AUO to Buy Automotive Controls Company

Display producer AU Optronics (2409.TT) has announced the purchase of Behr-Hella Thermocontrols GmbH for €600m ($632m US), a producer of vehicle climate control panels, Climate sensors, power related hardware for automotive heating and cooling blowers, and associated software. The company’s customer base is large, with a ~20% share of the market, 2nd only to Denso (6902.T) at ~24% and provides climate controls and other products to BMW (BMW.DE), Daimler (DTG.DE), GM (GM), Ford (F), and others. AUO has made other acquisitions that have brought it deeper into the automotive display market, with Litemax Electronics (4995.TT) in 2017 that helped AUO with backlighting technology for automotive instrument clusters, and Raystar Technologies (pvt) in 2018 that brought in technology for large automotive displays.

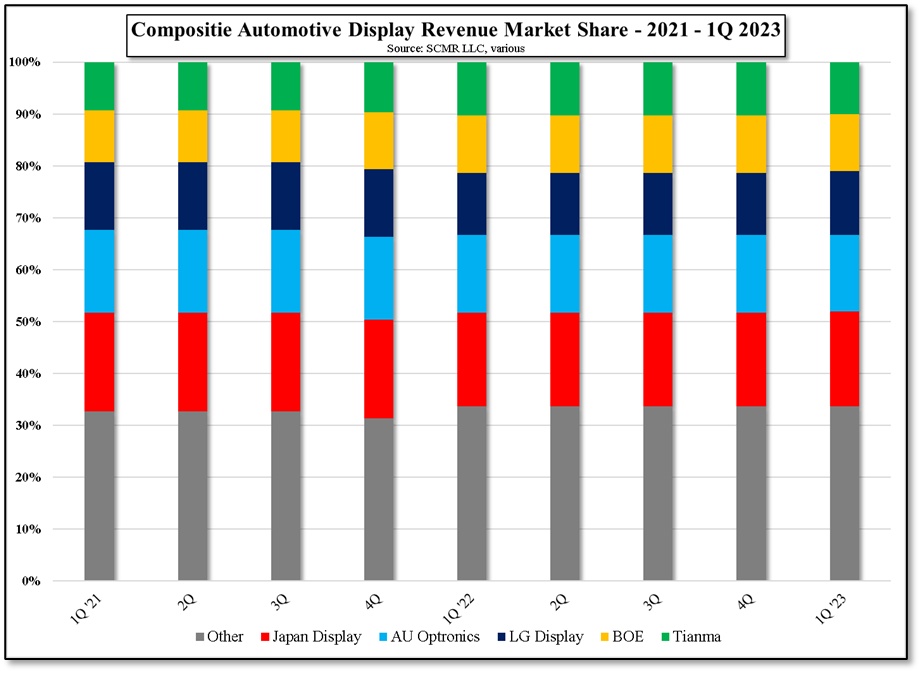

In 2020 AUO began breaking out their automotive display business share, which has grown from a low of 6% in 2Q ’20 to 17% for the last two quarters of l2022and the first quarter of this year. It declined to 16% in 2Q as TV panel revenue increased, but we expect automotive to remain between 16% and 18% for the remainder of the year. AUO, along with a number of other panel producers, have been increasing their exposure to the automotive display market as the industry returned to pre-pandemic demand levels last year. The automotive display business is a bit different that the typical seasonally driven generic display business in that the development cycles are long relative to the CE space, but the product sustainability is also long, typically 2 to 3 years, so those panel producers looking for a more predictable business cycle have shifted their focus.

AUO began that process earlier than many other panel producers, but automotive display market share tends to remain stable for the reasons mentioned above and has not changed appreciably over the last few quarters. That said, the automotive display market is oriented toward hybrid or electric vehicles, although not exclusively, but given China’s large share of the electric vehicle manufacturing market, Chinese panel producers have at least a starting advantage over automotive display producers from other regions, with Chinese display producers BOE (200125.CH) and Tianma (000050.CH) having a combined 21%+ share. Rather than compete on a capacity basis, AUO’s general philosophy has been to produce high-end, non-generic products, and does the same in the automotive space. We would expect to see other acquisitions that give them additional expertise in the automotive space, especially as LCD is by far the dominant display type in automotive displays, with Mini-LED backlighting beginning to appear as a way to compete with OLED displays.

AUO began that process earlier than many other panel producers, but automotive display market share tends to remain stable for the reasons mentioned above and has not changed appreciably over the last few quarters. That said, the automotive display market is oriented toward hybrid or electric vehicles, although not exclusively, but given China’s large share of the electric vehicle manufacturing market, Chinese panel producers have at least a starting advantage over automotive display producers from other regions, with Chinese display producers BOE (200125.CH) and Tianma (000050.CH) having a combined 21%+ share. Rather than compete on a capacity basis, AUO’s general philosophy has been to produce high-end, non-generic products, and does the same in the automotive space. We would expect to see other acquisitions that give them additional expertise in the automotive space, especially as LCD is by far the dominant display type in automotive displays, with Mini-LED backlighting beginning to appear as a way to compete with OLED displays.

AU Optronics - Automotive Revenue - Source: SCMR LLC, Company Data

Composite Automotive Display Revenue Market Share - 2021 - 1Q 2023 - Source: SCMR LLC, various

RSS Feed

RSS Feed