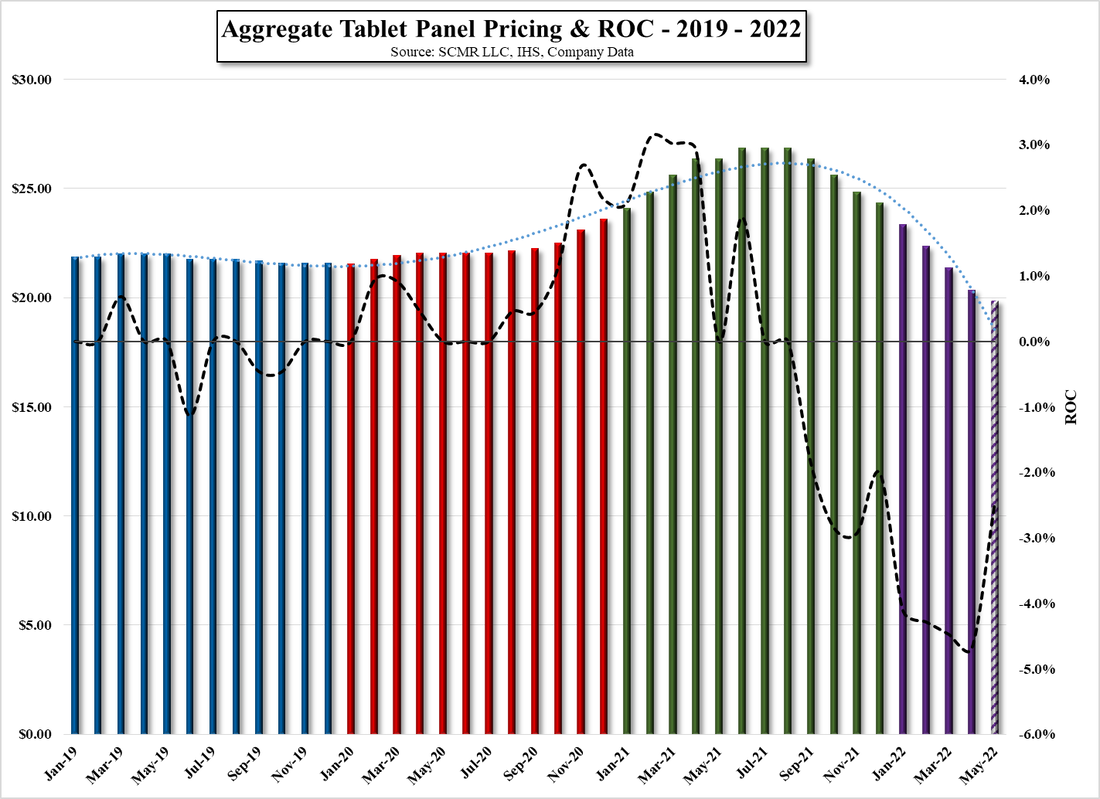

No 8K in the EU…

If new rules in the UK are not changed, starting in March of next year 8K and Micro-LED TVs will no longer be available to consumers in the EU. A series of energy-related rules will come into effect next year that set energy use requirements for televisions with more than UHD resolution (8K) and micro-LED based displays as part of a larger ‘ecodesign requirement for energy related products’ program initiated in 2019. When the guidelines were determined, 8K television sets were barely a notion, other than as demos at trade shows, so the specs were written (pre-2019 release) before there were a reasonable number of 8K sets available on which to make typical efficiency and power consumption calculations. The 2023 rules require that 8K television sets must consume the same amount of power as 4K sets or would be unable to be sold in the EU.

Based on a quick check of Mini-LED/QD and OLED TVs, 8K TVs consume 90% more power than their 4K equivalents, with 8K OLED TVs coming in at ~77% higher and the 8K Mini-LED/QD sets coming in ~102% above their 4K counterparts. A further look by the 8K Association, a group with an obviously big stake in the debate, has indicated that they find that no 8K television sets currently in the market would meet the new specifications. The regulatory committee that has set the guidelines is supposed to meet before the end of this year to review the guidelines, although no meetings have been scheduled to date.

The problems facing 8K TV power requirements is simple to understand. 8K TVs have to fit 4 times as many pixels into the same space as 4K TVs, which means each pixel has to be smaller. As the electronics that control each pixel remains basically the same size in both 4K and 8K, the area available for the backlight to pass through becomes smaller as a percentage of area in 8K pixels. In order to compensate for the lower amount of light, the backlight in 8K sets needs to be brighter and therefore requires more power. Additionally, given the increased number of pixels in 8K sets, the processing done for each pixel is also multiplied by 4, requiring more transistors and more power to drive them.

Those in the 8K ecosystem stand against the new regulations citing the effects on EU consumers who will no longer be able to avail themselves of the latest 8K content and will ‘fall behind’ other regions, although we are hard pressed to find a regional competition toward establishing 8K as the day-to-day television media format. Japan has the only (state-sponsored) 8K broadcast station, usually reserved for important events, travelogues, and nature specials, and while there are streaming services that supply 8K content, 8K TV sales have not been stellar, with ~350,000 8K sets sold last year, a less than 1% share of the TV market, and Samsung Electronics (005930.KS) holding a ~65% share.

While we understand both sides of the 8K argument, the broadcast industry is still grappling with 4K while some streaming services charge extra for 4K, so pushing the television industry toward reducing power requirements for 8K TV does not strike us as a bad idea, although one that has relatively little relevance to consumers at least currently. At some time in the future 8K will become germane to the industry but pressing the industry over a product that was developed way before it became useful to consumers will serve to push set producers to improve 8K set power consumption or abandon the product until there is at least some consumer demand. We doubt there will be much consumer lament over ‘falling behind’ other regions in the world of television technology…

Based on a quick check of Mini-LED/QD and OLED TVs, 8K TVs consume 90% more power than their 4K equivalents, with 8K OLED TVs coming in at ~77% higher and the 8K Mini-LED/QD sets coming in ~102% above their 4K counterparts. A further look by the 8K Association, a group with an obviously big stake in the debate, has indicated that they find that no 8K television sets currently in the market would meet the new specifications. The regulatory committee that has set the guidelines is supposed to meet before the end of this year to review the guidelines, although no meetings have been scheduled to date.

The problems facing 8K TV power requirements is simple to understand. 8K TVs have to fit 4 times as many pixels into the same space as 4K TVs, which means each pixel has to be smaller. As the electronics that control each pixel remains basically the same size in both 4K and 8K, the area available for the backlight to pass through becomes smaller as a percentage of area in 8K pixels. In order to compensate for the lower amount of light, the backlight in 8K sets needs to be brighter and therefore requires more power. Additionally, given the increased number of pixels in 8K sets, the processing done for each pixel is also multiplied by 4, requiring more transistors and more power to drive them.

Those in the 8K ecosystem stand against the new regulations citing the effects on EU consumers who will no longer be able to avail themselves of the latest 8K content and will ‘fall behind’ other regions, although we are hard pressed to find a regional competition toward establishing 8K as the day-to-day television media format. Japan has the only (state-sponsored) 8K broadcast station, usually reserved for important events, travelogues, and nature specials, and while there are streaming services that supply 8K content, 8K TV sales have not been stellar, with ~350,000 8K sets sold last year, a less than 1% share of the TV market, and Samsung Electronics (005930.KS) holding a ~65% share.

While we understand both sides of the 8K argument, the broadcast industry is still grappling with 4K while some streaming services charge extra for 4K, so pushing the television industry toward reducing power requirements for 8K TV does not strike us as a bad idea, although one that has relatively little relevance to consumers at least currently. At some time in the future 8K will become germane to the industry but pressing the industry over a product that was developed way before it became useful to consumers will serve to push set producers to improve 8K set power consumption or abandon the product until there is at least some consumer demand. We doubt there will be much consumer lament over ‘falling behind’ other regions in the world of television technology…

4K/8K Pixel Aperture Comparison - Source: SCMR LLC

RSS Feed

RSS Feed