 2024. Of the five biggest concerns indicated (see below), the biggest change from 2023 was concern over deployment costs, which increased by 18x from 2023 (share of concern, not actual costs), but at the same time the portion of companies that said they realized significant benefits from AI increased by 15% y/y to 34% this year, and we note that 43% of those in the healthcare industry indicated those same AI benefits, the highest of all industries.

Two other interesting points from the survey were that 21% of the respondents used open source models exclusively, 49% used only commercial products, while 30% used both, and 42% of respondents used a single model type, 31% used two models, 16% used three, 8% used 4 and 3% used five or more models.

What we come away with after reviewing the surveys is that while generative and agentic AI remains high on both B2B and B2C implementation lists, the headlong rush of 2023 and early 2024 seems to have passed the “In at any cost” level and is now more focused on gaining real-world benefits from AI at a reasonable cost. We are nowhere near a major pullback at the corporate level, but it is important to note that the idea of balancing cost against benefit is now as important as making sure everyone knows our company has AI. Quantifying those potential and real-world benefits will be the next major step.

Figure 1 - Agentic AI Adoption - B2C - By Sector - Source: SCMR LLC, LucidWorks

Figure 3 - Agentic AI Adoption - Semiconductor Companies - Source: SCMR LLC, LucidWorks

Figure 4 - Agentic AI Adoption Rate - Grocery Stores - Source -SCMR LLC, LucidWorks

Figure 5 - Agentic AI Adoption Rate - Pharmaceuticals - Source: SCMR LLC, LucidWorks

RSS Feed

RSS Feed