Category Conversion

Wearables are a broad consumer electronics category and depending on the source, can include a number of types of devices and specific items. In many cases the ‘wearables’ category primarily includes smartwatches, but some, in this case IDC, include a number of device types, giving the data more granularity. Here is what is included in the data:

Watches:

Rings – Fitness tracking rings or control devices. This can also include modular devices such as active pins or clip-on sensors.

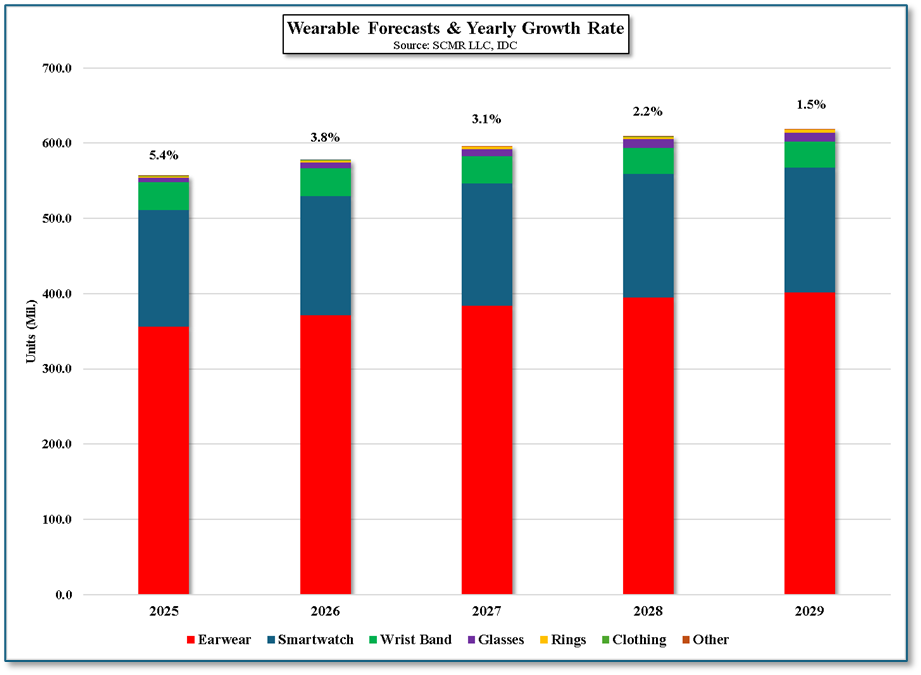

In 2024 the wearables market reached 534.6m units, according to IDC, up 5.4% y/y, however growth is expected to slow a bit this year (up 4.1% to 556.6m units) as larger markets, such as the US and India, begin to see maturity in major wearable categories, earwear (63.9% of total units in 2025) and smartwatches (27.9% of 2025 total). While growth continues through the forecast period (2025 – 2029) it slows each year, again as the two largest categories see lower growth each year. When combined, smartwatches and hearables make up over 91% of the unit volume total. While other categories see growth, particularly the ‘glasses’ category, combined, they remain under 10% throughout the forecast period. Hearables, the largest single category, sees 1.9% growth in 2029 while smartwatch growth is a meager 0.7%.

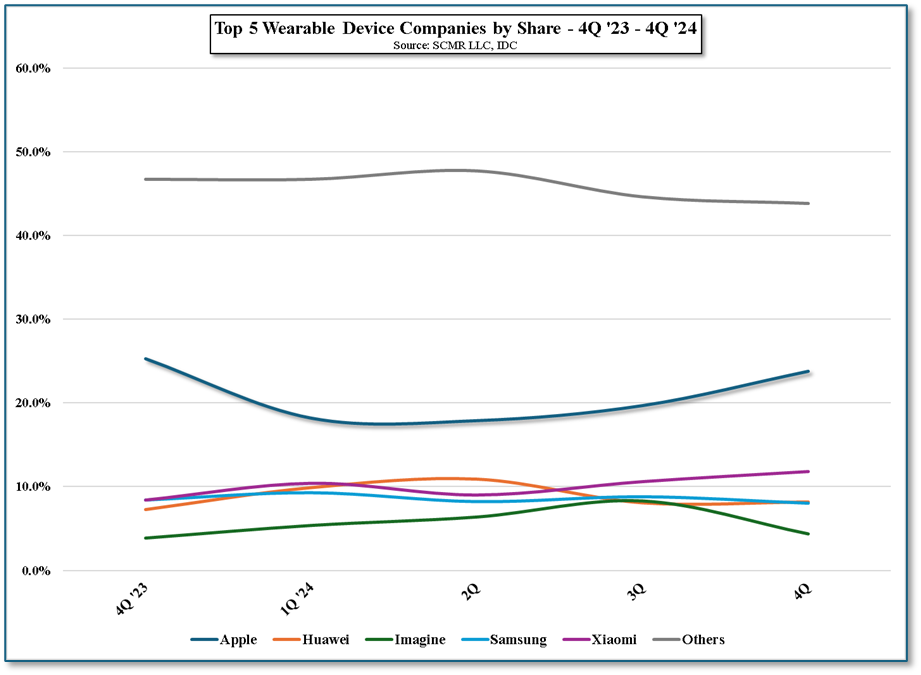

In terms of share, Apple (AAPL) is the leader, especially in 4Q when the newest Apple Watch series is released, with the possibility of also offering the next generation or a refresh of the Air Pods line. While 4Q is typically the peak quarter for Apple, they do remain the share leader throughout most of the year, although it is thought that Huawei (pvt) might take over that lead in 1Q of this year when the most recent data is tabulated. Huawei has benefited from Chinese government subsidies for consumer products, a spate of public nationalism, a governmental push away from Apple, and its own chip development program that have given new confidence to Chinese consumers about Huawei’s long-term sustainability. Huawei has taken advantage of these positives by broadening out its wearable portfolio and pricing products more competitively, while Apple struggles against anti-US sentiment on the mainland.

All in, wearables remain a high volume market that continues to grow, albeit at a more measured pace. Brands are looking to offset the maturity of the smartwatch and earwear segments with new categories, which we suspect will be focused on connections to AI. We expect the ‘glasses’ category to grow a bit faster than IDC products as AI functions give smart glasses either a rich combination of functions (high-end) or highly specialized functions (low-end) that will generate growth and higher unit volumes, especially as new AI applications are popularized. We note that there is already a ‘smart glass’ sub-category for the hearing impaired, with the glasses performing what are essentially conversation sub-titles in real-time. As similar applications appear, the ‘glasses’ category should expand more quickly and become the driver for growth in the category.

Watches:

- Smartwatches

- Basic & Hybrid watches

- Kid’s watches – Some with GPS tracking

- Fitness trackers

- Smart assistants

- Language translators

- Truly wireless earbuds

- Fitness trackers (ear based)

- Smart glasses – With or without displays

- AR/VR headsets

Rings – Fitness tracking rings or control devices. This can also include modular devices such as active pins or clip-on sensors.

In 2024 the wearables market reached 534.6m units, according to IDC, up 5.4% y/y, however growth is expected to slow a bit this year (up 4.1% to 556.6m units) as larger markets, such as the US and India, begin to see maturity in major wearable categories, earwear (63.9% of total units in 2025) and smartwatches (27.9% of 2025 total). While growth continues through the forecast period (2025 – 2029) it slows each year, again as the two largest categories see lower growth each year. When combined, smartwatches and hearables make up over 91% of the unit volume total. While other categories see growth, particularly the ‘glasses’ category, combined, they remain under 10% throughout the forecast period. Hearables, the largest single category, sees 1.9% growth in 2029 while smartwatch growth is a meager 0.7%.

In terms of share, Apple (AAPL) is the leader, especially in 4Q when the newest Apple Watch series is released, with the possibility of also offering the next generation or a refresh of the Air Pods line. While 4Q is typically the peak quarter for Apple, they do remain the share leader throughout most of the year, although it is thought that Huawei (pvt) might take over that lead in 1Q of this year when the most recent data is tabulated. Huawei has benefited from Chinese government subsidies for consumer products, a spate of public nationalism, a governmental push away from Apple, and its own chip development program that have given new confidence to Chinese consumers about Huawei’s long-term sustainability. Huawei has taken advantage of these positives by broadening out its wearable portfolio and pricing products more competitively, while Apple struggles against anti-US sentiment on the mainland.

All in, wearables remain a high volume market that continues to grow, albeit at a more measured pace. Brands are looking to offset the maturity of the smartwatch and earwear segments with new categories, which we suspect will be focused on connections to AI. We expect the ‘glasses’ category to grow a bit faster than IDC products as AI functions give smart glasses either a rich combination of functions (high-end) or highly specialized functions (low-end) that will generate growth and higher unit volumes, especially as new AI applications are popularized. We note that there is already a ‘smart glass’ sub-category for the hearing impaired, with the glasses performing what are essentially conversation sub-titles in real-time. As similar applications appear, the ‘glasses’ category should expand more quickly and become the driver for growth in the category.

Figure 1 - Wearable Forcasts & Yearly Growth Rate - Source: SCMR LLC, IDC

Figure 2 - Top 5 Wearable Device Companies by Share - 4Q '23 - 4Q '24 - Source: SCMR LLC, IDC

RSS Feed

RSS Feed