Benefaction Blues

Last year the Chinese State Council issued “The Action Plan for Promoting Large-scale Equipment Renewal and Consumer Goods Trade-in” better known as the “New for Old” subsidy program. Under the plan, which began in March of last year, consumers were given subsidies of up to 20% of the purchase price of a variety of retail goods, particularly consumer electronics[1], automobiles, appliances, and a number of home renovation products. This year the CE list was expanded to include mobile phones, tablets, smartwatches, and smart bands, along with a number of additional home appliances. According to estimates, these subsidies were responsible for 44.5% of China’s 2.2% GDP growth last year, and the expanded plan was thought to be responsible for 23.7% of y/y sales in the first half of this year.

The Chinese government funded the plans ostensibly from state revenue and reserves, a portion of which is funded by ultra-long special treasury bonds that are part of the 1.3 trillion yuan 2025 budget, and pays these quarterly subsidy allocations to the states and provinces who are required to contribute no less than 1/9 of the amount granted by the central government. The total central government budget for the subsidies this year is 300 billion ($42.14 billion US) yuan, twice the 2024 allocation, with 162 billion yuan paid out in 1H and (January & April) two 69 billion yuan payments in July and October. A number of provinces have run out of funds as they have exhausted their state allocation, or they are limiting the subsidies to certain items to conserve capital until the Chinese government makes the final October payment.

As the program has been quite successful in stimulating GDP the question remains as to whether the government will renew the plan in 2026. Currently, the budget for the next year is being devised by the State Council, so no announcement as to whether the plan will continue or be cut in size has been made to date. The general consensus seems to be that the plan is unlikely to continue into 2026, at least at the 2025 level. The fact that the final 2025 payment is made in October has led to speculation that the current weakness in Chinese CE demand is related to the fact that the provincial subsidies are typically used up within the first few days of the quarter, leaving the back end demand a bit weak. There is also concern that the subsidies have pulled forward sales, creating a vacuum for demand as the year finishes, along with the general consumer concern of the weakness in Chinese real estate.

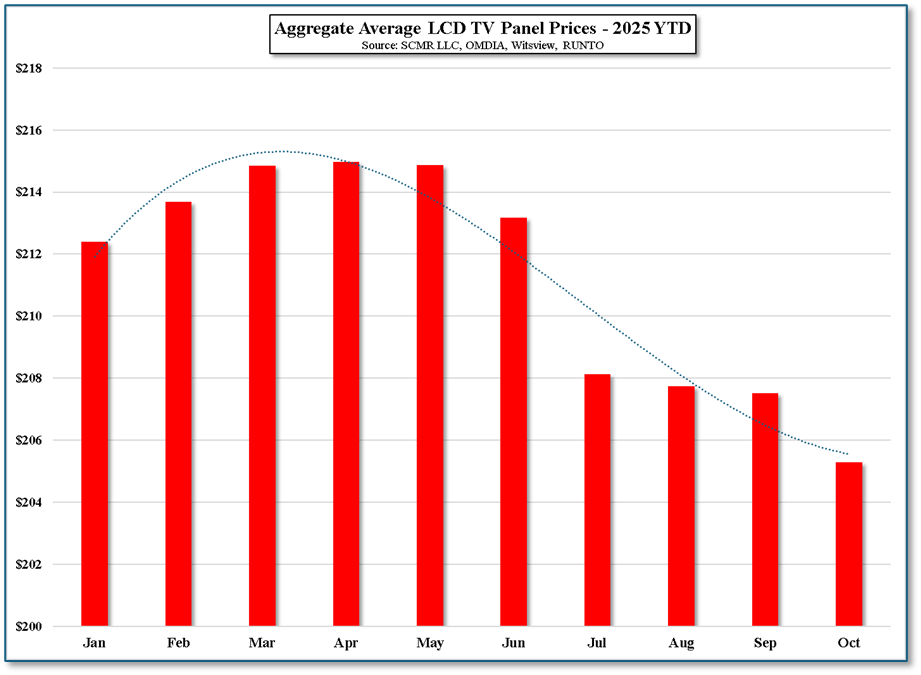

All of this seems to be putting a damper on consumer enthusiasm across the mainland, first showed up in the TV space where prices for LCD large panels have been declining, particularly ultra-large sizes that have been supported by Chinese demand. As noted, China is currently working on their 2026 budget, but they have already set goals for the 2025/2026 years. Their aims are for >5% growth across ‘electronic information manufacturing industries’, outpacing the 4.5% to 5.0% GDP growth expectations for the outgoing 2021-2025 plan. 2026 will be the first year of the new 5-year plan that is currently being devised and could be different than the expectations of prognosticators. We expect less than 5% growth in China’s CE space next year even if the subsidies are renewed, as we expect the amount of the plan to be less than this year’, and as the effect of the subsidies continues to decrease over time. Drivers for CE sales growth in 2026, according to expectations, are:

[1] Televisions, Air Conditioners, Refrigerators, Washing Machines, Computers, water heaters, stoves (household) and kitchen hoods.

The Chinese government funded the plans ostensibly from state revenue and reserves, a portion of which is funded by ultra-long special treasury bonds that are part of the 1.3 trillion yuan 2025 budget, and pays these quarterly subsidy allocations to the states and provinces who are required to contribute no less than 1/9 of the amount granted by the central government. The total central government budget for the subsidies this year is 300 billion ($42.14 billion US) yuan, twice the 2024 allocation, with 162 billion yuan paid out in 1H and (January & April) two 69 billion yuan payments in July and October. A number of provinces have run out of funds as they have exhausted their state allocation, or they are limiting the subsidies to certain items to conserve capital until the Chinese government makes the final October payment.

As the program has been quite successful in stimulating GDP the question remains as to whether the government will renew the plan in 2026. Currently, the budget for the next year is being devised by the State Council, so no announcement as to whether the plan will continue or be cut in size has been made to date. The general consensus seems to be that the plan is unlikely to continue into 2026, at least at the 2025 level. The fact that the final 2025 payment is made in October has led to speculation that the current weakness in Chinese CE demand is related to the fact that the provincial subsidies are typically used up within the first few days of the quarter, leaving the back end demand a bit weak. There is also concern that the subsidies have pulled forward sales, creating a vacuum for demand as the year finishes, along with the general consumer concern of the weakness in Chinese real estate.

All of this seems to be putting a damper on consumer enthusiasm across the mainland, first showed up in the TV space where prices for LCD large panels have been declining, particularly ultra-large sizes that have been supported by Chinese demand. As noted, China is currently working on their 2026 budget, but they have already set goals for the 2025/2026 years. Their aims are for >5% growth across ‘electronic information manufacturing industries’, outpacing the 4.5% to 5.0% GDP growth expectations for the outgoing 2021-2025 plan. 2026 will be the first year of the new 5-year plan that is currently being devised and could be different than the expectations of prognosticators. We expect less than 5% growth in China’s CE space next year even if the subsidies are renewed, as we expect the amount of the plan to be less than this year’, and as the effect of the subsidies continues to decrease over time. Drivers for CE sales growth in 2026, according to expectations, are:

- AI

- AI Smartphones (50% adoption by 2027)

- Smart home products

- Large TVs (75”+ (Penetration to 40% next year)

- Foldables

[1] Televisions, Air Conditioners, Refrigerators, Washing Machines, Computers, water heaters, stoves (household) and kitchen hoods.

Figure 1 - Aggregate Average LCD TV panel Prices - 2025 YTD - Source: SCMR LLC, OMDIA, Witsview, RUNTO

RSS Feed

RSS Feed