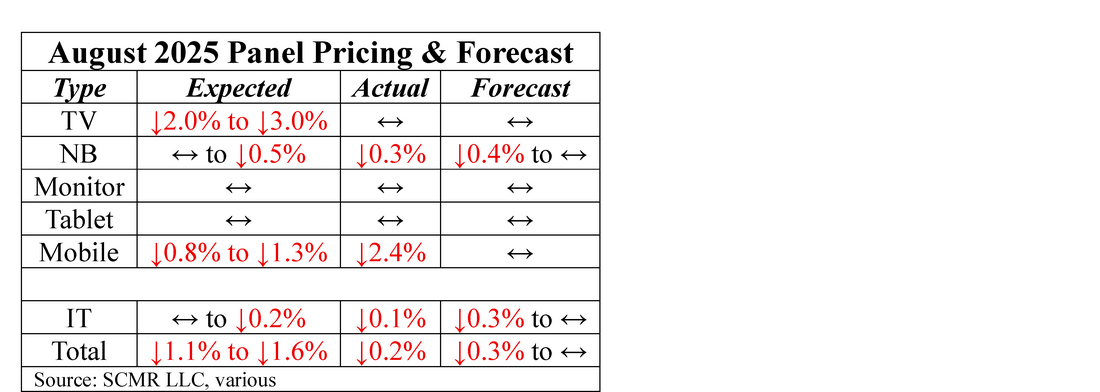

August Panels Pricing

Panel pricing was down 0.2% in August, a modest move after July’s 2.4% decline. TV panels were the standout, with no change for the month, far from our expectations of a 2.0% to 3.0% decline. It seems that after the 4.7% decline in July for TV panels, brands are using the lower prices to get inventory levels closer to targets, which, as we noted previously, have been lowered for the year. Seeing some demand strength (or perhaps a lack of pricing pressure), Chinese panel producers are pointing toward raising utilization rates from their recent upper 70’s% to 85% to 90% through September, to try to save 3Q after the weak July, but they run the risk of overbuilding into a 4th quarter that has little clarity for demand as to real demand.

While TV panels showed at least some price resilience, IT panels (Monitors, Notebooks, Tablets) did not, declining 0.1% for the 3rd month in a row. If you remember, IT products were to be the 2025 ‘saviors’ at the start of the year, yet demand has fizzled out as the complexities of tariffs and other macro issues make consumers wary. Small panel prices (Mobile) dropped by more than expected (down 2.4% m/m against expectations of down 1%) in August, making the 4th month in a row of negative mobile panel pricing.

While TV panels showed at least some price resilience, IT panels (Monitors, Notebooks, Tablets) did not, declining 0.1% for the 3rd month in a row. If you remember, IT products were to be the 2025 ‘saviors’ at the start of the year, yet demand has fizzled out as the complexities of tariffs and other macro issues make consumers wary. Small panel prices (Mobile) dropped by more than expected (down 2.4% m/m against expectations of down 1%) in August, making the 4th month in a row of negative mobile panel pricing.

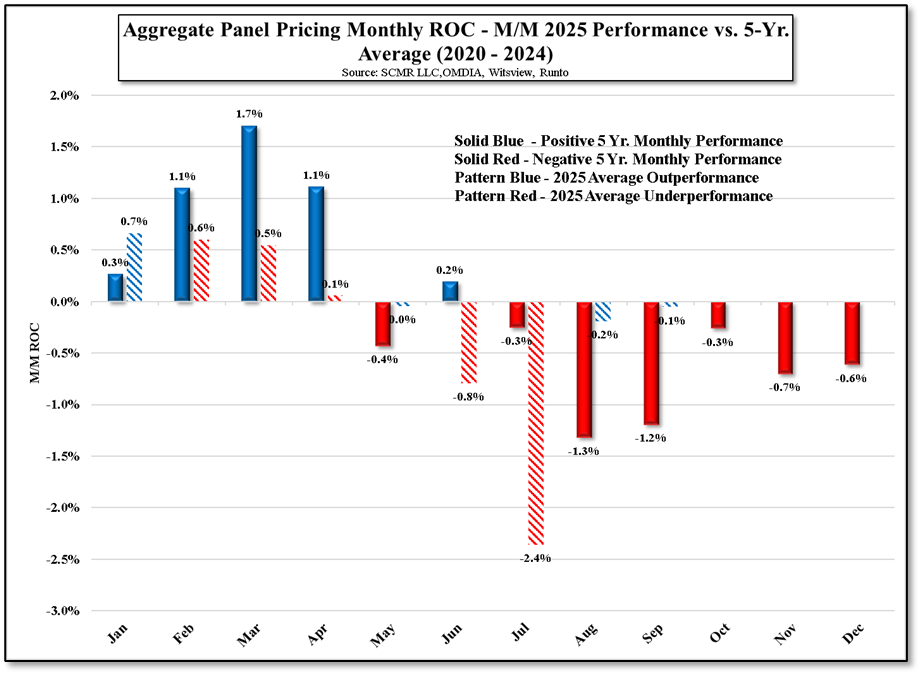

While volatility, for the most part, has been low this year, Figure 1shows how actual panel pricing performed thus far, against the 5-year averages. In January, panel prices grew more than the average, but February, March, and April saw pricing movements below average. May was better than average, followed by June and July where pricing was below average. In August and September (forecast), while negative, pricing outperformed the averages. We note that the 5-year averages for the last three months of the year are negative, indicating weaker pricing potential.

All in, August was a weak pricing month, albeit one where TV panel pricing was flat, but better than expected. We expect TV panel pricing in September to be flat on brand stocking demand, but concern over an inability to discount enough during the holidays to attract buyers continues to overhang the market. Chinese panel producers are reacting on a very short-term basis and increasing utilization but run the risk of flooding the market and creating a weak 4th quarter. They want to show profitability for the year in order to justify both short-term fab purchases and expansions, but are also focused on pointing out how they dominate South Korean producers concerning market share. It is hard to balance both.

All in, August was a weak pricing month, albeit one where TV panel pricing was flat, but better than expected. We expect TV panel pricing in September to be flat on brand stocking demand, but concern over an inability to discount enough during the holidays to attract buyers continues to overhang the market. Chinese panel producers are reacting on a very short-term basis and increasing utilization but run the risk of flooding the market and creating a weak 4th quarter. They want to show profitability for the year in order to justify both short-term fab purchases and expansions, but are also focused on pointing out how they dominate South Korean producers concerning market share. It is hard to balance both.

Figure 1 - Aggregate Panel Pricing Monthly ROC - M/M 2025 Performance vs. 5-Yr. Average (2022 - 2024) - Source: SCMR LLC,OMDIA, Witsview, RUNTO

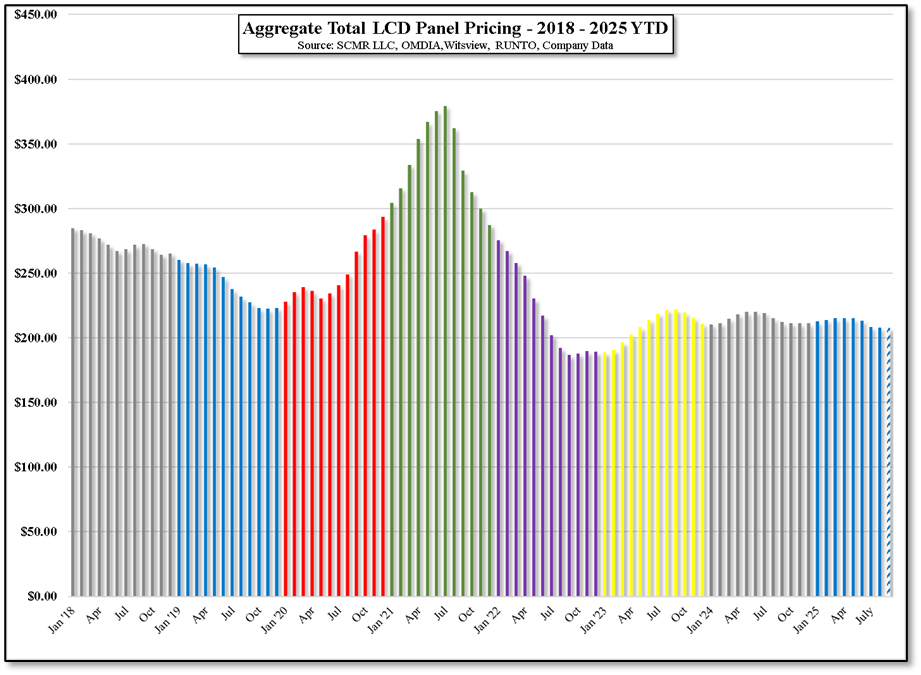

Figure 2 - Aggregate Total LCD PAnel Pricing - 2018 - 2025 YTD - Source: SCMR LLC, OMDIA, Witsview, RUNTO, COmpany Data

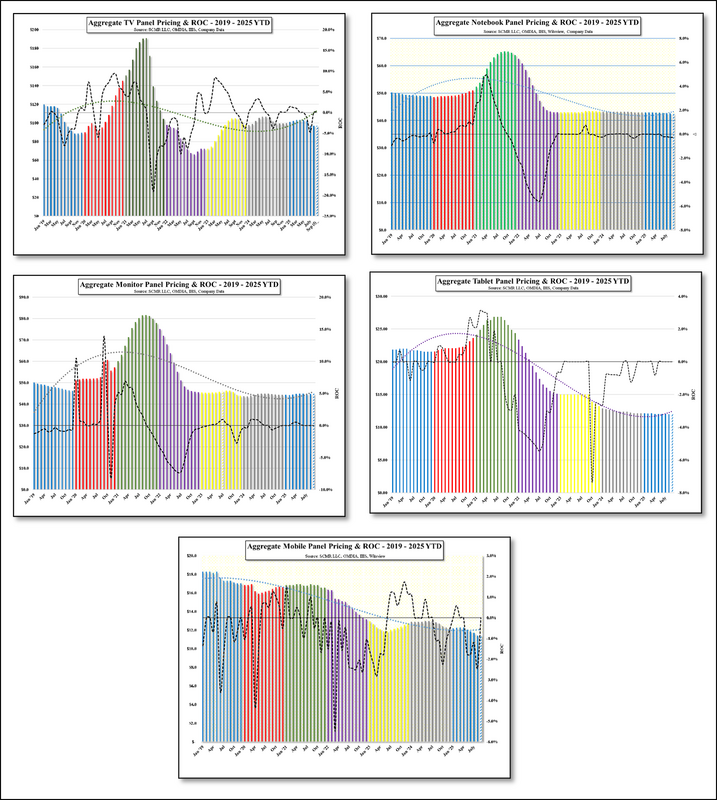

Figure 3 - Aggregate PAnel Pricing by Category - 2019 - 2025 YTD - Source: SCMR LLC, OMDIA, Witsview, RUNTO, Company Data

RSS Feed

RSS Feed