Buying Growth

TV set unit volume has been on the decline in China, and, as we have noted, the Chinese government has been subsidizing TV set purchases since August of last year as part of a broader program to stimulate the replacement of older CE products. The “Swap Old for New” program has a stated purpose of stimulating consumer spending, promoting energy conservation, and improving the quality of life of consumers by upgrading appliances to newer and more technically advanced models, although we believe stimulating consumer spending is the overriding goal.

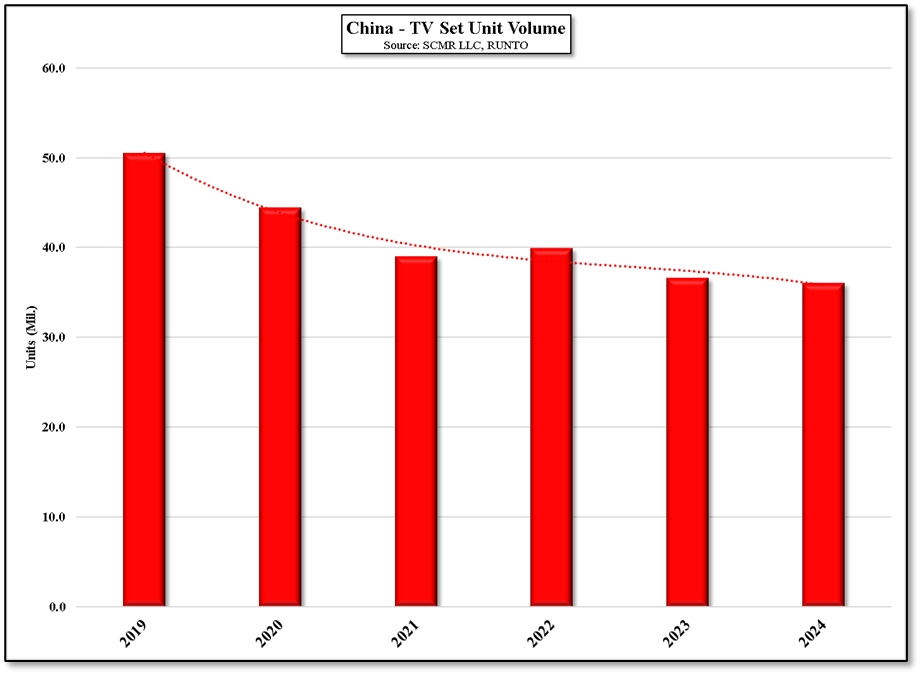

There is little empirical data as to why TV set volumes have been on the decline in China for the last few years but if the Chinese population is moving closer to the attitudes of westernized countries, they have less time to sit in front of a TV as their lives become more complex. However, even more of an influence is the availability of other display types, particularly inexpensive smartphones. US consumers spend 3 hrs. 33 mins. on their phones each day, just a bit below the global average of 3 hrs. 50 mins, and Chinese citizens are getting close at 3 hrs. 19 mins.[1] With less overall time available and a more convenient solution than TV, it is not surprising that TV set volumes have declined as China’s social development matures.

.

[1] https://explodingtopics.com/blog/smartphone-usage-stats

There is little empirical data as to why TV set volumes have been on the decline in China for the last few years but if the Chinese population is moving closer to the attitudes of westernized countries, they have less time to sit in front of a TV as their lives become more complex. However, even more of an influence is the availability of other display types, particularly inexpensive smartphones. US consumers spend 3 hrs. 33 mins. on their phones each day, just a bit below the global average of 3 hrs. 50 mins, and Chinese citizens are getting close at 3 hrs. 19 mins.[1] With less overall time available and a more convenient solution than TV, it is not surprising that TV set volumes have declined as China’s social development matures.

.

[1] https://explodingtopics.com/blog/smartphone-usage-stats

Figure 1 - China - TV Set Unit Volume - Source: SCMR LLC, RUNTO

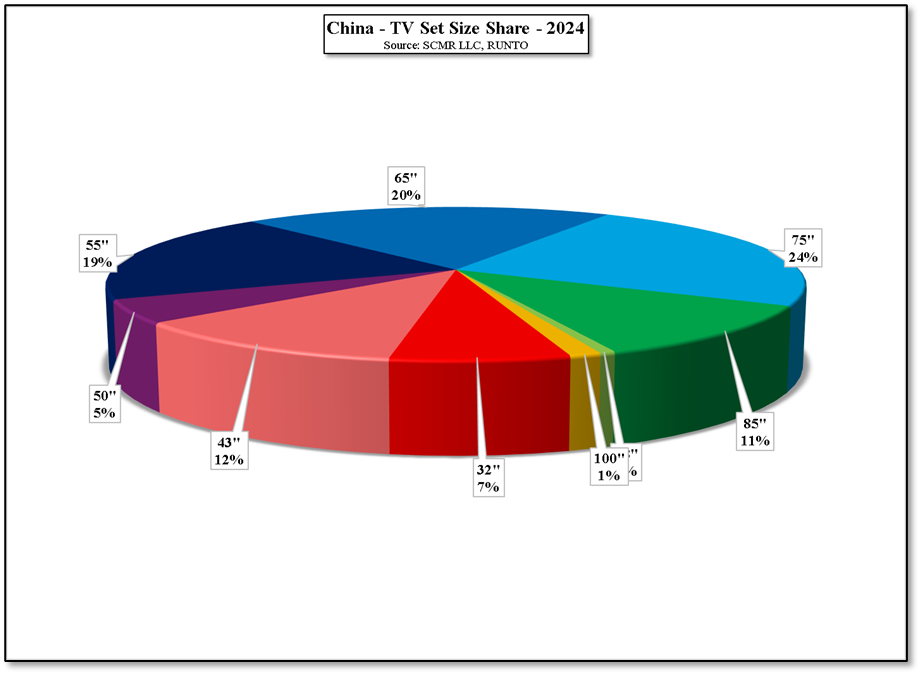

In fact, TV set sales in China have declined, but have also shifted to larger sets, serving as an entertainment source rather than an information source, with the average TV set size increasing 3.3” in 2024 after a 3.0” increase the year before. For the first time ever, the unit volume share of 75” TVs was greater than that of 65” TVs. 65” TVs became the leader only two years ago and 85” TVs, which made up 10.9% of unit volume, saw 56.7% y/y unit growth last year.

Figure 2 - China - TV Set Size Share - Source: SCMR LLC, RUNTO

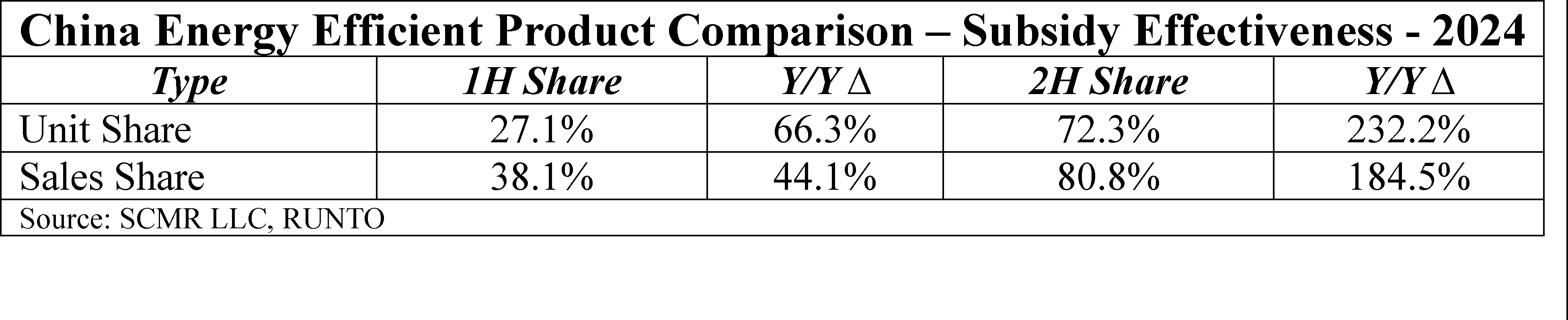

The effectiveness of Chinese consumer subsidies, which are financed through both government budget allocations and the issuance of bonds, can be measured to a degree as they are specific to certain product criteria. The Chinese government has 5 levels of energy efficiency that are attached to consumer products, with one being the most efficient and 5 the least. The subsidies only apply to levels 1 and 2 on a sliding scale, and Chinese TV brands found relatively inexpensive ways to move lower efficiency rated Tv models up to levels 1 and 2 to qualify without the expense and time of a full redesign. By the time the TV set subsidies kicked in, many lower efficiency models had already been upgraded, giving consumers a wide range of choices under the plan.

Since TV set energy efficiency was only a small factor in Chinese consumer’s minds before the subsidy became effective, comparing 1H energy efficient TV set volumes (Pre-Subsidy) against 2H energy efficient TV set volumes (Post-Subsidy) gives clues as to how influential the subsidies were. As shown below, energy-efficient TVs (level 1 & 2) represented 27.1% of unit volume and 38.1% of sales, however in 2H, after the subsidies had been put in place (August), energy efficient TVs represented 72.3% of unit volume and 80.8% of sales. To compensate for possible seasonality we show that the y/y increase in units in 1H was 66.3% but was 232.2% in 2H and similarly, sales were up 44.1% y/y in 1H but up 184.5% y/y in 2H.

Since TV set energy efficiency was only a small factor in Chinese consumer’s minds before the subsidy became effective, comparing 1H energy efficient TV set volumes (Pre-Subsidy) against 2H energy efficient TV set volumes (Post-Subsidy) gives clues as to how influential the subsidies were. As shown below, energy-efficient TVs (level 1 & 2) represented 27.1% of unit volume and 38.1% of sales, however in 2H, after the subsidies had been put in place (August), energy efficient TVs represented 72.3% of unit volume and 80.8% of sales. To compensate for possible seasonality we show that the y/y increase in units in 1H was 66.3% but was 232.2% in 2H and similarly, sales were up 44.1% y/y in 1H but up 184.5% y/y in 2H.

The Chinese swap subsidy plan remains in effect in 1Q, although we expect its effect will diminish over time, however Chinese prognosticators expect it to have enough of an impact to grow Chinese TV set shipment 2.1% this year. While from a macro view, there is certainly a case to be made for TV set shipment growth on the mainland, but our concern is that the 2024 TV set subsidies have ‘stolen’ sales and potential upgraders from 2025, resulting in weaker than expected full year 2025-unit volume. Sales could increase as the share of larger TVs continues to grow, against the negative of competitive brand pricing, but growth in unit volume might be harder to find. Of course there is always the potential for larger subsidies but buying growth through subsidies is expensive way for the Chinese government to show the world that China is back on a growth track.

RSS Feed

RSS Feed