5G – June

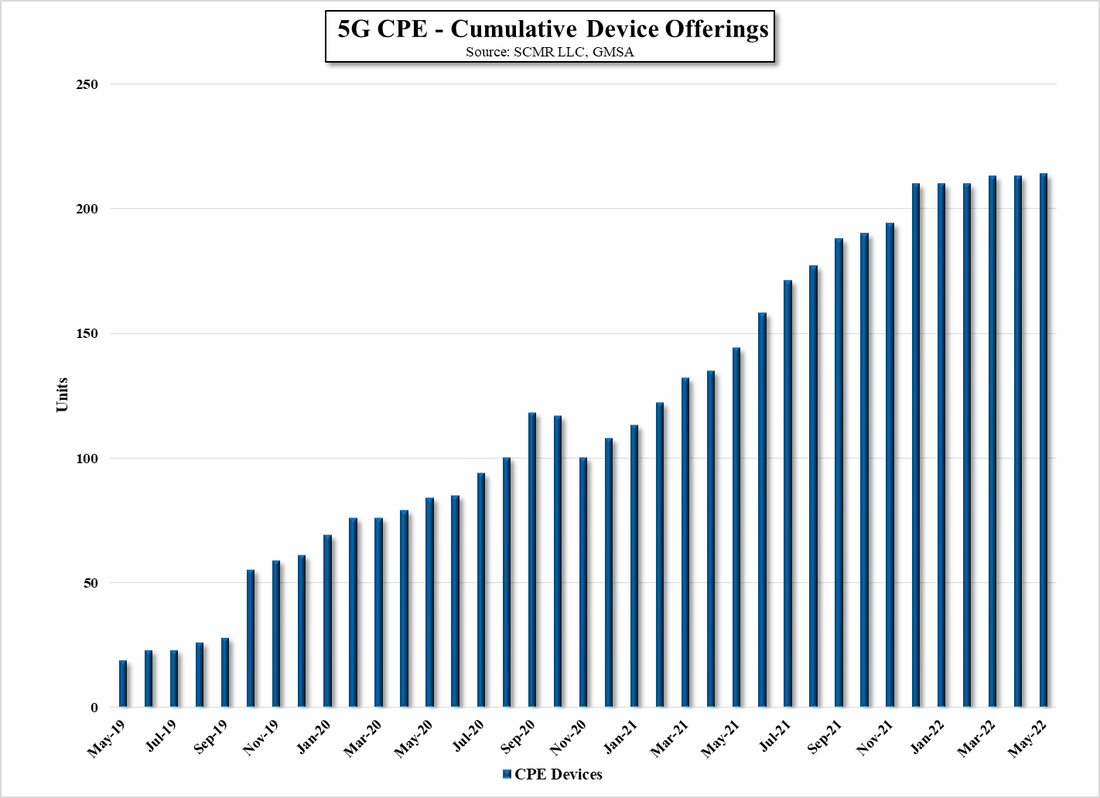

While the challenges facing the smartphone market are considerable and well-documented in our notes, 5G has been the only shining light in a sea of smartphone darkness and June results continue that trend. 5G smartphone offerings grew 5% m/m in June, putting y/y growth at 85.6%, while overall 5G device growth continued at 3.7% m/m and 79.0% y/y. As expected, the number of 5G form factors (types of 5G devices) has stabilized at 24 as has the number of 5G vendors at 193, while CPE device offerings increased 1.9% for the month and 51.4% for the year.

We expect that customer transitions to 5G are among the few justifications that consumers are using to purchase a new or replacement smartphone currently, with the release of the iPhone 14 series later this year the only seminal event that will empower consumers to return to the smartphone market. That said, it is also essential that Apple differentiates the iPhone 14 from the iPhone 13 enough to justify an upgrade, or, although a lesser possibility, offer the ‘same’ phone for less and is able to deliver devices on a reasonable schedule. Thus far we have not heard of any ‘leaked’ iPhone 14 features that might move the needle, but while iPhone aficionados might take umbrage with that comment because of a slight variation in camera setup or ‘notch’ placement, we hope there is something in Apple’s iPhone 14 arsenal that might bring back a bit of life to the smartphone market. Since Apple is already 5G compliant (both Sub6 and mmWave) there would be no 5G based incentive for iPhone users to upgrade.

We expect that customer transitions to 5G are among the few justifications that consumers are using to purchase a new or replacement smartphone currently, with the release of the iPhone 14 series later this year the only seminal event that will empower consumers to return to the smartphone market. That said, it is also essential that Apple differentiates the iPhone 14 from the iPhone 13 enough to justify an upgrade, or, although a lesser possibility, offer the ‘same’ phone for less and is able to deliver devices on a reasonable schedule. Thus far we have not heard of any ‘leaked’ iPhone 14 features that might move the needle, but while iPhone aficionados might take umbrage with that comment because of a slight variation in camera setup or ‘notch’ placement, we hope there is something in Apple’s iPhone 14 arsenal that might bring back a bit of life to the smartphone market. Since Apple is already 5G compliant (both Sub6 and mmWave) there would be no 5G based incentive for iPhone users to upgrade.

5G Ecosystem - Primary Indicators - Source: SCMR LLC, GSA.com

Selected 5G Devices - Device Offerings - Source: SCMR LLC, GMSA

5G Smartphone Unit Volume & ROC - Source: SCMR LLC, GSA.com

RSS Feed

RSS Feed