(More) Fun With Data – China Smartphone Shipments - September – Better…

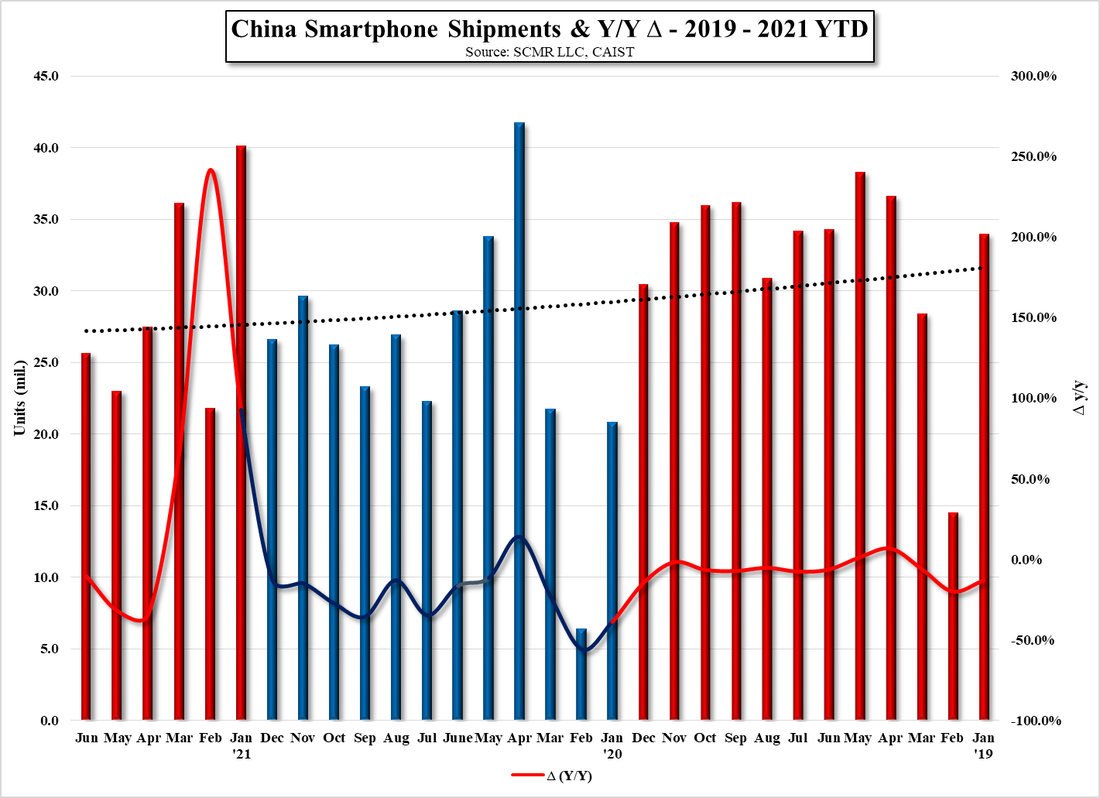

The China Academy for Information & Communications (CAICT) has released China’s smartphone shipments for September which came in at 20.922m units, a bit above our 19.79m unit estimate, putting the month up 10.22% and down only 2.2% y/y. While the slight outperformance is a positive, September 2021 was a particularly weak month, followed by stronger showings during the next three months. This will make y/y comparisons considerably more difficult for the remainder of the year and into January unless there is a meaningful upswell in Chinese smartphone demand. Discounting could be a factor in such a scenario, and there is likely a bit of pent-up demand to be released as the country eases it COVID stance, but we see those as relatively small factors rather than creating significant momentum.

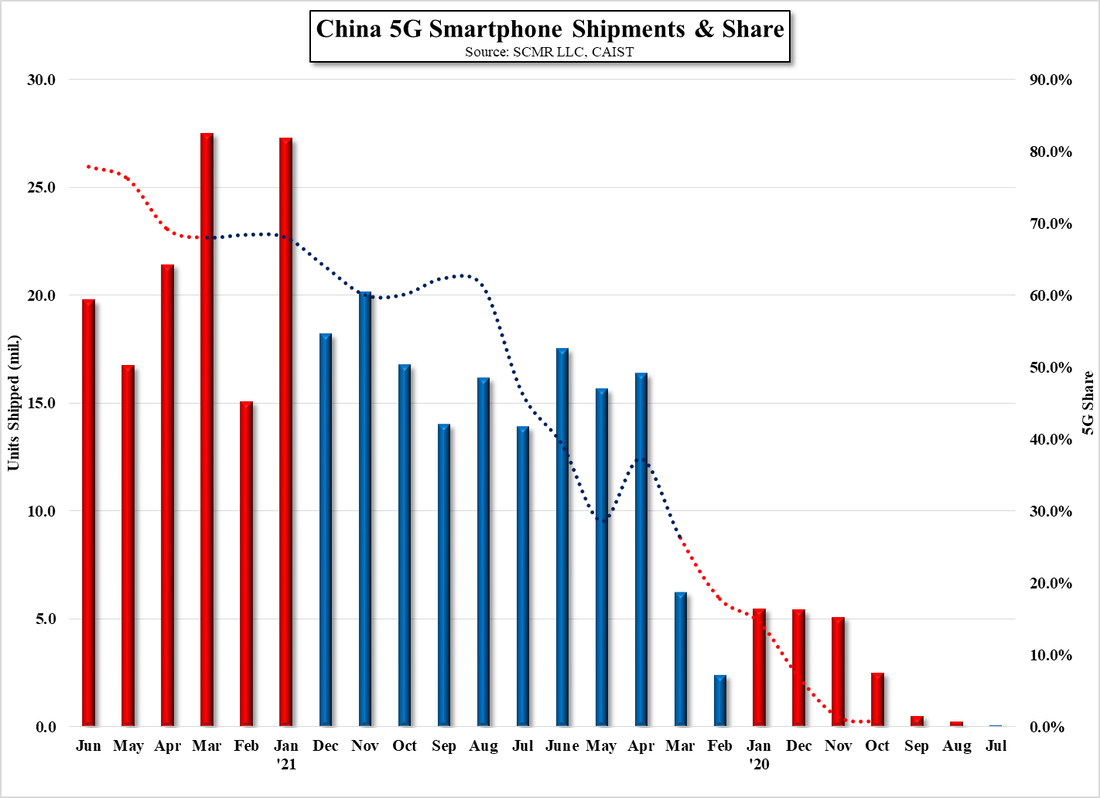

5G shipments were 15.104m units, up 5.9% m/m and essentially flat y/y, while representing 72.2% of all phones shipped on the Mainland in September, a bit lower than in past months this year. It is difficult to attribute the lower 5G share to a singular factor, but we would expect the overall macro situation might attract consumers to lower tier phones, where 5G is less penetrated. We would become concerned if the 5G share fell below 70% for more than a month or so, but our expectation is for a range between 70% and 80% for 2023, and our overall expectations for full year smartphone shipments in China remains at 252m units.

5G shipments were 15.104m units, up 5.9% m/m and essentially flat y/y, while representing 72.2% of all phones shipped on the Mainland in September, a bit lower than in past months this year. It is difficult to attribute the lower 5G share to a singular factor, but we would expect the overall macro situation might attract consumers to lower tier phones, where 5G is less penetrated. We would become concerned if the 5G share fell below 70% for more than a month or so, but our expectation is for a range between 70% and 80% for 2023, and our overall expectations for full year smartphone shipments in China remains at 252m units.

China Smartphone Shipments & Y/Y ROC - 2019 - 2022 YTD - Source: SCMR LLC, CAIST

China 5G Smartphone Shipments & Share - Source: SCMR LLC. CAIST

RSS Feed

RSS Feed