The Weight of the Metaverse

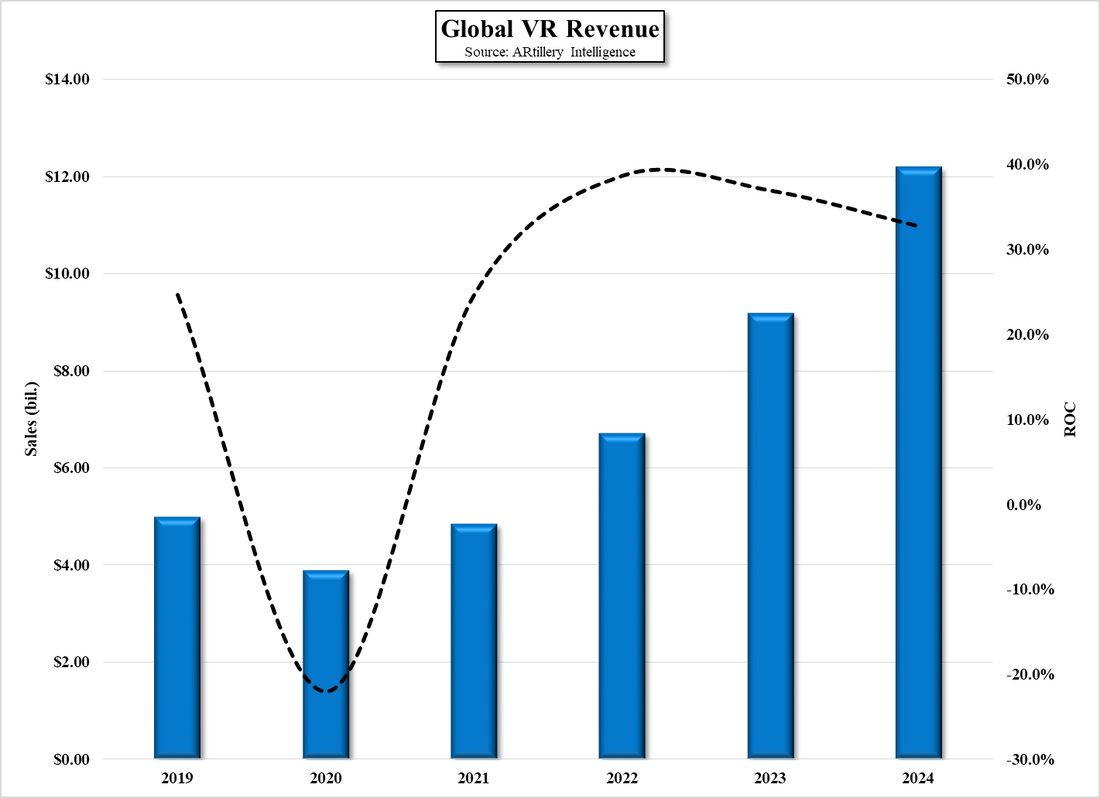

The metaverse is still around, despite the tech refocus on AI, and VR headsets are the gateway to this world of make-believe, but until the metaverse is something substantial enough to attract even a modest portion of consumers, the VR space will have to rely on gaming to generate headset sales, with headset brands hoping that a more robust macro environment will help to boost sales this year, after a dismal 2022. According to published numbers, which vary considerable from source to source, VR headset shipments declined ~20% last year, for the first time, after years of large gains, albeit on smaller bases in the early years.

There are many factors that come into play when it comes to VR headset sales, however there is one facto, aside from price, that might be considered the ‘elephant in the room’, and that is weight. VR headsets are complex devices, containing considerable optical and electronic components, along with batteries (in some cases), cameras, displays, and fans, all of which add up to what can be a ridiculously odd looking and weighty headset that can become quite fatiguing. As each headset brand is looking to provide its own combination of features and visual quality, much effort is placed on squeezing in as much necessary equipment as possible into the average headset, and while all brands try to keep headset weight in mind, headset developers are usually big fans of VR in general and are likely willing to accept a heavy and bulky headset than the average consumer.

Our VR database shows that the average weight of a VR headset is trending down, albeit slowly, with the average for headsets either released this year or expected to be released, is ~382 grams, or the equivalent of a loaf of bread with a few slices missing, so imagine playing a game with an almost full loaf of bread on one’s head, and it becomes easier to understand why VR headset weight is a significant factor for VR users. [Note that the Hi/Lo range scale is on the left side of the chart, with this year’s heaviest headset weighing in at 625 oz, or the weight of a healthy squirrel.]

While all brands are interested in reducing the weight of their VR headsets, it is a tradeoff against technology and features, with many looking toward those characteristics over headset weight, but there are those that are working toward making VR headsets more than (less than?) the bulky devices they are today. One company in particular has taken the weight challenge to heart and will be releasing its first VR headset this year that will clock in at a mere 127 grams, 1/3 of the average 2023 VR headset weight, and only 20% of the weight of this year’s heaviest headset. While the company Bigscreen (pvt) has been around since 2014 and has released only a beta headset in 2016, the new ‘Beyond’ headset, which ships in 3Q, is designed to be the lightest and smallest VR headset available, and while it will certainly play games it comes with an interface box that allows the user to rent 3D movies (200+ available through the company), browse TV channels, watch live events, or do more conventional game playing (Twitch shared) and work oriented collaboration using Bigscreen software, which can be used on other VR headsets and is free.

The Bigscreen VR headset is not cheap, with a starting price of $1,000 (pre-order) and $100 for the audio strap, but when compared to other headsets, regardless of price, the ‘Beyond’ headset looks, by far, the most comfortable to wear for an extended period. The only issue that might become a problem is that the company decided not to make the headset IPD adjustable. IPD, or Inter-pupillary distance, is the distance between a user’s pupils, which is obviously different for each person. Many Vr headsets build in mechanics that can change the IPD to match the user, a particularly necessary detail, as an incorrect setting can cause blurry images and rapid eyestrain. Bigscreen did not want the heavy and bulky IPD adjustment hardware in the headset, so they will custom set the IPD for each user on order. This solves the problem but will slow production and raise costs considerably and will limit the headset’s use to one individual.

All in, while the Bigscreen headset has not been field tested yet, the company’s more practical development direction gives hope that VR brands understand that they have a number of major hurdles to cross before VR headsets are everyday items. Developers want all the bells and whistles, but that is not always what the average consumer wants, and they certainly don’t want a headset that feels like a squirrel is sitting on their head. Image quality is certainly a major consideration with VR headsets, but some of the add-ons make only minor improvements and add to the bulk of the headset. Absolute size and weight comparisons are hard to make without having the devices in physical reach, but we compared the images of the Bigscreen Beyond against the Sony (SNE) Playstation VR2, which sells for $550 and weighs 550 grams, and the Meta (FB) Quest Pro, which sells for $1,000 and weighs 722 grams.

There are many factors that come into play when it comes to VR headset sales, however there is one facto, aside from price, that might be considered the ‘elephant in the room’, and that is weight. VR headsets are complex devices, containing considerable optical and electronic components, along with batteries (in some cases), cameras, displays, and fans, all of which add up to what can be a ridiculously odd looking and weighty headset that can become quite fatiguing. As each headset brand is looking to provide its own combination of features and visual quality, much effort is placed on squeezing in as much necessary equipment as possible into the average headset, and while all brands try to keep headset weight in mind, headset developers are usually big fans of VR in general and are likely willing to accept a heavy and bulky headset than the average consumer.

Our VR database shows that the average weight of a VR headset is trending down, albeit slowly, with the average for headsets either released this year or expected to be released, is ~382 grams, or the equivalent of a loaf of bread with a few slices missing, so imagine playing a game with an almost full loaf of bread on one’s head, and it becomes easier to understand why VR headset weight is a significant factor for VR users. [Note that the Hi/Lo range scale is on the left side of the chart, with this year’s heaviest headset weighing in at 625 oz, or the weight of a healthy squirrel.]

While all brands are interested in reducing the weight of their VR headsets, it is a tradeoff against technology and features, with many looking toward those characteristics over headset weight, but there are those that are working toward making VR headsets more than (less than?) the bulky devices they are today. One company in particular has taken the weight challenge to heart and will be releasing its first VR headset this year that will clock in at a mere 127 grams, 1/3 of the average 2023 VR headset weight, and only 20% of the weight of this year’s heaviest headset. While the company Bigscreen (pvt) has been around since 2014 and has released only a beta headset in 2016, the new ‘Beyond’ headset, which ships in 3Q, is designed to be the lightest and smallest VR headset available, and while it will certainly play games it comes with an interface box that allows the user to rent 3D movies (200+ available through the company), browse TV channels, watch live events, or do more conventional game playing (Twitch shared) and work oriented collaboration using Bigscreen software, which can be used on other VR headsets and is free.

The Bigscreen VR headset is not cheap, with a starting price of $1,000 (pre-order) and $100 for the audio strap, but when compared to other headsets, regardless of price, the ‘Beyond’ headset looks, by far, the most comfortable to wear for an extended period. The only issue that might become a problem is that the company decided not to make the headset IPD adjustable. IPD, or Inter-pupillary distance, is the distance between a user’s pupils, which is obviously different for each person. Many Vr headsets build in mechanics that can change the IPD to match the user, a particularly necessary detail, as an incorrect setting can cause blurry images and rapid eyestrain. Bigscreen did not want the heavy and bulky IPD adjustment hardware in the headset, so they will custom set the IPD for each user on order. This solves the problem but will slow production and raise costs considerably and will limit the headset’s use to one individual.

All in, while the Bigscreen headset has not been field tested yet, the company’s more practical development direction gives hope that VR brands understand that they have a number of major hurdles to cross before VR headsets are everyday items. Developers want all the bells and whistles, but that is not always what the average consumer wants, and they certainly don’t want a headset that feels like a squirrel is sitting on their head. Image quality is certainly a major consideration with VR headsets, but some of the add-ons make only minor improvements and add to the bulk of the headset. Absolute size and weight comparisons are hard to make without having the devices in physical reach, but we compared the images of the Bigscreen Beyond against the Sony (SNE) Playstation VR2, which sells for $550 and weighs 550 grams, and the Meta (FB) Quest Pro, which sells for $1,000 and weighs 722 grams.

VR Headset Weight & Hi/Lo Range - 2013 - 2023 - Source: SCMR LLC

Bigscreen Beyond - Source: Bigscreen

Sony Playstation VR2 - Source: Sony

2022 Meta Quest Pro - Source: Meta

Note: We do not receive any compensation from the companies we mention and have no contractual relationship with same. We do speak with company management concerning products but have no vested interest in any public or private company. Our analysis of products and markets is entirely independent and does not represent the opinions of anyone other than ourselves.

RSS Feed

RSS Feed